Crown Asset Management (CAM) is one of the most active debt-buying companies in the country — and if they’ve filed a lawsuit against you, or are blowing up your phone demanding money, you need to know your rights before you do anything else. This guide covers everything: who Crown Asset Management is, what legal options you have, how class action lawsuits against CAM work, and what steps to take right now if you’ve been served.

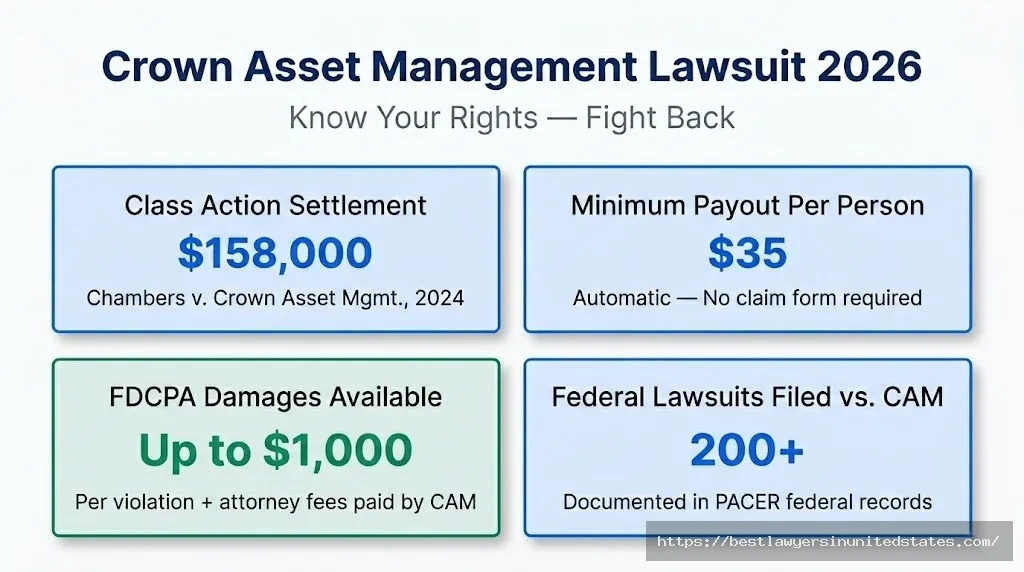

Quick Answer: Crown Asset Management, LLC is a Georgia-based “junk debt buyer” that purchases old, charged-off consumer debts for pennies on the dollar and then sues consumers to collect the full amount. A California class action (Chambers v. Crown Asset Management, Case No. 18CV338800) reached a $158,000 settlement in 2024 over improper debt collection letters. If you’re being sued by CAM right now in 2026, you have legal defenses — and CAM may actually owe YOU money if they violated the Fair Debt Collection Practices Act (FDCPA).

| Fast Facts | Details |

|---|---|

| Company Full Name | Crown Asset Management, LLC (CAM) |

| Headquarters | 3100 Breckinridge Blvd., Suite 725, Duluth, Georgia 30096 |

| Founded | 2004 |

| Business Type | Junk Debt Buyer / Third-Party Debt Collector |

| Key Class Action | Chambers v. Crown Asset Management, Santa Clara County |

| Class Action Settlement | $158,000 (Final approval hearing: Sept. 11, 2024) |

| FDCPA Lawsuits Filed Against CAM | 200+ documented in federal PACER records |

| Governing Federal Law | Fair Debt Collection Practices Act (15 U.S.C. § 1692) |

| FDCPA Damages Available | Up to $1,000 per violation + actual damages + attorney fees |

| Free Legal Help | Available — CAM pays attorney fees if you win |

Whether you got served with a Summons and Complaint, received threatening letters, or are just starting to research your options — you’re in the right place. Let’s break it down. Champion Windows Lawsuit History, Consumer Complaints & Your Legal Rights (2026)

What Is the Crown Asset Management Lawsuit?

Background: Who Is Crown Asset Management?

Crown Asset Management directly purchases portfolios of charged-off accounts from U.S. creditors. They buy a wide variety of charged-off accounts, including credit card, installment, lines of credit, auto loans, healthcare, telecom, utility, student loans, and retail.

In plain terms: if you defaulted on a credit card, medical bill, auto loan, or personal loan, your original lender may have sold your debt to CAM for a tiny fraction of what you owed — sometimes just a few cents per dollar. CAM then comes after you for the full balance, pocketing the difference as profit.

Since 2004, their business model has relied on buying people’s debt from other companies to generate profits. They are headquartered in Duluth, Georgia, and operate nationwide through a network of in-house and third-party collection attorneys.

