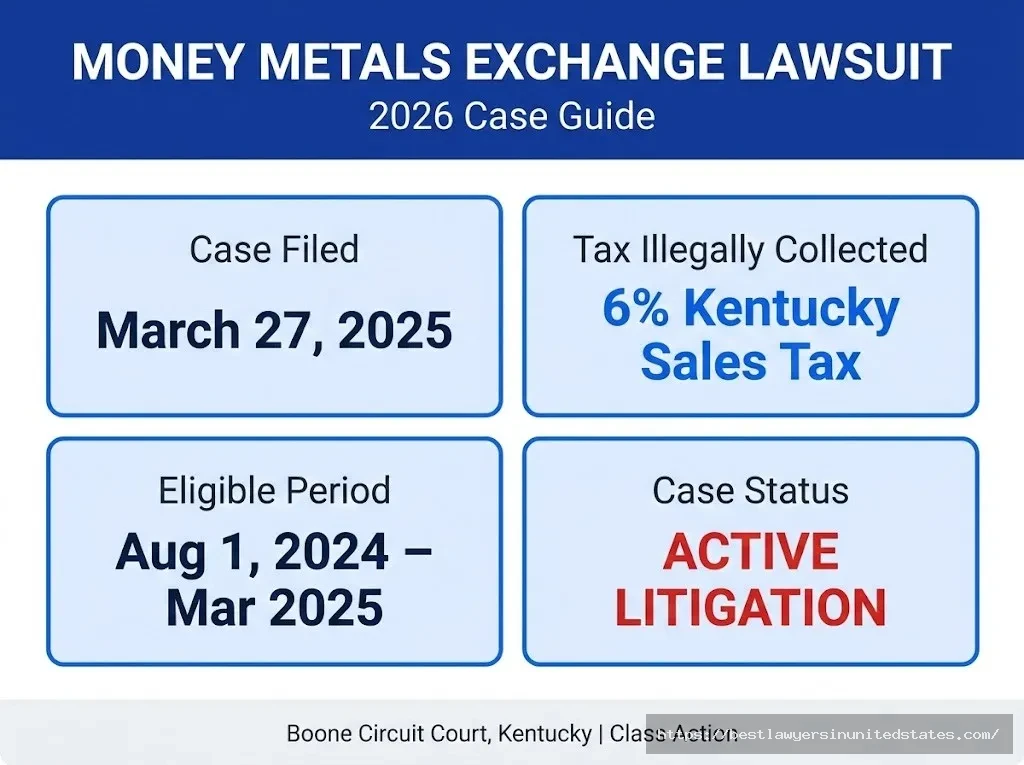

The Money Metals Exchange lawsuit is a class-action case filed against Kentucky Governor Andy Beshear, the Commonwealth of Kentucky, and the Kentucky Department of Revenue for illegally collecting a 6% sales tax on purchases of gold and silver — even after Kentucky law explicitly exempted those purchases. Money Metals Exchange joined three Kentucky taxpayers in filing the complaint on March 27, 2025, in Boone Circuit Court.

No settlement has been finalized as of March 2026, but the underlying law (Kentucky House Bill 2) already gives Kentuckians a legal path to recover every dollar of sales tax they paid, plus interest and potentially attorney’s fees. This guide explains exactly what happened, who qualifies, how to pursue your refund, and where the case stands today. Ancient Nutrition Lawsuit

Quick Answer: If you bought gold or silver in Kentucky after August 1, 2024 and paid a 6% state sales tax, you may have been illegally taxed. Kentucky law now gives you the right to sue the state for a full refund with interest. Money Metals Exchange and three Kentucky residents filed a class-action lawsuit on your behalf. The case is active, no general claim deadline has been set yet, but you should document your purchases now.

