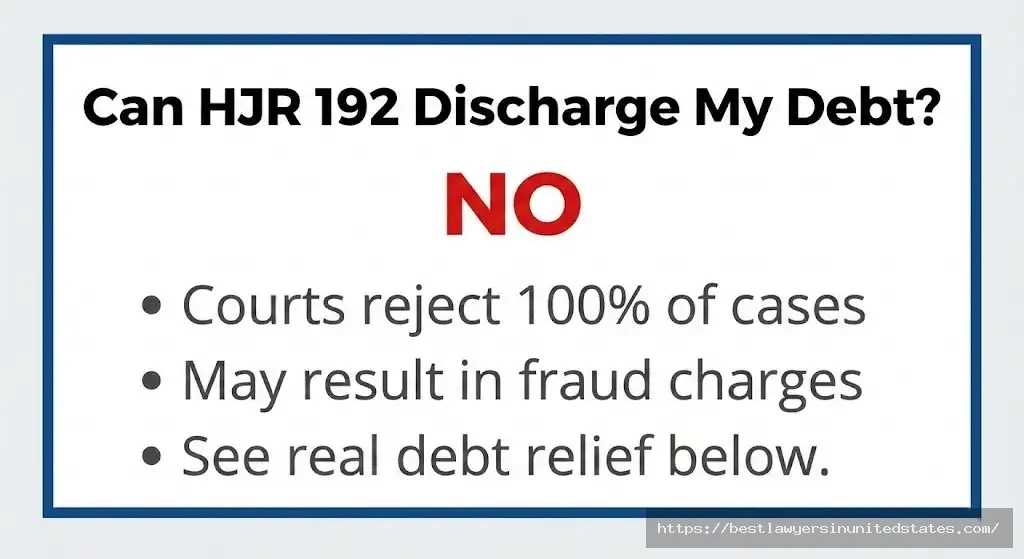

⚠️ CRITICAL LEGAL ALERT: If someone told you that HJR 192 (House Joint Resolution 192, Public Law 73-10) allows you to legally discharge your personal debts, they are dangerously wrong. Federal courts have rejected this theory in every single case for 90 years. Attempting to use HJR 192 to avoid debt payments can result in fraud charges, damaged credit, and legal penalties.

Last Updated: January 6, 2026

Reviewed by: Legal Research Team | Constitutional Law Division

Download Our Free HJR 192 Legal Guide

Get the complete breakdown in PDF format. Our comprehensive 12-page guide includes the full text of HJR 192, Supreme Court case summaries from Perry v. United States (1935), a timeline of federal court rejections, and a scam prevention checklist. Perfect for offline reading, legal research, or sharing with family members who may have encountered debt discharge myths. Download your free copy below—no email required.

This resource summarizes 90 years of legal precedent and includes citations to 31 U.S.C. § 5118, official court documents, and federal debt relief programs. Last updated: January 2026.