This business model creates serious problems for consumers. By the time a debt reaches CAM’s hands, records may be incomplete, the statute of limitations may have expired, and the amount being demanded may be incorrect. These gaps are exactly what makes CAM lawsuits defensible — and sometimes winnable.

The Two Types of Crown Asset Management Lawsuits

When people search “Crown Asset Management lawsuit,” they’re usually dealing with one of two very different situations:

Type 1 — CAM Suing You: Crown Asset Management filed a collection lawsuit against you to collect an alleged debt. You received a Summons and Complaint in the mail or were served by a process server. This is the most common scenario and the one most people face.

Type 2 — Consumers Suing CAM: Crown Asset Management violated federal or state law in the way it collected — or tried to collect — a debt. In this situation, you become the plaintiff. The Chambers v. Crown Asset Management class action in California is the clearest example of this type.

Both scenarios are covered in this guide.

Timeline of Key Events Involving Crown Asset Management

| Date | Event | Details |

|---|---|---|

| 2004 | Crown Asset Management founded | Established in Duluth, Georgia as a debt purchasing firm |

| 2008 | Randolph v. Crown Asset Management | Federal court in N.D. Illinois certified class action over FDCPA and Illinois state law violations |

| 2014–2015 | Smith v. Crown Asset Management | FDCPA lawsuit over continued contact with consumer represented by counsel |

| 2017 | Persolve & CAM FDCPA class action (Wisconsin) | Proposed class action over improper collection notices |

| 2018 | Chambers v. Crown Asset Management filed | California Superior Court, Santa Clara County; Case No. 18CV338800 |

| Dec. 27, 2022 | Class certification granted | Court certified Chambers case as a class action |

| 2023–2024 | Settlement negotiations | Parties agreed to $158,000 class settlement |

| Sept. 11, 2024 | Final approval hearing | Judge Theodore C. Zayner presided, Dept. 19 |

| 2025–2026 | CAM active collection lawsuits | CAM filing hundreds of new suits monthly across the U.S. |

Who Runs Crown Asset Management?

CAM is managed by Brian Williams and operates primarily as a receivables purchasing and management company. According to the BBB, Crown Asset Management, LLC was founded in 2004. CAM is listed as a business consultant and financial services company. Buzzfile estimates Crown Asset Management’s annual revenue at $4.3 million and the size of its headquarters staff at 12 employees.

Despite its relatively small staff, CAM handles massive debt portfolios by outsourcing collection work to a network of law firms and collection agencies across the country. In lawsuits, they’re often represented by firms like Gurstel Law Firm, McCarthy Burgess & Wolff, and various regional collection law firms.

What Are the Allegations Against Crown Asset Management?

CAM has received consumer complaints alleging violations of the Fair Debt Collection Practices Act (FDCPA), including threatening to take actions that cannot legally be taken and attempting to collect debts not owed.

In the landmark Randolph v. Crown Asset Management case, the plaintiff alleged that Crown Asset violated Illinois state laws and the FDCPA by “filing collection actions on purported debts to which it did not have lawful title,” “fraudulently pretending to be a holder in due course,” and acting as a collection agency without a required license from the State of Illinois.

Common allegations across Crown Asset Management lawsuits and complaints include:

- ❌ Attempting to collect debts past the statute of limitations (“zombie debt”)

- ❌ Filing lawsuits without proper documentation proving they own the debt

- ❌ Sending collection letters that fail to include legally required notices in proper format

- ❌ Contacting consumers who are represented by attorneys

- ❌ Claiming incorrect debt amounts including unauthorized interest or fees

- ❌ Using third-party collectors who engage in harassing or deceptive conduct

- ❌ Operating without required state collection agency licenses

A search of PACER (Public Access to Court Electronic Records) will display over 200 lawsuits filed against CAM in U.S. courts, and these typically involve violations of consumer rights and/or the Fair Debt Collection Practices Act.

The Chambers v. Crown Asset Management Class Action Settlement

What Was This Lawsuit About?

Pamela S. Chambers filed a class action lawsuit against Crown Asset Management, LLC in the Superior Court of California, County of Santa Clara, alleging violations of the California Fair Debt Buying Practices Act, California Civil Code §§ 1788.50-1788.64. Plaintiff alleged that Defendant’s collection letters failed to include the notice required by California Civil Code § 1788.52(d)(1) in 12-point or larger type.

