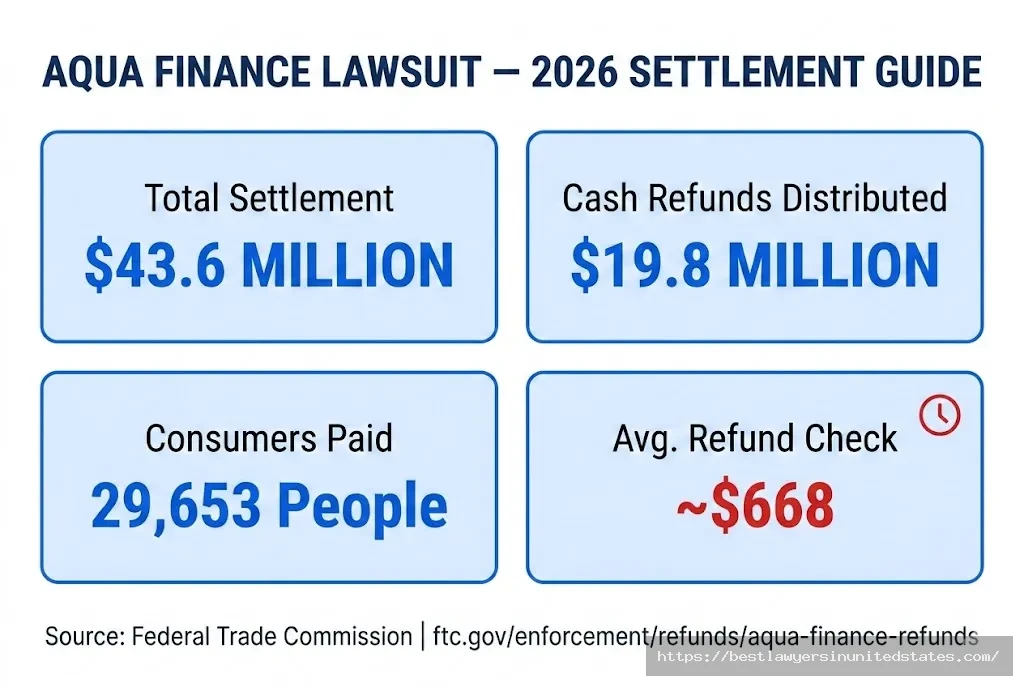

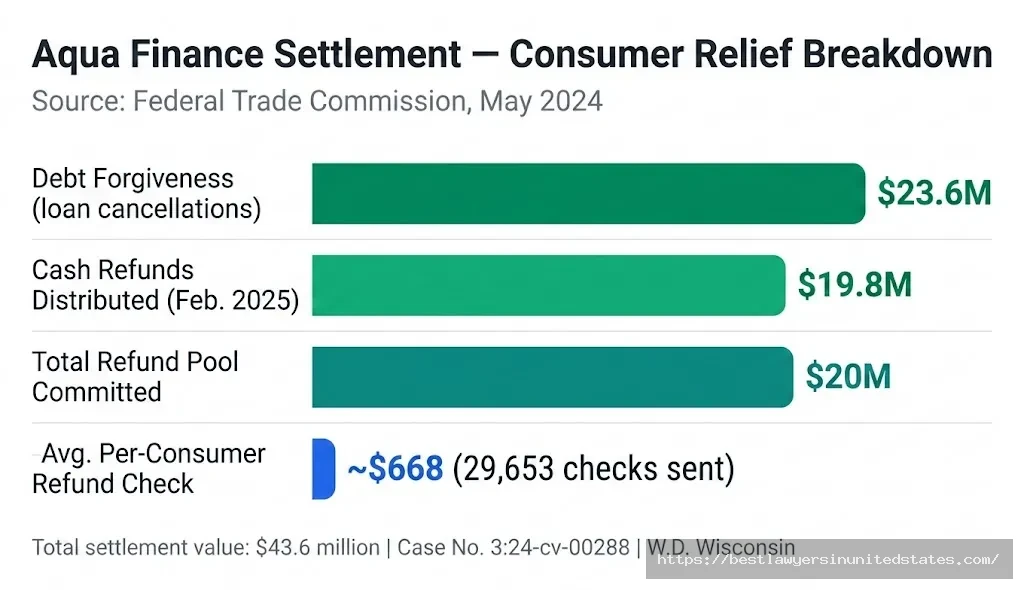

The Aqua Finance lawsuit is one of the most significant consumer protection cases against a home financing company in recent history. The Federal Trade Commission (FTC) sued Aqua Finance, Inc. (AFI) in May 2024, alleging that its network of door-to-door dealers systematically deceived homeowners about the true cost of water treatment financing — leaving tens of thousands of people stuck with unexpected debt, sky-high interest rates, and liens on their own homes. Aqua Finance agreed to a $43.6 million settlement, including $19.8 million in direct refund checks and $23.6 million in debt forgiveness. The FTC distributed refund checks to 29,653 affected consumers in February 2025.

Quick Answer: Aqua Finance settled with the FTC for $43.6 million over deceptive water treatment financing sales practices affecting consumers primarily from 2018–2021. The FTC sent refund checks averaging roughly $668 each to 29,653 consumers in February 2025. If you financed a water treatment system through Aqua Finance and believe you were deceived, you still have options — including disputing credit damage and pursuing individual legal claims.

If you didn’t receive a refund check but feel you were harmed, keep reading. There are still concrete steps you can take in 2026.

Aqua Finance Lawsuit Overview

| Fact | Details |

|---|---|

| Case Name | FTC v. Aqua Finance, Inc. |

| Case Number | 3:24-cv-00288 |

| Court | U.S. District Court, Western District of Wisconsin |

| Filed | May 1, 2024 |

| Defendant | Aqua Finance, Inc. (Wausau, Wisconsin) |

| Settlement Amount | $43.6 million total |

| Cash Refunds | $19.8 million (distributed February 2025) |

| Debt Forgiveness | $23.6 million |

| Consumers Paid | 29,653 refund checks |

| Refund Administrator | Epiq Systems |

| Refund Admin Phone | 1-888-884-8509 |

| FTC Refund Page | ftc.gov/enforcement/refunds/aqua-finance-refunds |

| FTC Complaint Line | ReportFraud.ftc.gov |

What Is the Aqua Finance Lawsuit About?

Background of the Case

Aqua Finance, Inc. is a Wisconsin-based company that provided financing for water filtration and softening systems sold through a nationwide network of door-to-door dealers. Since at least January 2018, AFI funded, serviced, and collected on more than 297,000 credit agreements totaling over $1 billion in systems sold across the country.

