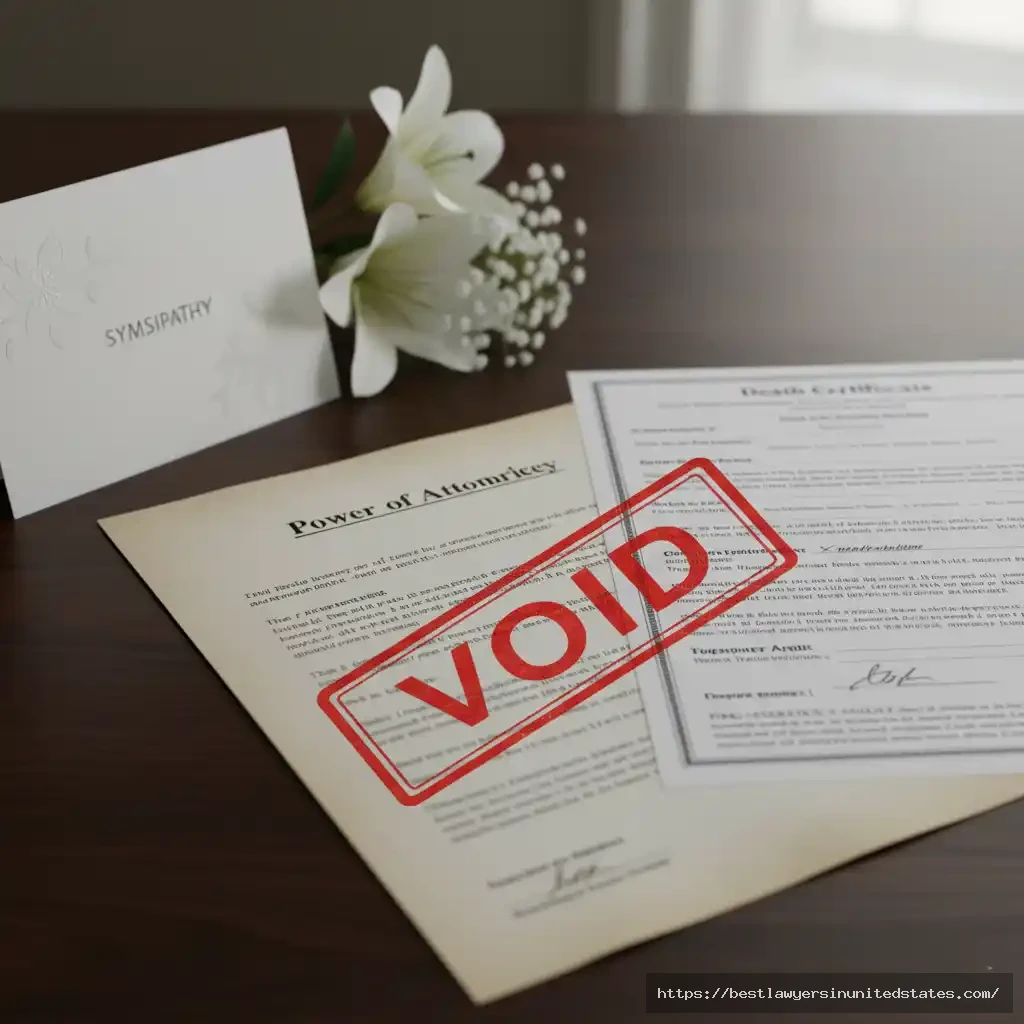

When a loved one passes away, families are often left scrambling to handle financial accounts, property, and legal obligations. If you held Power of Attorney (POA) for the deceased, you might assume you can continue managing their affairs. But here’s the hard truth: a Power of Attorney becomes completely invalid the moment someone dies—no exceptions.

This isn’t just a technicality. Using a POA after death can lead to serious legal consequences, including accusations of fraud or theft. Understanding exactly when and why a POA ends is critical for anyone handling end-of-life matters or planning their own estate.

What Is a Power of Attorney? (Legal Definition & Function)

A Power of Attorney is a legal document that grants one person—called the agent or attorney-in-fact—the authority to make decisions and take actions on behalf of another person, known as the principal. It’s one of the most important tools in estate planning, allowing someone you trust to step in when you’re unable to manage your own affairs due to illness, disability, travel, or simply convenience.

The scope of a POA can be broad or highly specific. Depending on how the document is drafted, your agent may be authorized to handle financial transactions, manage real estate, pay bills, file taxes, or even make healthcare decisions. The key is that all of this authority exists only while the principal is alive.

For more information on the legal responsibilities of agents and best practices for creating a POA, refer to the American Bar Association’s guidance on Powers of Attorney.

Common Uses of Power of Attorney:

- Managing bank accounts and investments

- Buying, selling, or refinancing property

- Handling business operations

- Paying bills and settling debts

- Making medical or end-of-life decisions (with a Medical POA)

The agent has a fiduciary duty, meaning they must act in the principal’s best interest at all times. Misuse of this authority—whether through negligence or intentional harm—can result in civil or criminal liability.