This might sound like a technical, small violation — a font-size requirement — but it’s a serious consumer protection issue. The mandatory notice exists specifically to inform people of their rights when being contacted by a debt buyer. Removing it or shrinking it below 12-point type can prevent consumers from knowing they have the right to dispute the debt, request verification, and receive complete account documentation.

Who Was Eligible?

California residents to whom McCarthy, Burgess & Wolff Inc. sent an initial written communication on behalf of Crown Asset Management attempting to collect a charged-off consumer debt originally owed to Synchrony Bank and whose mailings were not returned as undeliverable by the post office between Dec. 4, 2017, and Dec. 27, 2022.

| Eligibility Criterion | Details |

|---|---|

| State | California (must have had a California address) |

| Communication Type | Initial written collection letters only |

| Sender | McCarthy, Burgess & Wolff, Inc. (on behalf of CAM) |

| Original Creditor | Synchrony Bank |

| Date Range | December 4, 2017 – December 27, 2022 |

| Status of Letter | Must NOT have been returned as undeliverable |

Settlement Amount and Payouts

The total class settlement fund was $158,000. Defendant agreed to pay class members no less than $35 each. Any money not claimed by class members would be paid to Katharine & George Alexander Community Law Center in San Jose, California as a cy pres fund.

No claim form was required to benefit from the Crown Asset Management settlement. Class members who did not exclude themselves automatically received a settlement payment.

Important Note for 2026 Readers: The Chambers v. Crown Asset Management settlement final approval hearing was held September 11, 2024. This settlement is now closed. If you were a California class member, payments should have been distributed. If you believe you qualified but did not receive payment, contact the settlement administrator at 866-473-1092 or write to: Chambers v. Crown Asset Mgmt., c/o Settlement Administrator, PO Box 23369, Jacksonville, FL 32241-3369.

| Settlement Category | Amount |

|---|---|

| Total Settlement Fund | $158,000 |

| Minimum Per-Person Payout | $35 |

| Unclaimed Funds | Cy pres to Alexander Community Law Center |

| Claim Form Required? | No — automatic distribution |

| Final Approval Hearing | September 11, 2024 |

| Case Number | 18CV338800 |

| Court | Santa Clara County Superior Court, Dept. 19 |

Who Qualifies: Are You Being Sued by Crown Asset Management?

If you’re facing a CAM collection lawsuit in 2026, the eligibility question works differently than a traditional class action. You don’t “apply” for anything — you’re a defendant, and you need to respond. Here’s what you need to know.

Quick Answer: If Crown Asset Management has filed a lawsuit against you, you are not automatically in a losing position. CAM must prove it actually owns your debt, can document the full amount claimed, and filed the lawsuit within the applicable statute of limitations. Many CAM lawsuits fail on one or more of these requirements.

What Crown Asset Management Must Prove Against You

In a debt collection lawsuit, Crown Asset Management always has the burden to prove that the consumer is responsible for the debt. To meet this burden, Crown Asset Management must prove that: (1) it has the right to sue you; (2) the debt is yours; and (3) you owe the amount for which you were sued.

This is harder than it sounds. Debt portfolios are bought and sold multiple times. Records get lost. Chain of title becomes murky. Amounts get inflated. And statutes of limitations run out. CAM files lawsuits betting that you won’t respond — and when you do respond with a solid defense, the case often falls apart.

Eligibility Table: Do You Have Defenses?

| Defense Type | What It Means | Documentation Needed |

|---|---|---|

| Statute of Limitations | Debt may be too old to sue on (3–6 years depending on state) | Dates of last payment or account charge-off |

| Lack of Standing | CAM can’t prove it actually owns your debt | Demand complete chain of title documentation |

| Incorrect Amount | The amount claimed includes unauthorized fees or interest | Original account agreement and billing statements |

| Already Paid | You paid this debt or it was discharged in bankruptcy | Payment records, bankruptcy discharge papers |

| Identity Issues | Wrong person — debt isn’t yours | Photo ID, address history, credit reports |

| FDCPA Violations | CAM or its attorneys broke federal collection law | All collection letters received, call logs, voicemails |

| Improper Service | You were never properly served with the lawsuit | Records of when/how you received notice |

Who Cannot Be Sued Successfully?