Read More: DailyNewsLaw

What You Need to Know Right Now

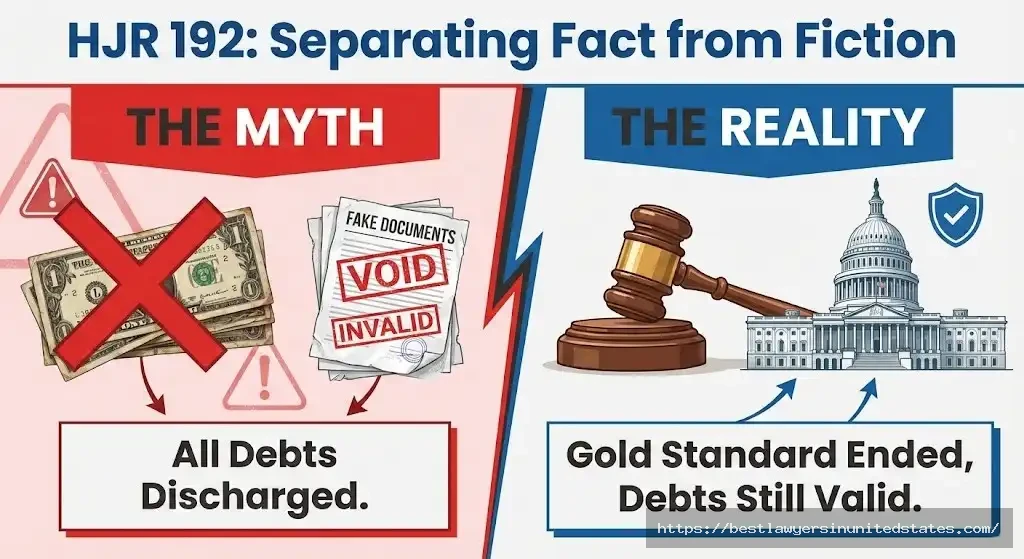

The Bottom Line: HJR 192, passed in 1933, ended the requirement for debts to be paid in gold. It did NOT create a system for discharging personal debts, and courts have consistently ruled that attempting to use it this way is frivolous and potentially fraudulent.

The 1933 Law: What HJR 192 Actually Did

The Historical Crisis

In June 1933, the United States faced economic catastrophe. The Great Depression had devastated the banking system, unemployment exceeded 25%, and desperate Americans hoarded gold, draining federal reserves. President Franklin D. Roosevelt and Congress took drastic action: they suspended the gold standard.

House Joint Resolution 192 (codified as Public Law 73-10, 48 Stat. 112) declared that:

“Every provision contained in or made with respect to any obligation which purports to give the obligee a right to require payment in gold or a particular kind of coin or currency, or in an amount in money of the United States measured thereby, is declared to be against public policy.”

What This Means in Plain English

Before HJR 192: If you borrowed $1,000 in 1920, your contract might have included a “gold clause” requiring repayment in gold coins or their exact gold-value equivalent. When gold prices changed, this could make your debt balloon unexpectedly.

After HJR 192: Those gold clauses became void. Debts had to be paid “dollar for dollar” in whatever legal tender (paper money) was current at the time, protecting borrowers from gold price fluctuations.

What it did NOT do: Create a “government fund” to pay your debts, allow you to “discharge” debts without payment, or give citizens a “secret” right to cancel obligations.

HJR 192 vs. The Debt Discharge Myth: Side-by-Side

| What HJR 192 Actually Says | What the Myth Claims |

|---|---|

| Voided gold clauses in existing contracts | Claims all debts are “prepaid” by the government |

| Required payment in U.S. legal tender (dollars) | Says you can send a “letter of discharge” to cancel debt |

| Applied only to gold-backed obligations | Suggests it works for credit cards, mortgages, car loans |

| Upheld creditors’ right to collect in dollars | Implies creditors have no legal right to collect at all |

| Court Status: Upheld by Supreme Court in Perry v. United States (1935) | Court Status: Rejected in 100+ federal cases (1935-2025) |

Why Courts Reject HJR 192 Debt Discharge Theories

Landmark Supreme Court Case: Perry v. United States (1935)

In Perry v. United States, 294 U.S. 330 (1935), the Supreme Court addressed HJR 192 directly. John Perry held a Liberty Bond with a gold clause promising payment in gold or its equivalent. After HJR 192, the government offered to pay in devalued dollars instead.

What the Court Held:

- The government could NOT be forced to pay in gold

- Perry was entitled to payment in dollars (legal tender)

- The resolution protected the “integrity of the public debt” by preventing gold-backed obligations from becoming unpayable

- Critically: The Court confirmed that debts must still be paid—just in dollars, not gold

What the Court Did NOT Hold:

- That debts are “automatically discharged”

- That individuals have a “government account” to pay their bills

- That HJR 192 voids contractual obligations

Modern Federal Court Rejections

Since 1935, federal courts have dismissed HJR 192 debt discharge claims as “frivolous” in every case. Here are key examples:

Sanford v. Robins Federal Credit Union (M.D. Ga. 2012)

Facts: Plaintiff sent “electronic funds transfer instruments” to pay off car loans, claiming HJR 192 meant the government would cover his debts.

Court’s Ruling:

“Plaintiff’s reference to H.J. Res. 192… is insufficient to state a claim… Plaintiff appears to advance a watered-down version of claims other plaintiffs have unsuccessfully attempted via Public Law 73-10, such as the ‘vapor money’ theory, ‘unlawful money’ theory, or ‘redemption’ theory… Courts have widely rejected arguments seeking relief pursuant to theories based on Public Law 73-10.”