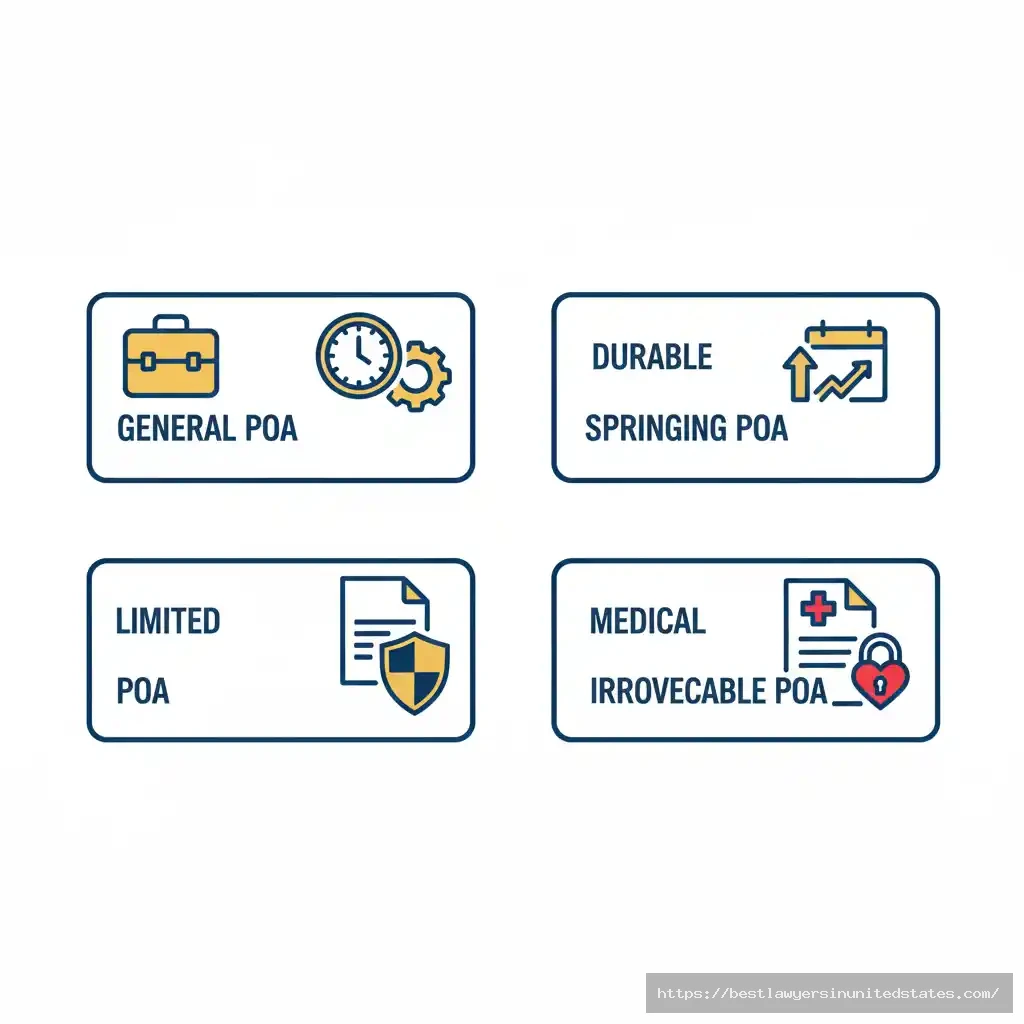

Types of Power of Attorney (And How They Differ)

Not all Powers of Attorney are created equal. The type of POA you choose determines when it takes effect, how long it lasts, and what decisions the agent can make. Here are the most common types:

1. General Power of Attorney

A General POA grants broad authority to the agent to handle nearly all financial and legal matters on behalf of the principal. This includes managing bank accounts, signing contracts, and handling real estate transactions. However, a General POA typically ends if the principal becomes incapacitated—unless it’s also durable.

2. Durable Power of Attorney

A Durable POA remains valid even if the principal becomes mentally or physically incapacitated. This is the most common type used in estate planning because it ensures continuity of decision-making during illness or cognitive decline. Important: Even a durable POA terminates immediately upon the principal’s death.

3. Springing Power of Attorney

A Springing POA doesn’t take effect until a specific event occurs—usually when the principal becomes incapacitated. This type requires proof (often from a doctor) that the triggering condition has been met. While it offers more control, it can also cause delays when quick action is needed.

4. Limited (or Special) Power of Attorney

A Limited POA grants authority for a specific task or time period only. For example, you might give someone limited POA to sell your car while you’re out of the country. Once the task is complete or the time expires, the POA ends.

5. Medical (or Healthcare) Power of Attorney

A Medical POA authorizes the agent to make healthcare decisions on behalf of the principal, including treatment options, surgical procedures, and end-of-life care. This is separate from financial POAs and is often paired with a living will or advance directive.

6. Irrevocable Power of Attorney

An Irrevocable POA cannot be canceled or changed by the principal once it’s executed. These are rare and typically used in very specific circumstances, such as Medicaid planning or certain business transactions. Critical point: Even an irrevocable POA becomes invalid when the principal dies.