The problem wasn’t the water systems — it was how the financing was sold. AFI-approved dealers fanned out across the country, knocking on doors and pitching water treatment products with misleading promises about the cost. According to the FTC’s complaint, dealers routinely told customers that low introductory interest rates and payments were permanent. In reality, those rates jumped dramatically after 12 months, costing the average consumer thousands of dollars more over the life of the loan than what they were told.

Many of the people targeted were older homeowners and Latino consumers — populations that federal regulators say were deliberately sought out for these high-pressure sales tactics. The FTC says Aqua Finance knew all of this was happening for years and did essentially nothing to stop it. LOLA Tampons Lawsuit 2026

Timeline of Key Events

| Date | Event | Details |

|---|---|---|

| 2015 | Early warnings ignored | AFI approved a Houston-based dealer targeting Spanish-speaking consumers despite red flags |

| January 2018 | Deceptive practices escalate | AFI’s door-to-door dealer network expands nationally |

| 2018–2021 | Peak harm period | Thousands of deceptive loans originated; consumers begin filing complaints |

| 2020 | Internal email surfaces | AFI VP wrote to CEO identifying “systemic issues” about interest rate confusion |

| 2020–2023 | Thousands of complaints filed | Consumers complained directly to AFI and through the BBB, state AGs, and the FTC |

| May 1, 2024 | FTC files lawsuit | Case 3:24-cv-00288 filed in the Western District of Wisconsin |

| May 1, 2024 | Settlement announced simultaneously | Stipulated final order filed alongside complaint |

| May 2024 | Settlement terms finalized | $43.6 million in relief; permanent injunction imposed |

| 2024 | Debt forgiveness letters sent | Aqua Finance mailed letters to consumers whose debt was being cancelled |

| February 19, 2025 | FTC mails refund checks | 29,653 checks totaling over $19.8 million sent to eligible consumers |

| May 2025 | 90-day check cashing window closes | Deadline to cash FTC refund checks |

| Ongoing | Private lawsuits continue | Individual consumer claims still active; AFI under permanent injunction |

Who Filed the Lawsuit?