Outcome: Case dismissed as frivolous.

Stokes v. Santander Consumer USA (M.D. Ala. 2018)

Facts: James Stokes claimed he sent a “money order” to his auto lender under HJR 192 to “discharge” his $18,479.69 loan. When the lender rejected it, he sued.

Court’s Ruling:

“No facts asserted in Plaintiff’s Complaint are relevant to Public Law 73-10, as no provision in that law (1) allows Plaintiff to ‘convert’ a payment demand into a money order to satisfy a loan, (2) provides a set-off from the U.S. Government as a means to discharge debts; or (3) voids or nullifies promissory notes.”

The court added that Stokes was advancing a “sovereign citizen” theory and dismissed the case with prejudice.

Legal Consequences: Stokes received nothing, still owed the debt, and faced potential sanctions for filing a frivolous lawsuit.

Williams v. Skelly (W.D. Ky. 2018)

Facts: Plaintiff sent a “contract/bond” document to the Department of Education claiming it discharged his student loans under HJR 192.

Court’s Ruling:

“Plaintiff appears to be asserting a form of ‘sovereign citizen’ claim… Courts have consistently rejected the ‘outlandish legal theories’ of sovereign citizens claims… Complaints based on sovereign citizen theories may be dismissed without extended argument.”

Outcome: Dismissed. Plaintiff still owed student loans plus accumulated interest.

What Happens If You Try This?

Legal Consequences:

- ❌ Your debt remains 100% valid and collectible

- ❌ Creditors can sue you for non-payment

- ❌ Courts may sanction you for filing frivolous claims

- ❌ You may be charged with fraud or conspiracy

- ❌ Your credit score will be destroyed

- ❌ You waste time and legal fees on a guaranteed loss

Real case examples like Stokes v. Santander show how courts penalize frivolous claims, underscoring why legitimate cases—such as those handled by a wrongful death lawyer—require solid legal grounding.

The “Sovereign Citizen” Connection

What Is the Sovereign Citizen Movement?

The “sovereign citizen” movement promotes the false belief that individuals can declare themselves exempt from government authority, taxes, and debt obligations through special paperwork or legal theories. HJR 192 is one of their most commonly cited “tools.”

Common Sovereign Citizen Claims About HJR 192:

- “The government created a secret ‘trust account’ in your name at birth”

- “Your birth certificate is a ‘bond’ the government trades”

- “Sending the right paperwork ‘accesses’ your account to pay debts”

- “Creditors can’t collect because money isn’t real after 1933”

The Truth: These theories have no basis in law. The U.S. Department of Justice, FBI, and federal courts have repeatedly labeled sovereign citizen legal tactics as fraudulent.

Why Do Courts Treat This Seriously?

Federal judges recognize HJR 192 debt discharge attempts as violating the principles of a formal legal promise, which requires genuine consideration and enforceable terms. Some courts have imposed fines and sanctions on filers—similar to the legal remedies available when an insurance settlement is mishandled, ensuring accountability in financial disputes..

Common Misconceptions Debunked

❌ Myth #1: “All Debts Are Prepaid Under HJR 192”

The Claim: Because the U.S. left the gold standard, the government now “pre-pays” all debts through a hidden system.

The Reality: HJR 192 changed HOW debts are paid (dollars instead of gold), not WHO pays them. You still owe your creditors. According to 31 U.S.C. § 5118:

“The United States Government may not pay out any gold coin… An obligation issued… before October 27, 1977, that requires payment in gold coin or in a particular coin or currency, may be discharged by payment in United States coin or currency that is legal tender at the time of payment.”

This statute confirms debts must be PAID, just in modern currency.