Key Takeaway:

Regardless of type—general, durable, springing, limited, medical, or irrevocable—all Powers of Attorney share one common trait: they end the moment the principal passes away. No POA survives death, no matter how it’s worded or what powers it grants.

Does Power of Attorney End at Death? (The Legal Answer)

Yes. A Power of Attorney automatically terminates the moment the principal dies. This is true in every U.S. state and is a fundamental principle of estate law. There are no exceptions, no grace periods, and no provisions in the POA document itself that can extend its validity beyond death.

For a more detailed breakdown of the legal timeline and state-specific variations, see our guide on understanding when a Power of Attorney ends at death.

Why Does POA End at Death?

The reason is rooted in the legal concept of agency. A Power of Attorney is designed to allow someone to act on behalf of a living person. When that person dies, their legal identity shifts—they no longer have rights, obligations, or the capacity to authorize actions. At that point, their estate becomes a separate legal entity, and control passes to the executor or court-appointed administrator, not the former agent.

Think of it this way: the agent’s authority was borrowed from the principal. Once the principal is gone, there’s nothing left to borrow from.

This Rule Applies to All Types of POA

Many people mistakenly believe that a durable or irrevocable Power of Attorney continues after death because these documents are designed to survive incapacity. But durability only refers to the principal’s mental or physical condition while alive—not their death.

Here’s the breakdown:

- ✅ Durable POA: Valid during incapacity, but ends at death

- ✅ Irrevocable POA: Cannot be canceled by the principal, but ends at death

- ✅ Lasting Power of Attorney (UK term): Still terminates upon death

- ✅ Springing POA: Only activates under certain conditions, but ends at death

State-Specific Considerations

While the rule is universal, the process for transferring authority after death can vary by state:

- Texas: The executor must apply for Letters Testamentary through probate court to gain legal authority over the estate.

- California: Similar process, but California also allows for simplified procedures if the estate qualifies as a “small estate.”

- Florida: Florida law is strict about POA termination and has specific statutes addressing abuse of authority after death.

- Ontario (Canada): A Power of Attorney for Property ends at death; estate authority passes to the estate trustee named in the will.

No matter where you live, the takeaway is the same: once someone dies, the POA is legally dead too.

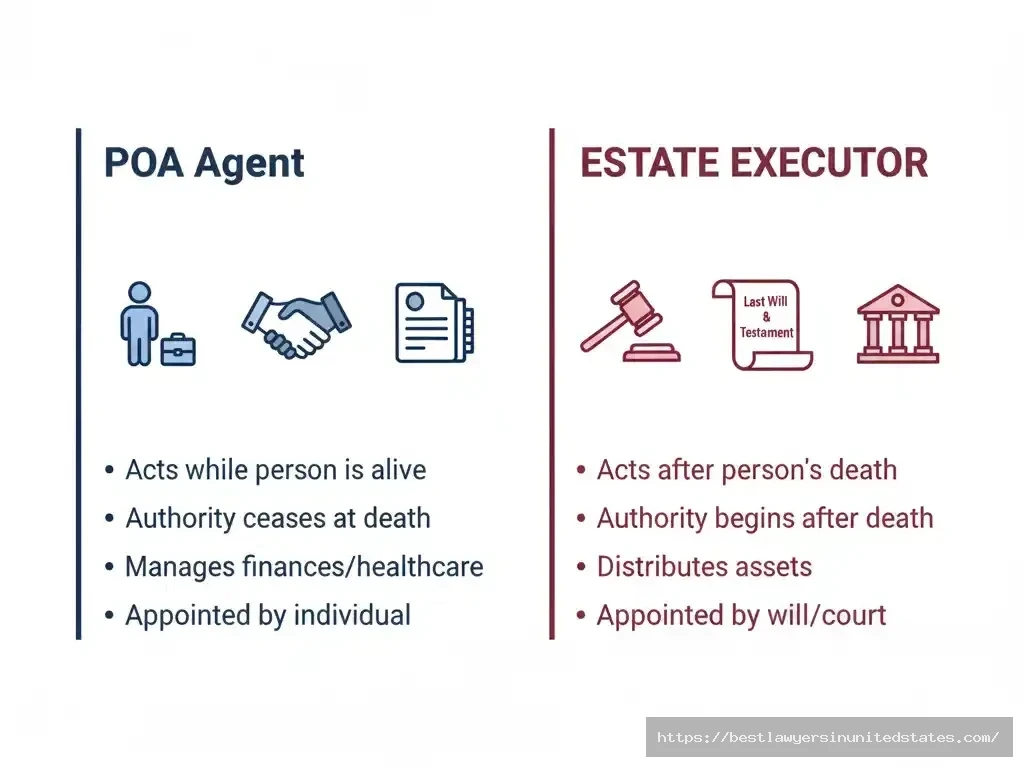

What Happens to the Agent’s Authority After Death?

The moment the principal dies, the agent’s legal authority vanishes. This means the agent can no longer:

- Access or manage bank accounts

- Sell, transfer, or mortgage real estate

- Sign contracts or legal documents

- Make financial decisions

- Pay bills from the deceased’s accounts

- Withdraw or move funds

Any action taken under the POA after the principal’s death is considered unauthorized and illegal—even if the agent has good intentions or believes they’re helping the family. Financial institutions are legally required to freeze accounts once they’re notified of a death, and any transactions made after that point can be reversed or investigated as potential fraud.