The Federal Trade Commission filed the complaint against Aqua Finance, Inc. on May 1, 2024, in the U.S. District Court for the Western District of Wisconsin (Case No. 3:24-cv-00288). The FTC staff attorneys on the matter included Edward Hynes, Luis Gallegos, Reid Tepfer, Erica Hilliard, and Tammy Chung from the FTC’s Southwest Region. The Commission vote to file was 3-0-2. The Tennessee Office of the Attorney General, the California Department of Financial Protection and Innovation, and Texas RioGrande Legal Aid also assisted in the matter.

What Are the Allegations?

The FTC’s complaint charged Aqua Finance with multiple violations of federal consumer protection law. Here’s what AFI and its dealers were accused of doing:

- Misrepresenting interest rates — Dealers told customers that promotional low APRs were permanent when they weren’t. After 12 months, rates jumped, costing the average consumer thousands of dollars more than they were promised.

- Hiding that interest accrued during deferral — Many consumers were told payments were deferred, but no one told them interest kept piling up the whole time.

- Concealing home liens — Aqua Finance took a security interest in financed equipment. This created a lien that made it hard or impossible for consumers to sell or refinance their homes — and dealers almost never disclosed this upfront.

- Falsely promising lifetime warranties and included service — Dealers claimed the equipment came with free service and lifetime coverage that didn’t exist.

- Ignoring thousands of complaints — AFI’s internal database showed hundreds of complaints about individual dealers. The company kept doing business with them anyway — including one dealer who had a prior fraud conviction.

- Violating the Fair Credit Reporting Act (FCRA) — When consumers disputed inaccurate credit reporting, AFI failed to investigate properly, failed to notify credit bureaus of disputes, and mishandled identity theft reports. This was the first time the FTC alleged this type of FCRA violation.

A 2020 internal email — written by an AFI vice president to the CEO — acknowledged the problem directly: AFI received complaints from customers who had a “lack of understanding of how interest works” and showed “dissatisfaction with the product.” Despite knowing this, the company took no meaningful action for years.

Who Qualifies for Relief from the Aqua Finance Settlement?

Quick Answer: The FTC automatically identified eligible consumers and sent them checks in February 2025. You didn’t need to file a claim — the FTC selected recipients based on Aqua Finance’s own records. If you received a letter or check, you were included. If you didn’t, there are still options for credit repair and individual legal action.

How the FTC Determined Eligibility

Unlike many class action settlements where you submit a claim form, this FTC enforcement action worked differently. The FTC and its settlement administrator (Epiq Systems) used Aqua Finance’s consumer database and loan records to identify harmed consumers directly. Checks were mailed automatically to people the FTC determined had been harmed by deceptive dealer practices.

Separately, Aqua Finance contacted consumers whose remaining loan balances were cancelled through the debt forgiveness portion of the settlement.

Eligibility Checklist (FTC Refund Recipients)

| Criterion | Details | What It Means |

|---|---|---|

| Financed through Aqua Finance | You signed a credit agreement with AFI | The financing, not just the product, had to be through AFI |

| Affected by deceptive dealer practices | Dealer misrepresented your loan terms | AFI’s records showed your account was affected |

| Loan originated primarily 2018–2021 | The core harm period identified by the FTC | Contracts outside this period may not have qualified |

| Active account or prior payment history | AFI had your account on file | Your information had to be in AFI’s consumer database |

| U.S. consumer | Domestic accounts only | International accounts excluded |

Who Does NOT Qualify?