CAM’s lawsuits are weakest against people in these situations:

- ❌ The debt is beyond your state’s statute of limitations (varies from 3–6 years by state)

- ❌ You filed for bankruptcy and the debt was discharged

- ❌ CAM cannot produce the original credit agreement with your signature

- ❌ The debt is not actually yours (identity theft, wrong person)

- ❌ CAM or its attorneys violated the FDCPA in the collection process

- ❌ CAM operated without a required collection agency license in your state

State-by-State Statute of Limitations for Credit Card Debt

| State | Statute of Limitations | Notes |

|---|---|---|

| New York | 3 years (post-2021 reform) | CPLR § 214-i; partial payments no longer restart clock |

| California | 4 years | Written contracts; includes credit cards |

| Texas | 4 years | Texas Civil Practice & Remedies Code § 16.004 |

| Florida | 5 years | Fla. Stat. § 95.11 |

| Illinois | 5 years | Applies to credit card debt |

| Georgia | 6 years | CAM’s home state |

Your Rights When Crown Asset Management Sues or Contacts You

The Fair Debt Collection Practices Act — Your Federal Shield

The FDCPA is the key federal law that limits what debt collectors like CAM and their attorney networks can do. The FDCPA is a federal law that regulates the collection of consumer debts. It precludes third party debt collectors from using false, misleading, deceptive and harassing debt collection tactics.

Under the FDCPA, Crown Asset Management and its collection attorneys cannot:

- Call you before 8:00 a.m. or after 9:00 p.m. in your time zone

- Contact you at work if you tell them your employer prohibits it

- Threaten legal action they have no intention of taking

- Discuss your debt with anyone except you, your spouse, or your attorney

- Claim to be government agents or law enforcement

- Continue contacting you after you retain an attorney and inform them

- Collect amounts not authorized by the original agreement or state law

- Use false, deceptive, or misleading statements to collect a debt

Under 15 USC § 1692g, you have the right to dispute the debt within 30 days, and the collector must cease collection until they provide verification. Send your dispute in writing, by certified mail, within 30 days of first contact.

What You Can Win If CAM Violated the FDCPA

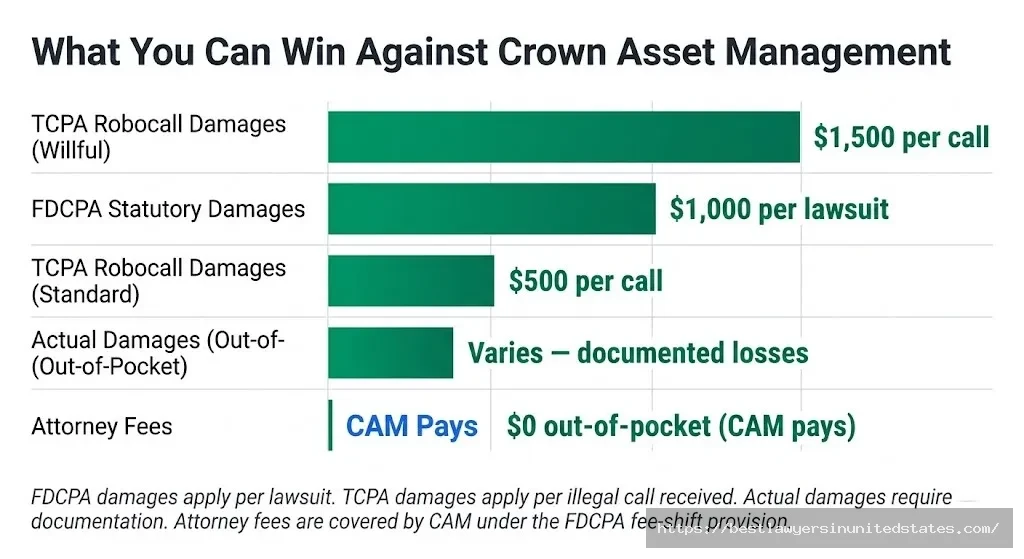

If a debt buyer like Crown Asset Management violates the FDCPA, you can sue it for statutory damages up to $1,000 plus actual damages (like pain and suffering) and your attorney’s fees.

The FDCPA also has a fee-shift provision, which means the debt collector will pay your attorney’s fees and costs. If you have a TCPA case against the agency, it can be handled on a contingency fee and you won’t pay a dime unless you win. Fabuloso Lawsuit: Complete 2026 Guide

| Type of FDCPA Damages | Amount |

|---|---|

| Statutory Damages (per lawsuit) | Up to $1,000 |

| Actual Damages | Varies — out-of-pocket losses caused by the violation |

| Attorney Fees and Court Costs | Paid by CAM if you win |

| TCPA Robocall Damages | $500–$1,500 per illegal call |

| Class Action FDCPA Statutory Damages | Up to $500,000 or 1% of net worth |

How to Respond if Crown Asset Management Sues You: Step by Step

⚠️ CRITICAL WARNING: If you were served with a lawsuit by Crown Asset Management, you have a limited window to respond — typically 20 to 30 days depending on your state and how you were served. If you miss this deadline, Crown Asset Management will get a default judgment against you automatically. Read this section immediately.