What If the Agent Didn’t Know About the Death?

Ignorance doesn’t provide legal protection. If an agent continues to act under a POA after the principal has died—even unknowingly—those actions can still be challenged. Banks, creditors, and beneficiaries have the right to question or void transactions made without proper authority.

That said, courts generally distinguish between innocent mistakes and intentional abuse. If you genuinely didn’t know the principal had passed and acted in good faith, you’re less likely to face criminal charges—but you could still be held liable for returning funds or reversing transactions.

The Agent’s Remaining Responsibilities

While the agent can no longer act on behalf of the deceased, they do have a few post-death obligations:

- Notify relevant parties that the principal has died (banks, insurance companies, creditors)

- Secure physical assets like property, vehicles, or valuable personal items to prevent loss or theft

- Turn over all records and documentation to the executor or personal representative

- Cooperate with the estate if questions arise about transactions made before death

The agent does not become the executor automatically—even if they were named as POA. These are two entirely separate roles that must be designated in different legal documents.

What Happens If Your Power of Attorney Dies Before You?

This is a scenario many people overlook when creating estate plans—but it’s more common than you might think. If the person you’ve named as your agent dies before you do, or becomes incapacitated themselves, your Power of Attorney doesn’t automatically transfer to someone else. Instead, the document becomes ineffective unless you’ve planned ahead.

Understanding the difference between Power of Attorney and conservatorship can help you make informed decisions about which legal tools are right for your situation.

Naming a Successor Agent

The best way to protect yourself is to designate a successor agent (also called an alternate or backup agent) in your POA document. A successor agent is someone who steps in if your primary agent is unable or unwilling to serve. You can name multiple successors in order of priority.

For example:

- Primary Agent: Your spouse

- First Successor: Your adult child

- Second Successor: Your sibling or trusted friend

If your POA doesn’t include a successor agent and your primary agent dies or becomes incapacitated, you’ll need to execute a new Power of Attorney—assuming you’re still mentally competent to do so.

What If You’re No Longer Competent?

This is where things get complicated. If your agent dies and you lack the mental capacity to sign a new POA, your family will need to petition the court for guardianship or conservatorship. This is a lengthy, expensive legal process that involves:

- Filing a petition with the probate court

- Medical evaluations to prove incapacity

- Court hearings and potential objections from family members

- Ongoing court supervision and reporting requirements

Guardianship can cost thousands of dollars and take months to establish—all of which could have been avoided by naming a successor agent in the original POA.

Best Practice: Review and Update Your POA Regularly

Life changes. Your agent might move away, become ill, pass away, or simply no longer be the right choice. It’s smart to review your Power of Attorney every few years and update it as needed. If your agent’s circumstances have changed, don’t wait—execute a new POA while you still have the legal capacity to do so.

Who Takes Over When POA Ends at Death? (Executor vs. Administrator)

Once the Power of Attorney terminates at death, legal authority over the deceased’s affairs must be transferred to someone else. But who that person is—and what they’re called—depends on whether the deceased left a will.

If There Is a Will: The Executor

If the deceased left a valid Last Will and Testament, they likely named an executor (also called a personal representative in some states). The executor is responsible for managing the estate, paying debts, and distributing assets according to the terms of the will.

However, being named in a will doesn’t automatically grant authority. The executor must first go through the probate process, which involves:

- Filing the will with the probate court

- Petitioning the court to be officially appointed

- Receiving Letters Testamentary—a legal document that proves the executor’s authority

Only after receiving Letters Testamentary can the executor legally access accounts, sell property, or act on behalf of the estate. This process can take weeks or even months, depending on the complexity of the estate and the court’s schedule.

If There Is No Will: The Administrator

If the deceased died intestate (without a will), the court will appoint an administrator to handle the estate. This person is typically a close family member—such as a spouse, adult child, or sibling—but the court makes the final decision based on state law and family circumstances.

The administrator’s role is similar to an executor’s, but they must follow the state’s intestacy laws rather than the deceased’s wishes. To gain legal authority, the administrator must petition the court and receive Letters of Administration.

Key Differences: Executor vs. Administrator

| Executor | Administrator |

|---|---|

| Named in the will | Appointed by the court |

| Follows the deceased’s wishes | Follows state intestacy laws |

| Receives Letters Testamentary | Receives Letters of Administration |

| Process may be faster if will is clear | Process may take longer due to family disputes |

Can the Same Person Be Agent and Executor?

Yes—many people choose to name the same trusted individual as both their Power of Attorney agent and their executor. However, these are two completely separate roles that must be designated in two different documents: the POA and the will.

Being someone’s agent does not automatically make you the executor, and vice versa. If you want the same person to serve in both capacities, you must explicitly name them in each document.

How to Get Legal Authority After Someone Dies (Letters Testamentary vs. Letters of Administration)

After someone passes away, no one—not even close family members—has automatic legal authority to manage their estate. Whether you were named as executor in a will or need to be appointed as administrator, you must go through the probate court to obtain the legal documents that prove your authority.