Not everyone who financed through Aqua Finance received a refund check. You likely weren’t included if:

- ❌ Your loan was originated before 2018 and didn’t fall within the deceptive practices period

- ❌ Your account wasn’t identified by the FTC as having been subject to dealer misrepresentation

- ❌ You financed through a dealer not included in AFI’s identified network of bad actors

- ❌ You already received full refunds or debt relief through a prior state-level action

- ❌ Your loan balance had been fully paid and the FTC didn’t calculate harm to your account

Debt Forgiveness: A Separate Track

If you received a letter from Aqua Finance (not the FTC) telling you your remaining balance was cancelled, that’s the debt forgiveness portion of the settlement. For those accounts:

- Your outstanding loan balance is wiped out — you owe nothing

- Aqua Finance is required to ask credit bureaus to delete the account from your credit report

- Any UCC fixture filings or liens against your property tied to the account must be released

- No action was required from you — if you got the letter, it’s done

How Much Money Could You Get?

Quick Answer: The total settlement fund is $43.6 million. The FTC distributed $19.8 million in cash refunds to 29,653 consumers — averaging approximately $668 per check. Separate debt forgiveness cancelled $23.6 million in outstanding loan balances for other affected consumers.

Settlement Fund Breakdown

| Category | Amount | Description |

|---|---|---|

| Total Settlement Value | $43.6 million | Full value of consumer relief |

| Cash Refunds | $20 million | FTC-administered refund pool |

| Actual Cash Distributed | $19.8 million | Sent to 29,653 consumers in Feb. 2025 |

| Debt Forgiveness | $23.6 million | Outstanding loan balances cancelled |

| Permanent Injunction | No monetary value | Requires AFI to change business practices |

Estimated Refund Amounts

The FTC didn’t publish a tiered payout structure. Refund amounts were calculated based on the financial harm each consumer’s account reflected — meaning people who were overcharged more or for longer generally received larger checks. Money Metals Exchange Lawsuit

| Relief Type | Average/Range | Who Got This |

|---|---|---|

| Cash refund check | ~$668 average | 29,653 consumers identified by FTC |

| Debt cancellation | Varies by remaining balance | Consumers with balances written off |

| Credit report deletion | N/A (credit repair benefit) | Debt forgiveness recipients |

| Lien release | N/A (property benefit) | Homeowners with UCC fixture filings |

| Combined relief (some consumers) | Both refund + debt forgiveness | Consumers with both types of harm |

Factors That Affected How Much Someone Received

Your check amount depended on:

- How much you overpaid due to the interest rate bait-and-switch

- How long you were in the deceptive loan before discovering the true terms

- Whether you were a primary or secondary account holder

- The extent of credit damage AFI’s practices caused your account

- Whether your account showed clear evidence of dealer misrepresentation in AFI’s records

Current Status: What’s Happening in 2026

Settlement Is Final — But Aqua Finance Is Still Under Court Order

The FTC settlement is fully approved and implemented. Refund checks went out in February 2025. Debt forgiveness letters were sent. But that doesn’t mean the case is entirely closed from a consumer standpoint.

Aqua Finance is now operating under a permanent injunction — a federal court order that requires it to:

- Run robust monitoring programs for all dealers, including tracking complaints and terminating dealers who repeatedly deceive consumers

- Provide clear and conspicuous disclosures about liens on consumers’ property before any financing agreement is signed

- Stop misrepresenting the terms of its financing products in any form

- Comply with the Fair Credit Reporting Act in handling disputes and furnishing information to credit bureaus

If Aqua Finance violates any of these requirements, it faces additional federal court penalties.

Latest 2026 Developments

- February 2025 — FTC distributed $19.8 million in refund checks to 29,653 consumers. The 90-day cashing window on those checks has since closed.

- Ongoing 2025–2026 — Individual consumer lawsuits continue. Some people not included in the FTC’s refund distribution are pursuing separate legal claims against Aqua Finance under state consumer protection laws.

- $50 million accounting verdict — Separately, a jury found Aqua Finance’s former accounting firm liable for negligence, resulting in a $50 million verdict in a related case — adding to the financial and legal pressure on AFI.