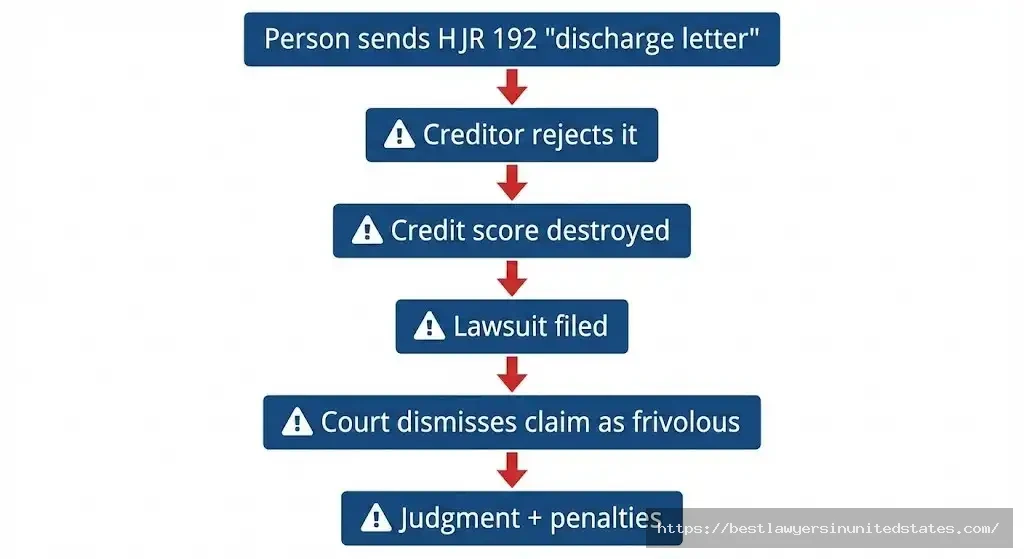

❌ Myth #2: “I Can Send a ‘Letter of Discharge’ to Cancel My Mortgage”

The Claim: By citing HJR 192 in a formal letter, you can legally erase mortgage or credit card debt.

The Reality: Creditors will ignore or reject such letters. If you stop making payments, they will:

- Report you to credit bureaus (destroying your credit score)

- Initiate foreclosure (for mortgages) or repossession (for auto loans)

- Sue you for the full balance plus interest

- Obtain a judgment and garnish your wages

Court Warning: In Sanford v. Robins Federal Credit Union, the court noted that attempting this could expose you to counterclaims for fraud.

❌ Myth #3: “HJR 192 Created a ‘Treasury Direct Account’ in My Name”

The Claim: Every American has a secret account at the U.S. Treasury worth millions, accessible through HJR 192.

The Reality: No such accounts exist. This myth conflates:

- Treasury Direct (a real platform for buying U.S. savings bonds)

- Sovereign citizen fantasy (the imaginary “birth certificate bond”)

The U.S. Treasury has explicitly stated that these theories are false and that attempting to access non-existent accounts can trigger federal fraud investigations.

❌ Myth #4: “Lawyers and Judges Hide This Secret Because They Profit From Debt”

The Claim: HJR 192 is a suppressed truth that the legal system conceals.

The Reality: HJR 192 is publicly available. Congress.gov archives the full text. Law schools teach it in Constitutional Law courses. The Supreme Court cited it in 1935. There is no conspiracy—there’s just a 1933 law that did something completely different from what online myths claim.