What Are Letters Testamentary?

Letters Testamentary are official court documents issued to the executor named in a will. They serve as proof that the executor has been legally authorized to act on behalf of the estate. With Letters Testamentary, the executor can:

- Open or close bank accounts in the estate’s name

- Access the deceased’s financial records

- Sell real estate or personal property

- Pay outstanding debts and taxes

- Distribute assets to beneficiaries

What Are Letters of Administration?

Letters of Administration serve the same purpose as Letters Testamentary, but they’re issued when there is no will or when the named executor cannot or will not serve. The court appoints an administrator (usually a close family member) and grants them legal authority to manage the estate according to state intestacy laws.

How to Obtain Letters Testamentary or Letters of Administration

The process varies by state, but generally includes these steps:

Step 1: File a Petition with Probate Court

You must file a petition to open probate and request appointment as executor or administrator. This typically requires submitting the original will (if one exists), a certified copy of the death certificate, and information about the estate’s assets and heirs.

Step 2: Notify Interested Parties

Most states require you to notify all beneficiaries, heirs, and creditors that probate has been opened. This gives them an opportunity to object or file claims against the estate.

Step 3: Attend a Court Hearing (if required)

In some cases, the court may schedule a hearing to confirm your appointment. If there are no objections or complications, this step may be waived.

Step 4: Receive Your Letters

Once the court approves your petition, you’ll receive Letters Testamentary or Letters of Administration. You’ll typically need certified copies to present to banks, insurance companies, and other institutions.

How Long Does the Process Take?

The timeline varies widely:

- Simple estates with a clear will: 2–6 weeks

- Estates with disputes or complications: Several months to over a year

- Intestate estates: Often longer due to the need to identify heirs and resolve family disagreements

Important: You Cannot Act Without Court Authority

Until you receive Letters Testamentary or Letters of Administration, you have no legal right to access the deceased’s accounts, sell property, or make decisions on behalf of the estate—even if you’re a close family member or were previously their Power of Attorney agent. Acting without proper authority can result in personal liability and legal consequences.

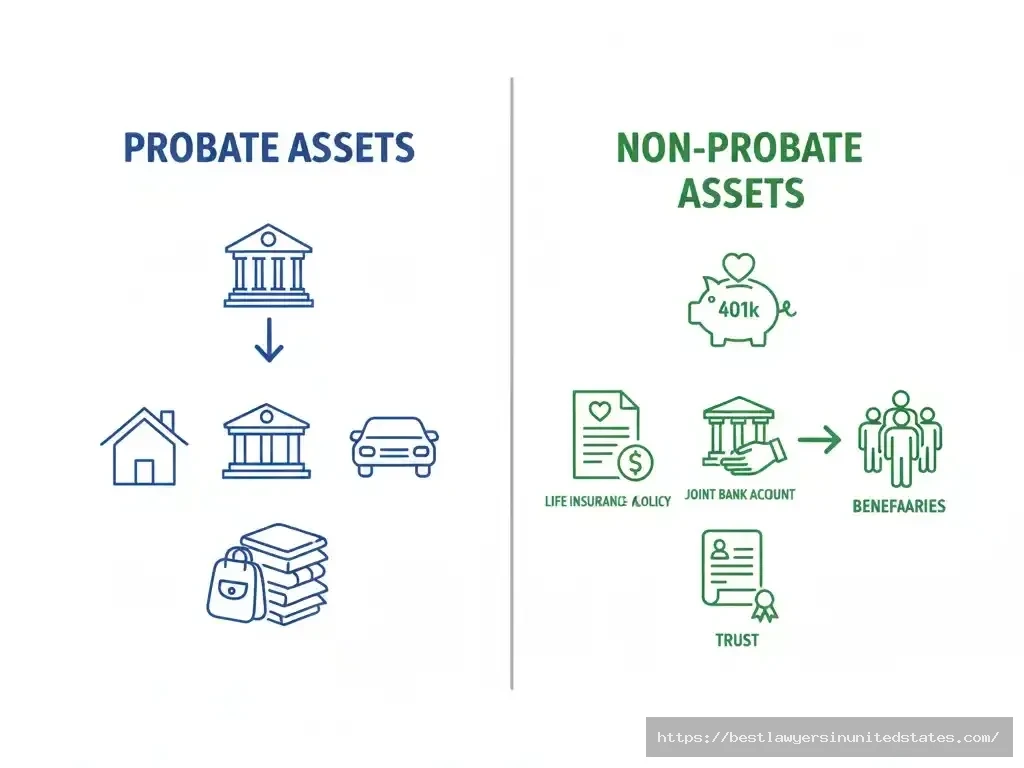

Probate vs. Non-Probate Assets: What the Executor Can and Can’t Touch

Not all assets go through probate, and understanding the difference is crucial for anyone handling a loved one’s estate. Some assets pass directly to beneficiaries without court involvement, while others must be managed by the executor through the probate process.

What Are Probate Assets?

Probate assets are those owned solely by the deceased at the time of death, with no designated beneficiary or co-owner. These assets cannot be distributed until the probate court approves, and the executor must use them to pay debts and taxes before distributing what remains to heirs.