- Dealer network scrutiny continues — Regulators are monitoring AFI’s dealer relationships under the permanent injunction.

Comparison with Similar FTC Actions

| Case | Settlement | Consumers Paid | Relief Type | Status |

|---|---|---|---|---|

| Aqua Finance (AFI) | $43.6 million | 29,653 | Cash + debt relief | Complete |

| VIVINT Smart Home | $20 million | ~88,000 | Cash refunds | Complete |

| Lularoe | $25 million | ~150,000+ | Cash refunds | Complete |

| GreenSky | $2.5 million | Varies | Consumer protection | Complete |

| First American Payment Systems | $4.9 million | Small businesses | Cash refunds | Complete |

The Aqua Finance case stands out for its combination of cash refunds and debt cancellation — a two-track approach that provided relief to different categories of harmed consumers.

What to Do If You Were Affected But Didn’t Get a Check

This is the most common question in 2026 from people who believe they were scammed by Aqua Finance but weren’t included in the FTC’s refund distribution. Here’s exactly what to do.

Step 1: Verify Whether You Received Debt Forgiveness

Check your mail from 2024–2025. Aqua Finance sent letters directly to consumers whose balances were cancelled under the $23.6 million debt forgiveness track. If you got one of those letters, your balance is gone and credit deletion should follow. Call Aqua Finance at 800-997-5356 to confirm the status of your account if you’re unsure.

Step 2: Contact the FTC Refund Administrator

If you believe you should have received a refund check but didn’t, call Epiq Systems at 1-888-884-8509 — the official FTC refund administrator for this case. Have your Aqua Finance account number and a description of the issue ready.

You can also visit the FTC’s official refund page at: ftc.gov/enforcement/refunds/aqua-finance-refunds

Step 3: File a Complaint with the FTC

Even if the main settlement distribution is complete, filing a complaint helps regulators track ongoing harm and can support future enforcement. Report your experience at ReportFraud.ftc.gov. Include:

- Your Aqua Finance account number

- The date you signed the financing agreement

- What you were told by the dealer vs. what your contract actually said

- Any financial harm you suffered (extra interest paid, credit damage, home sale difficulty)

Step 4: Dispute Credit Damage

If Aqua Finance’s practices damaged your credit report, you have rights under the Fair Credit Reporting Act regardless of the FTC settlement:

| Action | How to Do It | Where |

|---|---|---|

| Request your credit report | Free at AnnualCreditReport.com | All three bureaus |

| File a dispute for inaccurate items | Write to Equifax, Experian, TransUnion | Bureau websites or certified mail |

| Demand deletion of forgiven accounts | If your debt was cancelled, AFI must request deletion | Contact AFI at 800-997-5356 |

| File CFPB complaint | If credit bureaus ignore your dispute | ConsumerFinance.gov/complaint |

Step 5: Consult a Consumer Protection Attorney

If your losses were significant — you paid thousands in extra interest, couldn’t sell your home due to a lien, or suffered major credit damage — an individual lawsuit may be worth pursuing. Several legal frameworks still apply:

- State consumer protection laws (many states have stronger remedies than federal law)

- Truth in Lending Act (TILA) — requires clear disclosure of all credit terms

- Fair Credit Reporting Act (FCRA) — governs credit reporting and disputes

- Texas Deceptive Trade Practices Act and similar state-level statutes

Many consumer protection attorneys handle these cases on contingency, meaning you pay nothing unless you win.

Required Documentation to Support Your Claim

| Document | Why You Need It | Where to Find It |

|---|---|---|

| Original credit agreement | Shows what terms you were actually given | Your files, or request from AFI |

| Dealer’s verbal promises (written record) | Proves misrepresentation | Texts, emails, notes from the sales visit |

| Payment history | Documents overcharges | Bank statements, AFI account portal |

| Credit reports | Shows damage from AFI’s practices | AnnualCreditReport.com |

| Home sale/refinance documents | Proves lien-related harm | Title company, mortgage lender |

| FTC complaint confirmation | Shows you’ve already reported it | Email from ReportFraud.ftc.gov |

Do You Need a Lawyer?