Lawsuit Overview

| Key Detail | Information |

|---|---|

| Lawsuit Name | Money Metals Exchange et al. v. Governor Andy Beshear et al. |

| Court Filed | Boone Circuit Court, Kentucky |

| Date Filed | March 27, 2025 |

| Plaintiffs | Money Metals Exchange, Jill Stahl Huston, Stacie Earl, Karen Strayer |

| Defendants | Gov. Andy Beshear, Commonwealth of Kentucky, Kentucky Department of Revenue |

| Type | Class-action lawsuit |

| Tax at Issue | Kentucky 6% sales tax on gold and silver purchases |

| Tax Illegal From | August 1, 2024 (when KY HB 8 exemption took effect) |

| Relief Sought | Full tax refund + interest + attorney’s fees + injunction |

| Settlement Status | Active litigation — no settlement finalized yet |

| Represented by | Sound Money Defense League, Money Metals Exchange |

What Is the Money Metals Exchange Lawsuit About?

Background of the Case

This lawsuit isn’t about a defective product or corporate wrongdoing by Money Metals Exchange. It’s actually the opposite: Money Metals Exchange is the hero of this story, standing up against what they say is an illegal government money grab.

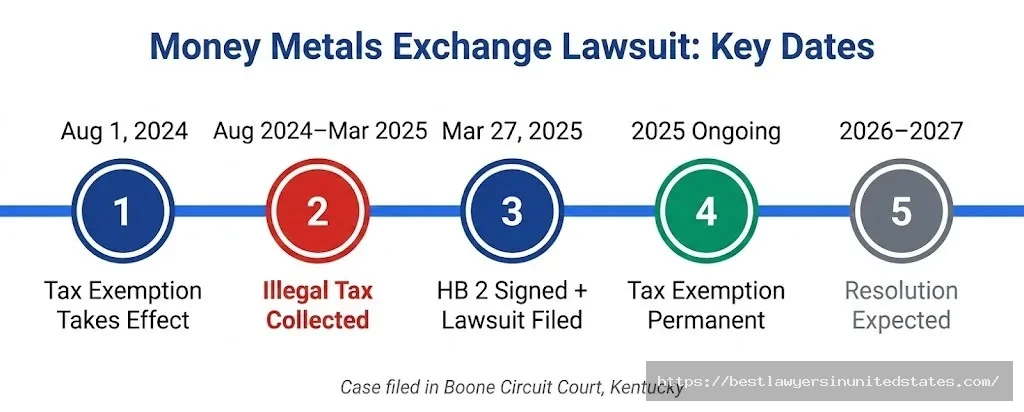

Here’s what happened. In 2024, the Kentucky state legislature passed House Bill 8, which removed the state’s 6% sales tax on purchases of gold and silver coins, bars, and rounds. Under that law, the exemption went into effect on August 1, 2024. But Governor Andy Beshear refused to accept it.

Beshear claimed he could use a “line-item veto” to strike the precious metals exemption from the bill. The problem? Kentucky’s constitution only allows line-item vetoes on appropriations bills. Kentucky Attorney General Russell Coleman reviewed the situation and concluded Beshear’s veto was unconstitutional and had no legal force. The law was enrolled as a statute. The sales tax exemption was on the books.

And yet, the Governor directed his Department of Revenue to keep collecting the 6% tax anyway — threatening dealers with prosecution if they didn’t comply. That put businesses like Money Metals Exchange in an impossible spot: charge customers a tax that isn’t legally owed, or face government enforcement.

Money Metals chose to fight. In March 2025, the legislature passed House Bill 2, which explicitly reinforced the exemption, overrode Beshear’s veto 80–19 in the House and 31–6 in the Senate, and — critically — created a legal path for taxpayers to sue the state for a refund of every dollar illegally collected, with interest and penalties.

Hours after that bill became law, Money Metals Exchange and three Kentucky residents filed this class-action lawsuit.

Who Filed the Lawsuit?

The lawsuit was filed jointly by:

- Money Metals Exchange — an Idaho-based precious metals dealer and one of the largest in the United States, recently named “Best Overall” online precious metals dealer by Investopedia. CEO Stefan Gleason has been a vocal advocate for sound money policies for years.

- Jill Stahl Huston — a Kentucky taxpayer who paid the sales tax on precious metals purchases

- Stacie Earl — a Kentucky taxpayer affected by the illegal tax collection

- Karen Strayer — a third Kentucky taxpayer who paid the disputed tax

The case is backed by the Sound Money Defense League, a national non-partisan organization that works to restore gold and silver as constitutional money at the state level.