🚨 SCAM ALERT: HJR 192 “Debt Elimination” Programs

How the Scam Works

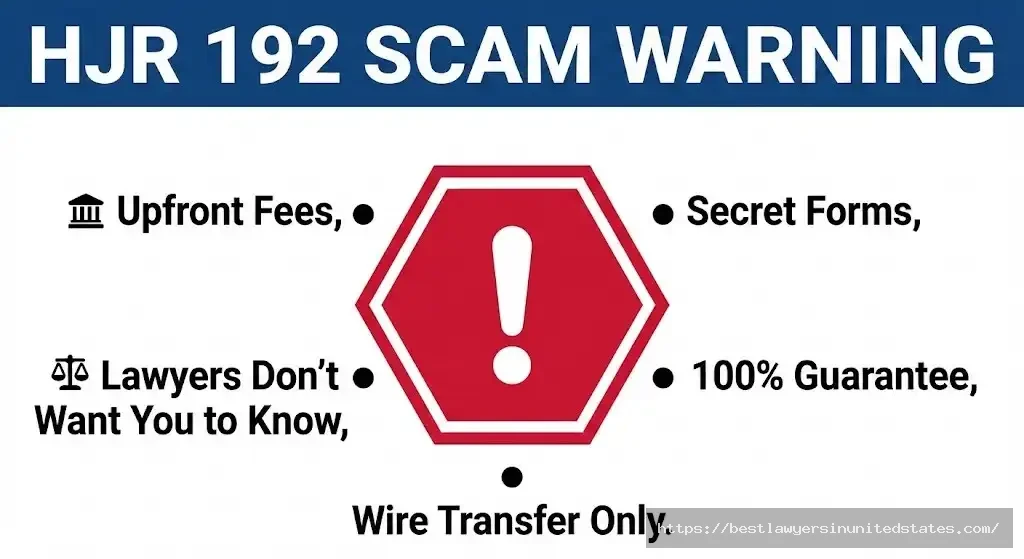

Fraudulent “debt relief” companies and online gurus sell “HJR 192 training packages” for $500-$5,000, promising:

- “Secret forms” to discharge debt

- “Bonded promissory notes” that supposedly pay your bills

- “Affidavits of tender” that claim to satisfy obligations

- “Treasury Direct Account” access instructions

What you actually get: Worthless templates that will be rejected by creditors and mocked by courts.

Red Flags to Watch For

🚩 Claims like:

- “Lawyers don’t want you to know this”

- “The government doesn’t want this information public”

- “Works 100% if you follow the steps exactly”

- “Thousands have eliminated millions in debt”

- “Based on a 1933 law banks hate”

🚩 Tactics used:

- High-pressure sales (“This offer expires tonight!”)

- Fake testimonials

- Misquoted court cases

- No refund policy

- Demands payment via wire transfer, Bitcoin, or gift cards

Report Scammers

If you’ve been targeted:

- Federal Trade Commission (FTC): ReportFraud.ftc.gov

- FBI Internet Crime Complaint Center: IC3.gov

- State Attorney General: NAAG.org

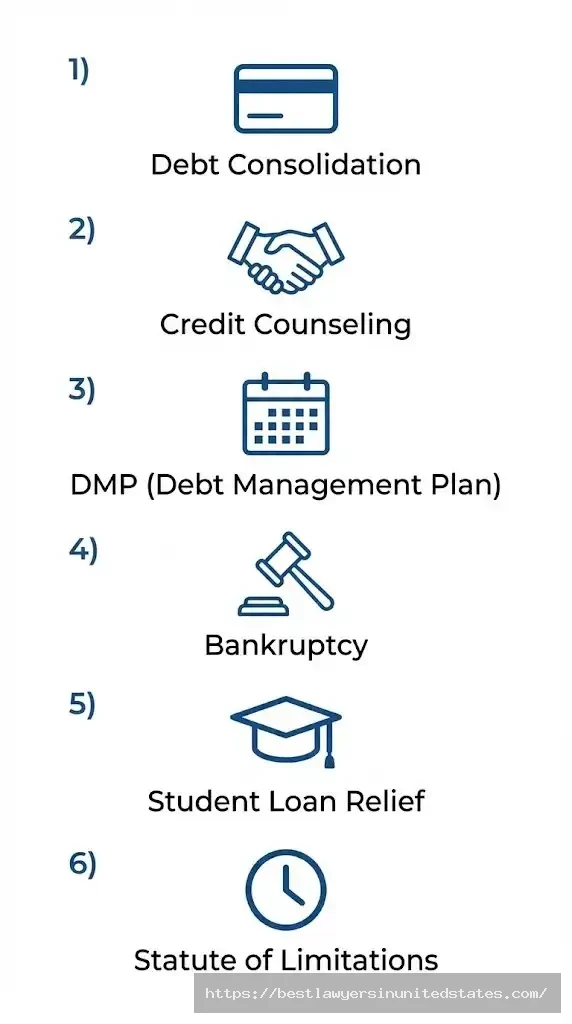

Real Debt Relief Options That Actually Work

If you’re struggling with debt, these legitimate strategies can help—including consultations with experienced bankruptcy attorneys who can evaluate your options.:

1. Debt Consolidation Loans

- Combine multiple debts into one lower-interest loan

- Available through credit unions, banks, and online lenders

- Explore options at NerdWallet

2. Credit Counseling (Non-Profit)

- Just as certified counselors negotiate with creditors, understanding your legal options for workplace disputes can help resolve complex financial situations tied to employment issues.