Quick Answer: For the FTC settlement, no — the process was automatic and no attorney was needed. For individual claims, ongoing disputes, or significant financial harm not covered by the settlement, consulting a consumer protection attorney is worth considering. Many offer free initial consultations.

The FTC Handled the Settlement — No Attorney Required

The FTC lawsuit was not a traditional class action where you file a claim form. The government handled the entire process: identified affected consumers from AFI’s own records, calculated their harm, and mailed checks directly. No attorney was needed to participate.

When Individual Legal Help Makes Sense

Think about talking to an attorney if:

- You suffered major financial losses (thousands in excess interest, blocked home sale, foreclosure risk)

- Your credit was seriously damaged and AFI or the credit bureaus aren’t correcting it

- You believe you were targeted based on your age or ethnicity — additional civil rights protections may apply

- You’re in a state with strong consumer protection laws that could provide greater recovery than the FTC settlement offered

- You want to pursue damages beyond what the FTC distributed

Free Legal Resources

- FTC Consumer Advice line: consumer.ftc.gov or 1-877-FTC-HELP

- Consumer Financial Protection Bureau (CFPB): ConsumerFinance.gov/complaint

- State Attorney General: Your state AG’s consumer protection division handles deceptive lending complaints

- Legal Aid organizations: If you qualify based on income, free legal help may be available

- Free consultations: Many consumer protection attorneys offer a free first call — contact [email protected] for attorney referrals

Frequently Asked Questions

What is the Aqua Finance lawsuit?

Quick Answer: It’s an FTC enforcement action filed in May 2024 against Aqua Finance, Inc. for deceiving consumers about water treatment financing terms. The case settled for $43.6 million.

AFI’s dealers went door-to-door selling water filtration systems while misrepresenting interest rates, hiding that interest accrued during deferral periods, and failing to disclose that AFI was placing liens on consumers’ homes. The FTC sued, and AFI settled — agreeing to pay $20 million in refunds, cancel $23.6 million in debt, and change its business practices permanently. Ancient Nutrition Lawsuit

Who was eligible for a refund check?

Quick Answer: Consumers identified by the FTC as having been harmed by Aqua Finance’s deceptive dealer practices, primarily from 2018–2021, received automatic refund checks in February 2025.

You didn’t apply. The FTC used AFI’s own loan database to identify affected accounts and mailed checks directly. No claim form was required.

How much did refund checks pay?

Quick Answer: The FTC distributed $19.8 million to 29,653 consumers — an average of roughly $668 per check. Individual amounts varied based on the financial harm each account reflected.

Can I still get money from the Aqua Finance settlement in 2026?

Quick Answer: The 90-day window to cash refund checks (mailed in February 2025) has closed. However, you may still have options through individual legal action, credit repair, or state-level consumer protection claims.

If your debt was cancelled through the $23.6 million forgiveness track, that relief is complete regardless of timing. If you believe you were harmed but weren’t included in the FTC distribution, consult a consumer protection attorney or contact the FTC at 1-888-884-8509.

What if I received a debt forgiveness letter?

Quick Answer: Your remaining Aqua Finance loan balance is cancelled. You owe nothing. AFI is also required to request credit bureau deletion of your account and release any property liens.

Call Aqua Finance at 800-997-5356 to confirm your account balance shows $0 and to verify that the lien release process has been completed if applicable.

What if I didn’t receive a check or letter but I was scammed?

Quick Answer: You still have options. File a complaint with the FTC at ReportFraud.ftc.gov, contact the refund administrator at 1-888-884-8509, and consider consulting a consumer protection attorney.

Individual lawsuits under state consumer protection laws, the Truth in Lending Act, and the Fair Credit Reporting Act are still available. The FTC settlement didn’t cut off your right to sue separately.

Does Aqua Finance still operate?

Quick Answer: Yes. Aqua Finance remains in business but is now under a permanent federal court injunction requiring it to operate honestly and monitor its dealers.

AFI describes itself as still providing financing for home renovations and water treatment systems. Under the court order, it must make clear disclosures, closely monitor dealers, and stop all misrepresentations.