Timeline of Key Events

| Date | Event | Details |

|---|---|---|

| 2020 | Money Metals advocacy begins | Money Metals Exchange begins pushing Kentucky to end precious metals sales tax |

| 2024 (Spring) | HB 8 passes | Kentucky legislature removes 6% sales tax on gold/silver in omnibus bill |

| August 1, 2024 | Tax exemption effective | Gold/silver purchases legally exempt from sales tax in Kentucky |

| Aug–March 2024–25 | Tax illegally collected | Beshear directs Department of Revenue to keep collecting tax despite the law |

| January 2025 | HB 2 introduced | Rep. TJ Roberts and Rep. Steve Doan file legislation to reinforce exemption and add penalty provisions |

| March 27, 2025 | HB 2 signed into law | Legislature overrides Beshear’s veto; law passes 80–19 in House, 31–6 in Senate |

| March 27, 2025 | Lawsuit filed | Money Metals Exchange + 3 taxpayers file class-action in Boone Circuit Court |

| Late 2025 | Case progresses | Litigation ongoing in Kentucky state court |

| 2026 (ongoing) | Active litigation | No settlement finalized; case continues through the courts |

What Are the Allegations?

The lawsuit makes several specific legal claims against Governor Beshear and the Kentucky Department of Revenue:

- Unconstitutional veto: Beshear used a line-item veto — which Kentucky’s constitution only permits on appropriation bills — to strike a non-appropriation tax exemption. The AG called it a constitutional nullity.

- Defying the law: Despite the AG opinion, the court’s enrolled statute, and the legislature’s clear intent, the Department of Revenue continued enforcing a tax that wasn’t legally owed.

- Coercion of businesses: The state threatened gold and silver dealers with prosecution if they refused to collect and remit the illegal tax, putting dealers in an impossible legal position.

- Unjust enrichment: The state collected millions of dollars in sales taxes that were not legally authorized, at the expense of Kentucky taxpayers and businesses.

The lawsuit seeks a full refund of all sales taxes collected on precious metals purchases from August 1, 2024 through the resolution of the case, plus statutory interest, penalties on state officials, and attorney’s fees — all as authorized by House Bill 2.

Who Qualifies?

Eligibility Requirements

Quick Answer: You likely qualify if you bought gold or silver in Kentucky (or had it shipped to a Kentucky address) after August 1, 2024 and were charged Kentucky’s 6% sales tax.

| Requirement | Details | Documentation Needed |

|---|---|---|

| Kentucky purchaser | You bought precious metals with a Kentucky delivery address | Purchase receipt or order confirmation |

| Purchase after August 1, 2024 | The tax exemption took effect August 1, 2024 | Date shown on receipt |

| Sales tax was charged | You actually paid the 6% Kentucky sales tax | Receipt showing tax line item |

| Eligible metals | Gold or silver coins, bars, rounds, or bullion | Description on receipt |

| Not a reseller for exempt purpose | Purchased for personal investment, saving, or use | General declaration |

You don’t need to have purchased from Money Metals Exchange. The class includes any Kentucky taxpayer who paid the illegal sales tax on precious metals after August 1, 2024 — regardless of which dealer they used.

What Metals Are Covered?

Kentucky’s exemption under House Bill 8 (and reinforced by House Bill 2) covers:

| Metal Type | Examples | Covered? |

|---|---|---|

| Gold | Coins, bars, rounds, ingots valued by metal content | ✅ Yes |

| Silver | Coins, bars, rounds, ingots valued by metal content | ✅ Yes |

| Platinum | Bars, coins valued by metal content | ✅ Yes |

| Palladium | Bars, coins valued by metal content | ✅ Yes |

| Collectible coins | Coins valued primarily for rarity, not metal | ❌ Likely excluded |

| Jewelry | Gold/silver jewelry sold as merchandise | ❌ Excluded |

| Scrap metal | Metals not used as money or investment | ❌ Likely excluded |

The law defines bullion as “bars, ingots, or coins made of gold, silver, platinum, palladium, or a combination of these metals, valued based on the content of the metal and not its form.” Ford EcoBoost Class Action Lawsuit

Who Does NOT Qualify?