Step 1: Do Not Ignore the Lawsuit

Often, these Crown Asset Management lawsuits are filed in the hope that the debtor will simply not respond to the suit. Do not make this mistake. When you do not appear or defend yourself, a court often sees no reason not to enter a judgment against you. If a judgment is issued against you, it could follow you for as many as twenty years and will most certainly negatively affect your credit report for seven years or longer.

This can make it very difficult to buy a home, get a car loan, open credit accounts, or obtain financing of any kind. After a judgment, CAM can also pursue wage garnishment and bank account seizure.

Step 2: Know Your Response Deadline

| How You Were Served | Typical Response Window |

|---|---|

| Personal service within your state | 20–30 days (check your specific state rules) |

| Service by mail (some states allow) | Often longer — verify with your state court |

| Service on a family member at your home | Varies by state — confirm with an attorney |

| New York specific (personal service) | 20 days |

| California specific | 30 days |

Set a calendar reminder for 10 days before your deadline so you have time to respond properly.

Step 3: Gather All Documents

Collect everything related to this debt:

- The Summons and Complaint you received

- Any collection letters from CAM or its attorneys

- Any voicemails or call logs from CAM

- Your original account agreement (if you have it)

- Billing statements showing when you last made a payment

- Any bankruptcy discharge papers, if applicable

- Your Social Security number and credit report to verify the debt is actually yours

Step 4: File Your Written Answer

When Crown Asset Management sues you, you will receive two documents in the mail called the Summons and Complaint. The Summons notifies you of the debt lawsuit and your deadline to respond, while the Complaint lists all the specific claims being made against you.

Your written Answer should respond to each numbered allegation in the Complaint. For allegations you don’t know to be true, you can respond “Defendant lacks sufficient information to admit or deny this allegation.” You should also list your affirmative defenses, such as statute of limitations, lack of standing, and any FDCPA violations.

Step 5: Request Documentation from Crown Asset Management

When defending against Crown Asset Management, demand strict proof of ownership and account balance. File responsive pleadings raising affirmative defenses such as statute of limitations, lack of standing, and improper service.

Send discovery requests asking CAM to produce:

- The complete chain of title showing every sale of this debt from original creditor to CAM

- The original credit agreement bearing your signature

- A full account history showing how the claimed amount was calculated

- Proof that CAM is licensed to collect debts in your state

- All documentation used to calculate interest and fees

Step 6: Consider Negotiating a Settlement

Many clients pay little or nothing to debt purchasers. If you choose to settle, clients who show strength to debt purchasers usually settle their cases for about one-third of the amount demanded in the lawsuit.

Once CAM realizes you’re fighting back with legal representation, they frequently offer to settle for a fraction of the original demand — or drop the case entirely. Your attorney may be able to negotiate a favorable settlement rather than leaving the decision to a judge at trial. However, ensure there is a valid written settlement agreement to confirm that the debt is fully resolved. The last thing you want is to settle and then have Crown Asset Management pursue you later for additional unpaid debt.

Step 7: Evaluate Whether CAM Owes YOU Money

Before simply trying to defend or settle, have an attorney review CAM’s conduct for FDCPA violations. If Crown Asset did not provide a letter indicating that they are representing the creditor and informing you of your right to dispute the debt or request verification within 30 days, then they have violated the Fair Debt Collection Practices Act. Some attorneys actively pursue claims against violators of the FDCPA. If successful, the opposing party is responsible for covering your attorney fees. Additionally, you may be entitled to receive up to $1,000 for each violation.

Filing Deadlines: Don’t Miss These Dates

| Action | Timeline | What Happens if Missed |

|---|---|---|

| File written Answer | 20–30 days after service (varies by state) | Default judgment entered against you |

| Dispute the debt in writing | Within 30 days of first collection contact | Lose right to automatic collection cessation |

| File FDCPA counterclaim | Within 1 year of violation | Lose right to FDCPA damages |

| File motion to vacate default judgment | Varies by state (act immediately) | Judgment becomes permanent |

Common Mistakes People Make When Sued by Crown Asset Management

Don’t make these errors:

- Ignoring the lawsuit — The #1 mistake. CAM banks on you not responding.

- Admitting the debt over the phone — Never confirm the amount or make a payment without written confirmation of all terms.

- Missing your answer deadline — Set multiple calendar reminders.

- Assuming the debt is valid — CAM’s records are often incomplete or inaccurate.