Did Aqua Finance admit wrongdoing?

Quick Answer: No. Like most FTC settlements, Aqua Finance settled without admitting wrongdoing. On its website, the company states it “strongly disagrees with the allegations” but chose to settle to focus on its business.

What was the $50 million verdict mentioned in some reports?

Quick Answer: Separately from the FTC case, a jury found Aqua Finance’s former accounting firm liable for negligence — resulting in a $50 million verdict in a related civil case.

This was a separate civil lawsuit between Aqua Finance and its auditing firm, not a consumer refund case. It doesn’t directly result in additional consumer payments.

Were only certain states affected?

Quick Answer: No. Aqua Finance operated a nationwide dealer network, and affected consumers span all 50 states. The FTC worked with regulators in Tennessee, California, and Texas specifically, but the harm was national.

My credit was damaged. Can I get that fixed?

Quick Answer: Yes. If your debt was cancelled, AFI must ask credit bureaus to delete the account. If AFI damaged your credit through improper reporting, you can dispute it under the Fair Credit Reporting Act.

Dispute inaccurate items directly with Equifax, Experian, and TransUnion. If your disputes are ignored, file a complaint with the Consumer Financial Protection Bureau at ConsumerFinance.gov/complaint. An attorney can also help force corrections.

Can I still file a lawsuit against Aqua Finance individually?

Quick Answer: Yes. The FTC settlement doesn’t prevent you from suing Aqua Finance separately. Individual lawsuits under state consumer protection laws, TILA, and FCRA remain available.

Statutes of limitations vary by state and claim type, so don’t wait. Consult a consumer protection attorney as soon as possible if you’re considering individual legal action.

What is Aqua Finance now required to do differently?

Under the permanent injunction, Aqua Finance must:

- Monitor all dealers rigorously and terminate those who mislead consumers

- Clearly and conspicuously disclose that its financing creates a security interest (lien) in the equipment installed in your home, before you sign

- Stop all misrepresentations about financing terms, interest rates, and payment amounts

- Handle credit bureau disputes properly, including notifying bureaus of disputed information

- Report identity theft claims correctly

Violations of the injunction can result in additional federal court penalties.

How do I contact the FTC refund administrator?

The official refund administrator for the Aqua Finance FTC case is Epiq Systems. You can reach them at:

- Phone: 1-888-884-8509

- FTC Refund Page: ftc.gov/enforcement/refunds/aqua-finance-refunds

What if I’m still being billed by Aqua Finance after debt forgiveness?

Quick Answer: Contact Aqua Finance immediately at 800-997-5356. If they continue billing you after confirming your debt was cancelled, file a complaint with the FTC and CFPB and consult an attorney.

Where can I file a complaint about Aqua Finance?

You have several options:

| Agency | How to File | Contact |

|---|---|---|

| FTC | Report fraud online | ReportFraud.ftc.gov |

| CFPB | File complaint online | ConsumerFinance.gov/complaint |

| State Attorney General | Contact your state’s consumer protection office | Find at naag.org |

| BBB | Submit complaint online | bbb.org |

| FTC Refund Admin | For settlement-specific questions | 1-888-884-8509 |

Key Takeaways for Aqua Finance Consumers in 2026

The Aqua Finance FTC lawsuit stands as a clear example of what happens when a company prioritizes profits over transparency. AFI and its dealers spent years deceiving vulnerable homeowners about financing terms — and the company was aware of it the entire time. The $43.6 million settlement provided real relief to nearly 30,000 people and wiped out $23.6 million in debt for others.

If you were affected, the key points to act on now are:

- Verify your credit reports for any Aqua Finance accounts that should have been deleted after debt forgiveness

- Confirm lien releases if you had a UCC fixture filing against your property

- Contact the FTC or Epiq Systems if you believe you were harmed but weren’t included

- Consult a consumer protection attorney if your losses were significant — individual claims under state law, TILA, or FCRA are still available

- Report any ongoing issues to the FTC and CFPB to help protect other consumers from similar schemes

For consumer protection attorneys experienced in cases like this, contact [email protected] for referrals.