You’re likely not part of this class if:

- ❌ You purchased precious metals outside of Kentucky with no Kentucky delivery

- ❌ Your purchase was before August 1, 2024 (when the exemption first took effect)

- ❌ You bought jewelry or collectibles, not investment-grade bullion

- ❌ You received a sales tax refund from the dealer already

- ❌ You’re a business that collected and remitted the tax as a dealer (that’s a separate claim)

How to Prove Your Claim

| Document Type | Why It’s Needed | Where to Find It | If You Don’t Have It |

|---|---|---|---|

| Purchase receipt/confirmation | Proves you made a qualifying purchase | Email inbox, dealer account portal | Bank/credit card statement showing the purchase |

| Receipt with tax line | Shows sales tax was actually charged | Same as above | Contact dealer for a copy |

| Proof of Kentucky delivery | Shows you’re in the class | Shipping address on order | Statement showing Kentucky billing address |

| Bank/credit card statement | Confirms payment amount | Bank online portal | Request from bank |

How Much Money Could You Get Back?

Since no settlement has been finalized, exact payout amounts haven’t been determined by a court. But here’s what Kentucky’s House Bill 2 actually entitles you to:

What the Law Guarantees

| Recovery Type | Details |

|---|---|

| Full tax refund | 100% of the 6% sales tax you paid on eligible purchases |

| Statutory interest | Interest accrues on the amount illegally taken |

| Penalties on officials | HB 2 allows penalties against Department of Revenue officials who violated the law |

| Attorney’s fees | If the lawsuit succeeds, attorney’s fees may be covered by the state |

Estimating Your Refund

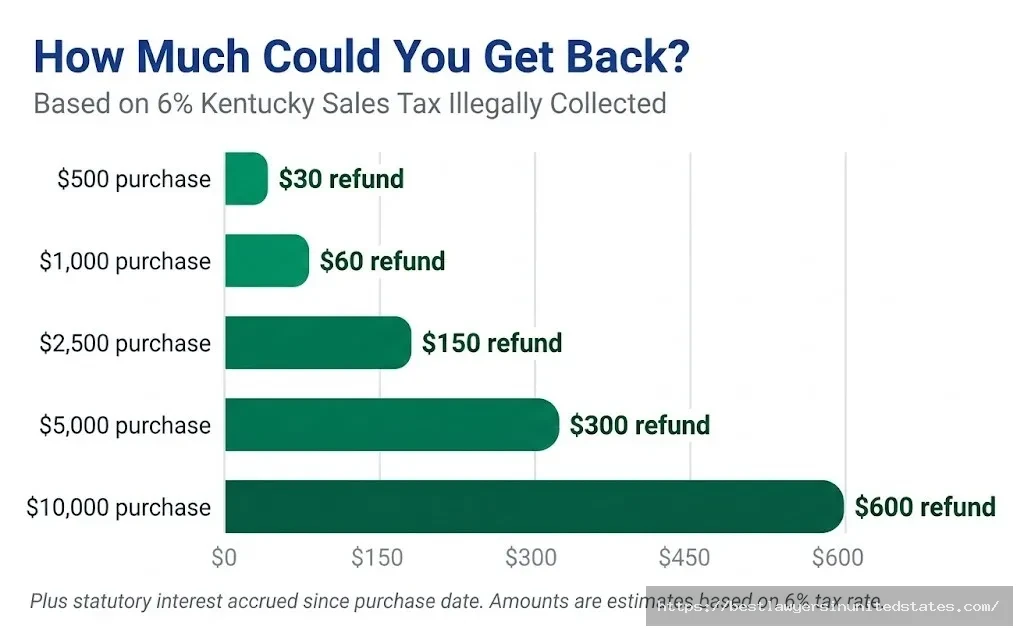

Your personal refund amount depends entirely on how much you spent and how much tax you paid. It’s straightforward math:

- If you spent $1,000 on gold and paid 6% tax → potential refund of $60 + interest

- If you spent $5,000 on silver and paid 6% tax → potential refund of $300 + interest

- If you spent $10,000 on bullion and paid 6% tax → potential refund of $600 + interest

Interest has been accruing since the date you paid, which could add meaningful additional recovery for purchases made in late 2024.