Common probate assets include:

- Bank accounts in the deceased’s name only

- Real estate titled solely in the deceased’s name

- Vehicles without a transfer-on-death designation

- Personal property (jewelry, furniture, collectibles)

- Business interests without a succession plan

What Are Non-Probate Assets?

Non-probate assets bypass the probate process entirely and transfer directly to the named beneficiaries or co-owners. The executor has no control over these assets, and they cannot be used to pay the deceased’s debts (with some exceptions).

Common non-probate assets include:

- Joint accounts with right of survivorship – automatically pass to the surviving account holder

- Payable-on-death (POD) or transfer-on-death (TOD) accounts – go directly to the named beneficiary

- Life insurance policies – paid to the designated beneficiary

- Retirement accounts (401(k), IRA) – distributed according to beneficiary designations

- Assets held in a trust – managed by the trustee, not the executor

- Real estate with transfer-on-death deeds – transfers to the named beneficiary without probate

Can You Withdraw Money from a Deceased Person’s Bank Account?

This is one of the most frequently asked questions after someone dies—and the answer depends on the type of account:

❌ If it’s a sole account (probate asset): No. Only the executor with Letters Testamentary can access it. Withdrawing funds without authority is illegal and can be prosecuted as theft or fraud.

✅ If it’s a joint account with right of survivorship: Yes. The surviving account holder has immediate access and full ownership.

✅ If it’s a POD account: Yes, but only the named beneficiary—and usually only after presenting a death certificate to the bank.

❌ If you were the POA agent: No. Your authority ended at death, even if you previously had access to the account.

Why This Matters for Estate Planning

Understanding the difference between probate and non-probate assets helps families avoid costly delays. By properly designating beneficiaries on accounts and using tools like trusts or TOD designations, you can ensure assets pass quickly to loved ones without waiting for probate to conclude.

However, be cautious: making all assets non-probate can backfire if the estate doesn’t have enough probate assets to cover debts, taxes, and final expenses. Balance is key.

Abuse of Power of Attorney After Death: Warning Signs & Legal Remedies

While most agents act in good faith, abuse of Power of Attorney—especially around the time of death—is more common than many families realize. When an agent continues to use POA authority after the principal dies, whether intentionally or through confusion, it can result in significant financial harm to the estate and its beneficiaries.

What Is Abuse of Power of Attorney After Death?

Abuse occurs when someone uses POA authority after it has legally terminated. This includes any actions taken in the principal’s name after their death, such as:

- Withdrawing money from bank accounts

- Transferring property or assets

- Selling real estate or vehicles

- Paying themselves from estate funds

- Writing checks or making electronic transfers

- Hiding or destroying financial records

- Making last-minute changes to beneficiary designations

Even if the agent believes they’re acting in the family’s best interest—such as paying funeral expenses or keeping up with bills—using expired POA authority is still illegal.

Warning Signs of POA Abuse After Death

If you suspect someone has misused POA authority after a loved one’s death, watch for these red flags:

- Unexplained withdrawals from bank accounts in the days before or after death

- Missing assets or valuables that were known to exist

- Rushed transactions completed right before or immediately after death

- Secretive behavior or refusal to provide financial documentation

- Conflicting statements about the deceased’s finances or wishes

- Sudden changes to beneficiary designations or account titles shortly before death

- Unpaid bills despite sufficient funds in accounts the agent controlled

Legal Remedies for POA Abuse After Death

If you believe a former agent has abused their authority, you have several legal options:

1. Demand an Accounting

The executor or administrator can formally request a complete record of all transactions the agent made, both before and after death. If the agent refuses or provides incomplete information, this can be evidence of wrongdoing.

2. File a Civil Lawsuit

Beneficiaries or the estate can sue the former agent for breach of fiduciary duty, conversion (legal term for theft), or fraud. If successful, the court can order the agent to return misappropriated funds plus interest, and may award damages.

3. Report to Law Enforcement

In cases of clear theft or fraud—such as forging signatures or making large unauthorized withdrawals after death—criminal charges may be appropriate. Contact your local district attorney’s office or elder abuse hotline.

4. Freeze Accounts

The executor can work with financial institutions to freeze accounts and reverse unauthorized transactions. Banks are generally cooperative once provided with a death certificate and evidence of abuse.

5. Remove the Agent from Any Remaining Roles

If the person who abused POA authority is also named as executor or trustee, the court can remove them and appoint someone else. Past misconduct is strong grounds for disqualification.

If family disputes escalate or the former agent refuses to cooperate, consulting an estate litigation attorney may be necessary to protect the estate’s interests.

Protecting Your Estate from POA Abuse

To minimize the risk of abuse, consider these precautions when creating your Power of Attorney:

- Choose an agent with unquestionable integrity and financial responsibility

- Name a successor agent who can step in if concerns arise

- Require regular accountings or financial reports

- Limit the agent’s authority to specific tasks or time periods

- Include oversight provisions that allow a third party (like an attorney or family member) to review transactions

- Work with an estate planning attorney to ensure proper safeguards are in place

What to Do Immediately After Someone Dies: A Step-by-Step Checklist

The hours and days following a death are overwhelming. While grief is natural, there are critical legal and financial steps that must be taken quickly to protect the estate and ensure a smooth transition. Here’s a practical checklist to guide you through the immediate aftermath.