- Negotiating without getting it in writing — Always get any settlement in a signed written agreement before paying anything.

- Not checking the statute of limitations — Many CAM lawsuits involve “zombie debts” that are time-barred.

- Forgetting to look for FDCPA violations — These can flip the situation entirely and make CAM owe you money.

Current Status and Latest Updates (2026)

What Crown Asset Management Is Doing Right Now

CAM remains extremely active in 2025 and 2026. BBB complaint records show new lawsuits being filed nearly every week, with recent filings in states including Georgia, Alabama, Minnesota, and Florida. After attempts to amicably resolve this matter were unsuccessful, a lawsuit was filed on or about January 6, 2026 and the consumer was served on January 20, 2026. This is one example of CAM’s ongoing collection activity.

CAM’s current collection strategy involves:

- Purchasing large portfolios of charged-off credit card debt, particularly from lenders like Synchrony Bank, Comenity Bank, Cross River Bank, and Upgrade

- Referring accounts to collection law firms (including Gurstel Law Firm and others) after initial collection attempts fail

- Filing lawsuits in state civil and district courts when consumers don’t respond to initial notices

- Obtaining default judgments against consumers who fail to answer

New York’s Consumer Credit Fairness Act — A Game-Changer

If you’re in New York, the 2021 Consumer Credit Fairness Act dramatically changed the landscape in your favor. The statute of limitations for consumer credit transactions is now three years, reduced from six. Importantly, the law prevents expired debts from being revived by partial payments or acknowledgments after the limitations period has lapsed. Further, when a debt buyer like CAM seeks a default judgment, courts apply stricter evidentiary rules.

This means a significant portion of New York CAM lawsuits are vulnerable to statute of limitations defenses.

The Chambers Settlement: What Happened

The Chambers v. Crown Asset Management class action reached final approval through the California Superior Court in 2024. The settlement required CAM to pay at least $35 to each qualifying California class member. No claim form was necessary — payments were distributed automatically. Unclaimed funds went to the Katharine & George Alexander Community Law Center in San Jose, California as a cy pres charitable donation.

Crown Asset Management Lawsuits vs. Similar Debt Buyer Cases

Understanding how CAM’s lawsuits compare to other debt buyers can help you understand the playbook these companies use — and how to fight back.

| Debt Buyer / Case | Nature of Action | Notable Outcome |

|---|---|---|

| Crown Asset Management (Chambers, 2024) | CA Fair Debt Buying Practices Act violations | $158,000 settlement; $35+ per class member |

| Midland Funding (Multiple class actions) | FDCPA violations, improper affidavits | Multi-million dollar settlements nationally |

| Portfolio Recovery Associates | FDCPA violations, robo-signed affidavits | FTC $19 million settlement (2015) |

| Asset Acceptance (FTC action) | Collecting time-barred debt without disclosure | $2.5 million FTC settlement |

| Encore Capital / Midland Credit | Deceptive collection practices | $42 million CFPB settlement (2015) |

| Persolve LLC & Crown Asset (Wisconsin, 2017) | FDCPA violations in collection notices | Class action filed |

What Makes Crown Asset Management Different?

A few key differences stand out:

- Smaller scale, aggressive volume: CAM has relatively few employees but outsources heavily to law firms, creating a high-volume lawsuit machine that relies on consumer non-response.

- Multi-layered collection: CAM frequently uses multiple law firms in sequence, which can create its own FDCPA compliance issues as notices get missed or repeated.

- Broad debt categories: CAM buys everything — credit cards, medical debt, auto loans, telecom debt, student loans, and retail — making its lawsuits appear across virtually every debt category.

Do You Need a Lawyer to Deal with Crown Asset Management?

Quick Answer: You don’t legally need a lawyer, but having one dramatically improves your odds — and if CAM violated the FDCPA, a lawyer may cost you nothing because CAM pays the fees. Byte Aligners Lawsuit

When You Can Probably Handle It Yourself

- The debt is clearly past the statute of limitations in your state

- You have strong documentation proving you don’t owe the debt

- The case is in small claims court and the amount is low

- You want to send a written debt validation request (you can do this yourself)

When You Should Absolutely Get an Attorney

- CAM has already gotten a default judgment against you

- The claimed amount is over $5,000

- You have reason to believe CAM violated the FDCPA

- You’re in New York, California, or another state with complex consumer protection laws

- Your wages are being garnished or bank account has been frozen

- The debt has been collected from the wrong person

Free and Low-Cost Legal Help Options

Many people sued by debt collectors do not hire an attorney. If you do nothing then they win. If you hire an attorney, the plaintiff may dismiss the lawsuit for financial reasons. Sometimes it is simply too expensive to collect a debt. If it appears to the creditor that they will not get an easy default judgment, they may decide not to pursue the lawsuit.