The total amount at stake statewide could be significant. Kentucky is a large state, and the Department of Revenue collected this tax for roughly seven months after it was legally abolished — from every dealer selling to Kentucky customers.

Current Lawsuit Status (as of March 2026)

Where Things Stand

The case remains active litigation in Boone Circuit Court, Kentucky. As of early 2026, no settlement has been reached and no final judgment has been entered. The class has not yet been certified by a court, though the class action complaint was filed in March 2025.

Importantly, the underlying policy fight has already been won: Kentucky is now the 44th state in the country to exempt precious metals from sales taxes. The Governor no longer has authority to collect the tax. The sales tax exemption is fully in effect.

What remains unresolved is the backward-looking question: Who owes what to the taxpayers and businesses that were illegally charged for those seven-plus months between August 1, 2024 and March 27, 2025?

Recent Developments

- November 2025: The 2026 Sound Money Index confirmed Kentucky as the 44th state to end precious metals sales taxes, crediting the multi-year effort led partly by Money Metals Exchange

- Ongoing 2025–2026: Litigation continues in Boone Circuit Court; class certification proceedings and discovery are expected

- No settlement announced: As of publication, no settlement agreement, claim portal, or deadline has been publicly announced

What Happens Next?

The court will need to:

- Certify the class — officially recognize the lawsuit as a class action representing all affected Kentucky taxpayers

- Resolve the legal questions — determine the full scope of the state’s liability under HB 2

- Either reach a settlement or go to trial — the state may settle to avoid a protracted court battle, or the case could proceed to judgment

- Establish a claims process — once liability is established, there will likely be a formal process for class members to document their purchases and receive refunds

You should start gathering and saving your documentation now, before receipts become harder to find.

How to Protect Your Potential Claim Right Now

Even though no formal claims process exists yet, there are concrete steps you can take today.

Step 1: Locate Your Purchase Records Go through your email inbox and search for order confirmations from precious metals dealers. Look for purchases with a Kentucky delivery address dated after August 1, 2024. Save copies in a dedicated folder.

Step 2: Check Your Receipts for Sales Tax Look at the line items on each receipt. Did the dealer charge Kentucky sales tax (typically shown as 6%)? If yes, that’s the amount you may be owed back.

Step 3: Organize by Date and Dealer Make a simple list or spreadsheet: dealer name, purchase date, total spent, tax charged. This will make filing a claim much easier once the process opens.

Step 4: Download Statements Pull your credit card and bank statements from August 2024 through March 2025. These serve as backup proof if you can’t find receipts.

Step 5: Check the Official Money Metals Website Visit moneymetals.com for the latest updates on the lawsuit. Money Metals Exchange is a lead plaintiff and will post updates as the case progresses.

Step 6: Stay Informed Watch for announcements about class certification and any formal claims process. Once a settlement or judgment occurs, there will be a defined window to submit your claim.

Critical Deadlines Table

| Deadline Type | Date/Status | What It Means for You |

|---|---|---|

| Tax exemption effective | August 1, 2024 | Purchases after this date may be eligible |

| Lawsuit filed | March 27, 2025 | Class action covers this period and beyond |

| Class certification | TBD — court pending | Official class recognition expected in 2026 |

| Claim submission deadline | Not yet set | Will be announced once case resolves |

| Settlement/judgment | TBD | Could come in 2026 or later |

There is no claim deadline yet. But don’t wait to gather your documentation — records become harder to find over time.

Do You Need a Lawyer to Participate?

Quick Answer: No. If a settlement or court judgment is reached, participating in the class action generally doesn’t require you to hire your own attorney. The class attorneys handle the litigation on your behalf.

How Class Actions Work

In a class action like this one, the attorneys representing the class — here supported by the Sound Money Defense League and Money Metals Exchange — handle all the legal work. If the case results in a settlement or judgment, affected Kentuckians will typically receive notice and have an opportunity to file a claim (similar to a rebate or refund form) without hiring personal legal counsel.