Within the First 24–48 Hours

1. Obtain a Legal Pronouncement of Death

If the person died at home or outside a medical facility, call 911 or the person’s physician. A doctor, coroner, or medical examiner must legally pronounce the death before any next steps can be taken.

2. Notify Close Family Members

Inform immediate family, close friends, and anyone who needs to know right away. This prevents confusion and ensures everyone is on the same page before decisions are made.

3. Stop Using Power of Attorney Immediately

If you were the POA agent, your authority ended the moment of death. Do not access accounts, sign documents, or make any transactions under the POA from this point forward.

4. Secure the Deceased’s Property

Lock the home, secure vehicles, and protect valuable items. Change locks if necessary, especially if multiple people had keys. This prevents theft and disputes over personal property.

5. Locate Important Documents

Find the will, trust documents, insurance policies, bank statements, titles, deeds, and any other estate planning paperwork. These will be needed for probate and to notify relevant institutions.

6. Contact the Funeral Home or Mortuary

Make arrangements for the body to be transported and cared for. The funeral home can also help you order death certificates, which you’ll need multiple certified copies of.

Within the First Week

7. Order Death Certificates

You’ll need at least 10–15 certified copies to provide to banks, insurance companies, Social Security, and other institutions. Order more than you think you’ll need—obtaining additional copies later can be time-consuming.

8. Notify Social Security Administration

Call the SSA at 1-800-772-1213 to report the death. If the deceased was receiving benefits, the funeral home often handles this notification, but confirm to be sure. Any benefits paid after death must be returned.

9. Notify Banks and Financial Institutions

Contact all banks, credit unions, brokerage firms, and credit card companies. Provide a death certificate and ask them to freeze accounts. This prevents unauthorized access and protects the estate from fraud.

10. Contact Insurance Companies

Notify life insurance providers, health insurance carriers, and any other insurers. Begin the claims process for life insurance benefits, which typically pass directly to beneficiaries outside of probate.

11. Cancel Subscriptions and Services

Stop recurring charges for utilities, subscriptions, memberships, and services that are no longer needed. This prevents unnecessary expenses from draining estate funds.

12. Notify Creditors

Inform mortgage lenders, credit card companies, and anyone the deceased owed money to. Don’t pay debts out of pocket—these should be settled through the estate during probate.

Within the First Month

13. Meet with an Estate Attorney

Consult with a probate or estate planning attorney to understand the legal requirements in your state and begin the probate process if necessary. An attorney can guide you through executor duties and help avoid costly mistakes.

14. File for Probate (If Applicable)

If the estate requires probate, file the petition with the appropriate court and begin the process of obtaining Letters Testamentary or Letters of Administration.

15. Notify the IRS and State Tax Authorities

The estate may need to obtain a federal Employer Identification Number (EIN). You’ll also need to file the deceased’s final income tax return and, if applicable, an estate tax return.

What NOT to Do After Someone Dies

Just as important as what to do is what to avoid:

- ❌ Don’t use the Power of Attorney to access accounts or make decisions

- ❌ Don’t distribute assets before going through probate (unless they’re clearly non-probate assets)

- ❌ Don’t pay estate debts with your own money—you’re not personally responsible

- ❌ Don’t throw away documents or records—they may be needed for tax filings or disputes

- ❌ Don’t make major decisions alone—consult with family members and professionals

The Importance of Estate Planning: More Than Just a Power of Attorney

A Power of Attorney is a critical component of any estate plan, but it’s only one piece of the puzzle. Comprehensive estate planning ensures your wishes are honored both during your life and after your death—and it spares your loved ones from unnecessary stress, confusion, and legal battles.

Why Estate Planning Matters

Without a proper estate plan, your family may face:

- Lengthy probate delays that tie up assets for months or years

- Court-appointed decision makers who may not know your wishes

- Family disputes over property, finances, and guardianship

- Higher taxes and fees that reduce what your beneficiaries receive

- Guardianship proceedings if you become incapacitated without a plan

Estate planning isn’t just for the wealthy. Anyone with assets, dependents, or specific wishes about their care and property should have a plan in place.

Essential Documents in a Complete Estate Plan

A well-rounded estate plan typically includes:

1. Last Will and Testament

Names your executor, specifies how assets should be distributed, and designates guardians for minor children. This is where you bridge the gap left when your POA ends at death.

2. Power of Attorney (Financial)

Authorizes someone to manage your finances if you’re unable to do so while you’re alive. Remember: this ends at death.

3. Medical Power of Attorney (Healthcare Proxy)

Designates someone to make medical decisions on your behalf if you’re incapacitated. Often paired with a living will or advance directive.

4. Living Will or Advance Directive

Specifies your wishes regarding end-of-life care, such as life support, resuscitation, and organ donation.

5. Revocable Living Trust

Allows assets to pass to beneficiaries without going through probate. A trust can also provide for management of assets if you become incapacitated, offering more flexibility than a POA alone.