Here’s where to find free or low-cost help:

- Consumer Law Center, Inc. — Represented plaintiffs in Chambers v. Crown Asset Management; handles California cases

- Legal Aid organizations — Free legal help for income-qualifying consumers in most states

- FDCPA attorneys — Most work on contingency or fee-shift arrangements (you pay nothing unless you win)

- State Bar lawyer referral services — Typically offer free 30-minute initial consultations

- Contact for referrals: [email protected]

Frequently Asked Questions About Crown Asset Management Lawsuits

What is Crown Asset Management?

Quick Answer: Crown Asset Management (CAM) is a Georgia-based debt buyer that purchases defaulted consumer debts and attempts to collect the full amount.

Crown Asset Management LLC (CAM) is a debt collector. As a certified receivables company, Crown Asset Management is a business that buys debt. Since 2004, their business model has relied on buying people’s debt from other companies to generate profits. They buy portfolios of charged-off debt from banks, hospitals, credit card companies, auto lenders, and retailers — then pursue collection through letters, phone calls, and lawsuits.

Why is Crown Asset Management suing me?

Quick Answer: CAM purchased a debt they claim you owe and is suing to collect it, gambling you won’t respond.

CAM buys debt portfolios and then files lawsuits against people who don’t pay after letters and calls. Their business model depends on many consumers simply not responding, resulting in automatic default judgments. When you do respond, cases often get dismissed or settled for far less.

Do I actually owe Crown Asset Management money?

Quick Answer: Not necessarily — even if you had a legitimate original debt, CAM may not be able to prove they have the right to collect it.

CAM must prove it owns your specific debt, that the amount is accurate, and that the debt is not time-barred. These are significant legal hurdles. Many consumers successfully challenge CAM’s claims when proper legal defenses are raised.

How much can I get from the Chambers v. Crown Asset Management settlement?

Quick Answer: At least $35 per class member, from a $158,000 total settlement fund — but this settlement is now closed.

The settlement had a final approval hearing in September 2024. If you were a California class member who received a McCarthy Burgess & Wolff collection letter on behalf of CAM (for a Synchrony Bank debt) between December 4, 2017 and December 27, 2022, you should have received a check automatically. If you haven’t received payment, contact the settlement administrator at 866-473-1092.

What happens if I ignore a lawsuit from Crown Asset Management?

Quick Answer: A default judgment will be entered against you — giving CAM the power to garnish wages, freeze bank accounts, and place liens on property.

If a judgment is issued against you, it could follow you for as many as twenty years and will most certainly negatively affect your credit report for seven years or longer. This can make it very difficult to do things like purchase a home or a car, open credit accounts, and obtain loans. Never ignore a lawsuit.

Can Crown Asset Management garnish my wages?

Quick Answer: Yes, but only after they obtain a court judgment against you.

If you respond to the lawsuit and contest it, CAM cannot garnish your wages. Wage garnishment only becomes possible after a judgment — and judgments only happen when you either lose at trial or fail to respond and a default judgment is entered.

What is the deadline to respond to a Crown Asset Management lawsuit?

Quick Answer: Typically 20–30 days from the date you were served, depending on your state and how service was made.

This deadline is not flexible. Missing it allows CAM to request a default judgment without any hearing. If you’ve already missed the deadline, contact an attorney immediately — it may be possible to file a motion to vacate the default if you act quickly.

Can Crown Asset Management violate my rights?

Quick Answer: Yes — and if they do, you can sue them for up to $1,000 plus actual damages plus attorney fees.

CAM has received consumer complaints alleging violations of the Fair Debt Collection Practices Act (FDCPA), including threatening to take actions that cannot legally be taken and attempting to collect debts not owed. If any of these violations occurred in your case, you may have a counterclaim worth pursuing.

What is the FDCPA and how does it protect me from Crown Asset Management?

Quick Answer: The Fair Debt Collection Practices Act is a federal law that limits how debt collectors like CAM can contact you and what they can say.

Key protections include the right to dispute the debt in writing within 30 days, the right to request debt validation, and the prohibition on harassing or deceptive collection tactics. Violations can result in damages paid to you by CAM.

Can I settle with Crown Asset Management for less than they’re claiming?

Quick Answer: Yes — most cases settle for significantly less than the original demand when the consumer gets legal representation.