- Can reduce interest rates and waive fees

- Free or low-cost through NFCC.org

3. Debt Management Plans (DMP)

- Structured repayment program lasting 3-5 years

- Consolidates payments without new loans

- Stops collection calls and late fees

4. Bankruptcy Protection

- Chapter 7: Discharges most unsecured debts (credit cards, medical bills)

- Chapter 13: Repayment plan for 3-5 years, keeps your assets

- Consult a bankruptcy attorney for a free evaluation

5. Income-Driven Repayment (Student Loans)

- Federal student loans qualify for income-based plans

- Payments capped at 10-20% of discretionary income

- Learn more at StudentAid.gov

6. Statute of Limitations Defense

- Old debts may be uncollectible after 3-10 years (varies by state)

- Consult a consumer rights attorney before responding to old debt claims

What HJR 192 Tells Us About Money Today

The Fiat Currency System

HJR 192 marked America’s transition to fiat currency—money that has value because the government declares it legal tender, not because it’s backed by gold.

Why this matters:

- The Federal Reserve can manage inflation and interest rates flexibly

- Economic crises don’t trigger gold hoarding panics

- Credit systems (mortgages, credit cards, business loans) can function without gold reserves

Modern Monetary Policy

Today’s economy operates under principles established in 1933:

- 31 U.S.C. § 5103: “United States coins and currency… are legal tender for all debts, public charges, taxes, and dues.”

- The Federal Reserve manages the money supply to stabilize the economy

- Debts are enforceable contracts, payable in U.S. dollars

HJR 192’s Legacy: It proved governments can stabilize economies by controlling monetary policy—a power used during the 2008 financial crisis and 2020 pandemic response.

Frequently Asked Questions

Is HJR 192 still in effect in 2026?

Yes and no. The specific gold clause prohibition remains codified at 31 U.S.C. § 5118, but it’s largely irrelevant because gold clauses disappeared after 1933. The law’s practical effect ended decades ago, though the statute has not been repealed.

Can I legally discharge any debt using HJR 192?

No. Not credit cards, student loans, mortgages, auto loans, medical bills, or any other debt. Courts have rejected this theory in 100% of cases for 90 years.

Where can I read the original HJR 192 text?

- Official Source: Congress.gov Archives (Search “H.J.Res. 192, 73rd Congress”)

- U.S. Statutes at Large: 48 Stat. 112 (June 5, 1933)

- Modern Codification: 31 U.S.C. § 5118

Has anyone successfully used HJR 192 to eliminate debt?

No. If someone claims they did, they are lying. Every documented court case since 1935 has ruled against these attempts. Many resulted in sanctions, fraud charges, or contempt findings.

Why do people keep claiming HJR 192 discharges debt?

Three reasons:

- Economic desperation: People drowning in debt want to believe in a “magic bullet”

- Sovereign citizen propaganda: Coordinated misinformation campaigns online

- Scammers profit: Fraudulent “debt relief” gurus charge thousands for fake training

What should I do if a creditor threatens to sue me?

Do NOT ignore it. If sued:

- Respond within the deadline (usually 20-30 days)

- Consult a consumer rights attorney immediately (many offer free consultations)

- Just as you’d request debt validation when challenged by collectors, understanding what employees should look for in employment agreements helps protect your financial rights in contractual relationships.

- Consider negotiating a settlement (creditors often accept 40-60% of balance)

- Explore bankruptcy if overwhelmed (Chapter 7 or 13)

Is HJR 192 connected to “redemption theory” or “accept for value”?

Yes. “Redemption theory” and “A4V” (accept for value) are sovereign citizen tactics that misuse HJR 192 language. Both are universally rejected by courts and can expose you to fraud charges.

Does HJR 192 apply to modern cryptocurrency or digital dollars?

No. HJR 192 addressed gold-backed obligations. Cryptocurrencies didn’t exist in 1933, and digital dollars (if ever issued by the Fed) would function as legal tender under 31 U.S.C. § 5103, not HJR 192.

What’s the difference between HJR 192 and Public Law 73-10?

They’re the same. House Joint Resolution 192 was the congressional bill number. When signed into law on June 5, 1933, it became Public Law 73-10 (the 10th public law of the 73rd Congress).