You only need your own attorney if you want to:

- Opt out of the class to pursue your own individual claim

- Object to any proposed settlement terms

- File a related but separate claim not covered by the class

When to Consider Legal Help

Talk to an attorney if:

- You’re a precious metals dealer who collected and remitted the tax on behalf of customers — your situation is more complex

- You have very large purchases and want to explore an individual claim strategy

- You want to stay current on the class certification timeline

For general questions about your eligibility, contact the Sound Money Defense League at SoundMoneyDefense.org or visit Money Metals Exchange’s news center at moneymetals.com/news. You can also contact [email protected] for attorney referrals related to this case.

Money Metals Exchange Lawsuit vs. Similar Cases

How This Compares to Other Precious Metals Lawsuits

| Case | Type | Settled | Payout | Who Benefited |

|---|---|---|---|---|

| Money Metals v. Beshear (KY) | Gov’t illegal tax collection | ❌ Ongoing | TBD — 6% tax refund + interest | KY precious metals buyers (Aug 2024–Mar 2025) |

| Platinum/Palladium Price-Fixing | Antitrust vs. Goldman Sachs, HSBC, BASF, ICBC | ✅ $20M settled Jan 2025 | Varies by claim | Futures traders 2008–2014 |

| Metals.com / Chase Metals CFTC | Fraud/receivership | ✅ Partial recovery | Varies | Defrauded precious metals investors |

| Stuppler v. Money Metals (CA) | Business dispute | Pending | TBD | B2B commercial dispute |

What Makes This Case Unique

Unlike most precious metals lawsuits — which typically involve price manipulation or corporate fraud — this case is a constitutional challenge to government overreach. Money Metals Exchange is suing a sitting governor for directing his department to collect a tax that state law had already abolished.

It’s also unusual in that the underlying legal question has largely been resolved: the sales tax exemption is now definitively in effect. The remaining fight is about making taxpayers whole for the period of illegal collection.

The case is also unusual in that the lawsuit vehicle itself (HB 2) was passed specifically to enable this refund claim — the legislature essentially handed taxpayers a legal sword and told them to use it.

Frequently Asked Questions

What exactly is the Money Metals Exchange lawsuit about?

Quick Answer: It’s a class-action lawsuit claiming the Kentucky state government illegally collected a 6% sales tax on gold and silver purchases after state law exempted those purchases.

Money Metals Exchange, alongside three Kentucky residents, sued Governor Andy Beshear and the Kentucky Department of Revenue in March 2025. The state had continued collecting a precious metals sales tax after the legislature passed a law abolishing it — and even after the Attorney General said the governor’s veto of that law was unconstitutional.

Is Money Metals Exchange in trouble? Are they being sued?

Quick Answer: No. Money Metals Exchange is a plaintiff — they filed the lawsuit, they didn’t get sued.

In this case, Money Metals is fighting on the consumer side against the state government. There is a separate, unrelated business dispute (Stuppler & Company v. Money Metals Exchange) in California federal court, but that’s a commercial dispute between businesses, not a consumer class action.

Who is eligible to join this class action?

Quick Answer: Any Kentucky resident or buyer who paid Kentucky’s 6% sales tax on gold, silver, or other precious metals bullion after August 1, 2024.

You don’t need to have bought from Money Metals Exchange specifically. Any dealer who collected Kentucky sales tax on bullion purchases after August 1, 2024 was collecting a tax that the law said wasn’t owed.

How much money could I get back?

Quick Answer: You’d get back the full 6% sales tax you paid, plus interest that has been accruing since your purchase.

There’s no cap on your individual refund — it’s calculated based on what you actually paid. A $1,000 purchase means a $60 tax refund potential; a $10,000 purchase means $600. Interest adds to that.

Is there a deadline to file a claim?

Quick Answer: No formal claim deadline exists yet. The case is still in active litigation.

Once the case is resolved — either through settlement or a court ruling — a claims process will be announced with a specific deadline. Start gathering your documentation now so you’re ready.

What documents do I need?

Quick Answer: Receipts or order confirmations showing a Kentucky delivery address, the purchase date after August 1, 2024, and a Kentucky sales tax charge.

Bank and credit card statements work as backup proof if you can’t find the original receipts. Contact your dealer directly if you need copies of past orders.

Do I need to hire a lawyer to participate?

Quick Answer: No. The class attorneys handle the litigation. Once resolved, there will likely be a simple claims process.