Clients who show strength to debt purchasers usually settle their cases for about one-third of the amount demanded in the lawsuit. Settlement amounts vary based on the strength of your defenses and how well-documented CAM’s claim is.

What documents do I need to defend against a Crown Asset Management lawsuit?

Quick Answer: Gather the Summons and Complaint, all collection letters, any payment records, your original account agreement (if available), and your credit report.

| Document | Why You Need It | Where to Get It |

|---|---|---|

| Summons and Complaint | Shows what CAM is claiming | You received this when served |

| Collection letters from CAM | May show FDCPA violations | Keep everything they sent you |

| Original account statements | Verify the amount claimed | Your old financial records |

| Credit report | Verify the account history and charge-off date | AnnualCreditReport.com (free) |

| Bankruptcy discharge papers | Proves debt was discharged (if applicable) | PACER or your bankruptcy attorney |

| Payment records | Show last payment date for SOL analysis | Bank records, cancelled checks |

What if the debt Crown Asset Management is suing me for is really old?

Quick Answer: The debt may be past the statute of limitations, which is a complete defense to the lawsuit — and in some states, even threatening to sue on time-barred debt violates the FDCPA.

Check your state’s statute of limitations (see the table above). If CAM filed the lawsuit after the limitations period expired, file an affirmative defense in your Answer asserting the statute of limitations. In New York, the CCFA now makes this defense even stronger.

Is Crown Asset Management required to prove they own my debt?

Quick Answer: Yes — and this is one of the most common weak points in their lawsuits.

CAM must produce a full chain of title showing how the debt was transferred from the original creditor to CAM. In practice, documentation gets lost during multiple portfolio sales. When a consumer demands proof, CAM frequently cannot provide it and may dismiss the case.

Will a Crown Asset Management lawsuit affect my credit?

Quick Answer: The judgment from a CAM lawsuit can appear as a public record on your credit report — but the original charged-off debt may already be there.

A CAM judgment can stay on your credit report for up to seven years from the judgment date (not the original charge-off date). This is separate from and in addition to the original charge-off entry. Settling or defeating the lawsuit before a judgment is entered is far better for your credit.

Can I sue Crown Asset Management?

Quick Answer: Yes — if they violated the FDCPA, TCPA, or applicable state consumer protection laws, you can file suit in federal court.

You will have a fee-shift provision, which means the debt collector will pay your attorney’s fees and costs. If you have a TCPA case against the agency, it can be handled based on a contingency fee and you won’t pay a dime unless you win. Contact a consumer protection attorney for a free evaluation.

How do I stop Crown Asset Management from calling me?

Quick Answer: Send a written cease-and-desist letter by certified mail — the FDCPA requires them to stop contacting you after receiving it (except to notify you of specific legal actions).

Once you hire an attorney and notify CAM, they must stop contacting you directly and communicate only through your attorney. Continuing to contact you after that notification is an FDCPA violation. Document everything.

Where can I find the official Crown Asset Management contact information?

Quick Answer: Crown Asset Management, LLC is located at 3100 Breckinridge Boulevard, Suite 725, Duluth, Georgia 30096.

For the Chambers settlement specifically, the settlement administrator was located at: Chambers v. Crown Asset Mgmt., c/o Settlement Administrator, PO Box 23369, Jacksonville, FL 32241-3369. Phone: 866-473-1092.

What to Do Right Now: Your Action Plan

The most important thing you can do is act quickly. Whether CAM is calling you, writing to you, or has already filed a lawsuit:

- Stop and read everything they sent you. Note all dates and deadlines.

- Do not call CAM or their attorneys and admit to or discuss the debt. Your words can be used against you.

- Send a written debt validation request within 30 days of first contact if a lawsuit hasn’t been filed yet.

- If you’ve been served with a lawsuit, contact an attorney today — or at minimum, file your written Answer before the deadline.

- Pull your credit report at AnnualCreditReport.com to see how CAM has reported the debt and verify account details.

- Look for FDCPA violations in everything CAM has done — the phone calls, the letters, the timing, the amounts claimed.

- Never pay anything without a signed, written agreement confirming the debt is fully resolved.

Understanding your rights is the most powerful weapon you have against Crown Asset Management. Many people who fight back win — or settle for a fraction of what CAM demands. The ones who lose are almost always the ones who did nothing.

This article is for informational purposes only and does not constitute legal advice. Laws vary by state and individual circumstances differ. Consult a licensed attorney in your state before taking any legal action.

For attorney referrals: [email protected] Settlement administrator (Chambers case): 866-473-1092