Can I cite HJR 192 in court to challenge a debt?

Technically yes, but you will lose and may face sanctions. Judges are familiar with these theories and reject them immediately. You’ll waste legal fees and damage your credibility.

Timeline: 90 Years of Court Rejections

| Year | Case | Outcome |

|---|---|---|

| 1935 | Perry v. United States (Supreme Court) | HJR 192 upheld; debts must be paid in dollars, not gold |

| 1935 | Norman v. Baltimore & Ohio R.R. (Supreme Court) | Gold clauses in private contracts voided; payment in dollars required |

| 2009 | McLaughlin v. CitiMortgage (D. Conn.) | “Vapor money” theory rejected as frivolous |

| 2012 | Sanford v. Robins Federal Credit Union (M.D. Ga.) | HJR 192 debt discharge claim dismissed |

| 2014 | Wilkerson v. Gozdan (M.D. Ala.) | Credit slip/promissory note scheme rejected |

| 2018 | Stokes v. Santander Consumer USA (M.D. Ala.) | “Money order” discharge theory dismissed as sovereign citizen claim |

| 2018 | Williams v. Skelly (W.D. Ky.) | Student loan “contract/bond” dismissed; sanctions considered |

| 2019 | Lawrence v. Holt (N.D. Ala.) | HJR 192 cited; case dismissed as “utterly frivolous” |

| 2025 | [Ongoing] | Federal courts continue rejecting HJR 192 theories nationwide |

Pattern: Not a single case in 90 years has ruled in favor of using HJR 192 to discharge personal debt.

Final Verdict: What You Must Remember

✅ What HJR 192 Actually Did

- Ended the gold standard for domestic transactions

- Voided “gold clauses” in contracts written before 1933

- Established U.S. currency (dollars) as legal tender for ALL debts

- Gave the Federal Reserve flexibility to manage monetary policy

❌ What HJR 192 Did NOT Do

- Create “government accounts” to pay your bills

- Allow individuals to “discharge” debts without payment

- Void modern credit cards, mortgages, or loan contracts

- Establish a “secret” system lawyers and judges hide

⚖️ Legal Reality

- 100% of court cases since 1935 reject HJR 192 debt discharge theories

- Attempting this can result in fraud charges, sanctions, and legal penalties

- Your debt remains fully valid and collectible

🛡️ Protect Yourself

- Avoid scams offering HJR 192 “training” or “forms”

- Seek legitimate debt help through non-profit credit counseling or bankruptcy attorneys

- Report fraudsters to the FTC and state attorneys general

Need Real Legal Help With Debt?

If you’re facing overwhelming debt, these resources provide genuine assistance:

- National Foundation for Credit Counseling: NFCC.org | 800-388-2227

- Legal Aid Society (Free Legal Help): LawHelp.org

- Student Loan Forgiveness Programs: StudentAid.gov/IDR

- Bankruptcy Attorneys (Free Consultations): Search your state bar association

Remember: Legitimate debt relief never requires upfront fees, never guarantees 100% debt elimination, and never involves citing obscure 1933 laws. If it sounds too good to be true, it is.

Legal Disclaimer: This article provides educational information about HJR 192 and is not legal advice. If you are facing debt collection, lawsuits, or financial hardship, consult a licensed attorney in your state. BestLawyersInUnitedStates.com does not endorse or promote sovereign citizen theories, debt discharge schemes, or fraudulent legal tactics.

Sources & Further Reading:

- H.J.Res. 192, 73rd Congress (1933), codified at 48 Stat. 112

- 31 U.S.C. § 5118 – “Gold clauses and consent to sue”

- Perry v. United States, 294 U.S. 330 (1935)

- Sanford v. Robins Federal Credit Union, No. 5:12-CV-306, 2012 WL 5875712 (M.D. Ga. Nov. 20, 2012)

- Stokes v. Santander Consumer USA, No. 2:18cv50, 2019 WL 2552488 (M.D. Ala. June 18, 2019)

- U.S. Department of the Treasury, “Myths About Treasury Direct Accounts”

- Federal Reserve History, “The Gold Standard and the Great Depression”

- Cornell Law School, Legal Information Institute – Constitutional Law Resources

Comments