If you want to opt out and pursue your own separate claim, or if you’re a dealer seeking recovery of tax you remitted on behalf of customers, you may want individual legal counsel.

What happened to Kentucky’s precious metals tax?

Quick Answer: It’s gone. As of March 27, 2025, Kentucky’s 6% sales tax on precious metals is firmly and permanently abolished.

Kentucky is now the 44th state to exempt gold and silver purchases from sales tax. The ongoing lawsuit is about recovering taxes that were wrongly collected in the past — not about stopping the tax going forward. Target Class Action Lawsuit 2026

Was the Governor’s veto legal?

Quick Answer: No — the Kentucky Attorney General ruled it unconstitutional.

Kentucky’s constitution only permits line-item vetoes of appropriations bills. House Bill 8 was not an appropriations bill, so the AG concluded the veto was a constitutional nullity. The legislature agreed and enrolled the statute over Beshear’s objection.

What is House Bill 2 and why does it matter?

Quick Answer: HB 2 is the 2025 Kentucky law that both reinforced the precious metals tax exemption and gave taxpayers an explicit legal right to sue the state for a refund of illegally collected taxes.

HB 2 specifically authorizes recovery of the full tax amount plus interest, and it allows for penalties against state officials who violated the exemption. This legislation is the legal foundation for the current class-action lawsuit.

What if I bought precious metals from Money Metals Exchange but live outside Kentucky?

Quick Answer: This lawsuit is specific to Kentucky’s sales tax and only covers purchases shipped to Kentucky addresses.

If you live in another state and were charged a sales tax on precious metals that your state has also abolished, you may have a separate state-level claim. Contact your state’s Department of Revenue or an attorney familiar with sound money legislation in your state.

What did Money Metals Exchange do during the period of illegal tax collection?

Quick Answer: They continued collecting the tax to avoid prosecution, but made clear they believed it was illegal — and filed this lawsuit to recover those funds for customers.

Stefan Gleason, Money Metals CEO, said the company was “put in an untenable position” by Beshear’s actions, but refused to simply absorb the situation. Filing suit was their response.

When will the lawsuit be resolved?

Quick Answer: There’s no official timeline, but class action cases of this nature typically take one to three years from filing to resolution.

The case was filed in March 2025. Class certification, discovery, and either settlement negotiations or trial proceedings take time. A resolution in 2026 or 2027 is plausible, but not guaranteed.

Will I be automatically included in the class?

Quick Answer: If you meet the eligibility criteria, you’ll likely be automatically included once the class is certified — you generally don’t have to opt in.

In most class actions, you’re automatically part of the class if you meet the definition. You’d have to affirmatively opt out if you want to pursue your own separate claim instead.

Where can I track updates on this case?

Quick Answer: Check moneymetals.com/news and soundmoneydefense.org for official updates from the plaintiffs.

You can also monitor Boone Circuit Court records in Kentucky for official court filings. No government settlement website has been established yet.

What if I threw away my receipts?

Quick Answer: Bank and credit card statements can substitute for receipts in most class action claims processes.

Log in to your bank or credit card account and download statements from August 2024 through March 2025. Look for charges to precious metals dealers. These records can establish the amount you paid even without the original receipt.

Should I do anything right now?

Quick Answer: Yes — gather your documentation while it’s still easy to find.

Pull together purchase confirmations, receipts, and bank statements from August 1, 2024 through March 2025. Save them somewhere safe. Sign up for updates at moneymetals.com. When a formal claims process opens, you’ll be ready.

What This Lawsuit Means for Precious Metals Investors

This case is about more than one state’s sales tax. It’s part of a broader national movement — now supported by 44 states — to treat gold and silver as constitutional money rather than taxable consumer goods. As consumer rights lawyers who handle class action and consumer protection cases know well, government overreach in taxation creates real financial harm to real people.

The broader lesson for precious metals buyers: know your state’s tax laws on bullion purchases. In most states, buying gold or silver is now tax-free. And if you’ve been charged taxes that weren’t owed, you may have options under state law that go beyond waiting for a class action to resolve.

If you’re exploring precious metals investing and want to understand your rights, or if you think you may have been over-taxed on investments in other contexts, understanding consumer protection law is a smart starting point.