6. Beneficiary Designations

Ensure all retirement accounts, life insurance policies, and bank accounts have current, correct beneficiary designations. These override what’s in your will.

Appointing an Executor Separately from Your POA Agent

Many people assume that naming someone as their Power of Attorney agent automatically makes that person their executor. This is not true. These are separate roles that must be designated in separate documents:

- Power of Attorney = manages your affairs while you’re alive

- Executor (in your will) = manages your estate after death

You can name the same person for both roles, but you must do so explicitly in both the POA and the will. If you only name them in one document, they won’t have authority to act in the other capacity.

Keep Your Estate Plan Updated

Life changes—marriages, divorces, births, deaths, relocations, and changes in financial circumstances all affect your estate plan. Review your documents every 3–5 years or whenever a major life event occurs. An outdated plan can be just as problematic as having no plan at all.

For example:

- Your named agent or executor may have moved, become ill, or passed away

- Beneficiary designations may no longer reflect your wishes

- Changes in tax law may impact your strategy

- New assets or debts may need to be addressed

When to Seek Professional Help

While some simple estate planning documents can be created using online templates, complex situations benefit from professional guidance. Consider consulting an estate planning attorney if:

- Your estate is valued over $1 million

- You own real estate in multiple states

- You have a blended family or complicated family dynamics

- You own a business

- You want to minimize estate taxes

- You have concerns about a family member’s ability to manage money

- You need special needs planning for a dependent

An experienced attorney can ensure your documents are legally valid, properly executed, and tailored to your specific situation and state laws.

Working with a wills and estates lawyer ensures your documents are legally sound and tailored to your specific family and financial situation.

Frequently Asked Questions About Power of Attorney After Death

Can I still use a POA after the person dies?

No. A Power of Attorney becomes completely invalid the moment the principal dies. Any attempt to use POA authority after death is illegal and can be prosecuted as fraud or theft, even if your intentions are good.

Does durable power of attorney stay valid after death?

No. While a durable POA remains valid if the principal becomes incapacitated, it still terminates immediately upon death. “Durable” only refers to mental or physical incapacity during life—not death.

Is irrevocable power of attorney valid after death?

No. Even though an irrevocable POA cannot be canceled by the principal while they’re alive, it still ends the moment they die. No type of POA survives death.

Who takes over when POA ends at death?

The executor named in the will takes over, but only after being officially appointed by the probate court and receiving Letters Testamentary. If there’s no will, the court appoints an administrator who receives Letters of Administration.

How is an executor different from a POA?

A POA agent acts on behalf of a living person and has no authority after death. An executor manages the deceased’s estate, pays debts, and distributes assets according to the will—but only after court appointment.

Can I be both an agent and executor?

Yes, but only if you’re explicitly named in both the Power of Attorney document and the will. Being named as one does not automatically make you the other.

Does power of attorney have to pay bills after death?

No. Once the principal dies, the agent has no authority or obligation to pay bills. The executor handles all debts through the probate process using estate funds, not personal money.

Can I withdraw money from a deceased person’s bank account?

Only if you’re a joint account holder with right of survivorship or the named beneficiary on a payable-on-death account. Otherwise, only the court-appointed executor with Letters Testamentary can access the account.

Does power of attorney have more power than executor?

No. They serve different purposes. The POA agent has authority only while the person is alive. The executor has authority only after death and must follow probate court rules. Neither outranks the other—they operate in different timeframes.

Who notifies Social Security when someone dies?

Typically the funeral home reports the death to Social Security, but family members should confirm this happened. Call the SSA at 1-800-772-1213 to verify. Any benefits paid after death must be returned.

What is abuse of power of attorney after death?

Abuse occurs when someone continues using POA authority after it has terminated—such as withdrawing funds, transferring property, or signing documents after the principal’s death. This is illegal and can result in civil and criminal penalties.

What happens if your power of attorney dies before you?

If your agent dies and you didn’t name a successor agent in the POA document, the POA becomes invalid. You’ll need to execute a new POA if you’re still mentally competent. If not, your family may need to pursue guardianship through the courts.

How long does power of attorney last after death?

Zero time. It ends instantly at the moment of death with no grace period. There is no situation where POA authority continues after the principal passes away.

What should I do immediately after someone dies if I was their POA?

Stop using the POA immediately, secure the deceased’s property, locate important documents like the will, notify banks and creditors, and help the family begin the probate process. Do not access accounts or make financial decisions.

Conclusion

So, is a Power of Attorney valid after death? The answer is definitively no. Regardless of type—general, durable, lasting, or irrevocable—all Powers of Attorney terminate the instant the principal dies. At that moment, legal authority transfers to the executor named in the will or a court-appointed administrator.

Understanding this boundary is essential for anyone serving as an agent or planning their own estate. Misusing POA authority after death can lead to serious legal consequences, even when done with good intentions. The key is preparation: create a comprehensive estate plan that includes both a Power of Attorney for life and a will that names an executor for after death.

If you’re navigating the loss of a loved one or need help setting up your own estate plan, consult with an experienced estate planning attorney who can guide you through the process and ensure all documents are properly executed.

Comments