Midland Credit Management (MCM) has faced multiple class action lawsuits and federal enforcement actions over its debt collection practices — and if MCM is contacting you or has sued you right now, you may have rights worth thousands of dollars. adriana chechik lawsuit

The company and its parent, Encore Capital Group, have paid tens of millions in settlements to the federal government and consumers since 2015. Understanding what those cases were about, what your rights are today, and exactly how to respond whether MCM is chasing you or harassing you is the purpose of this guide. Jefferson Capital Systems Lawsuit

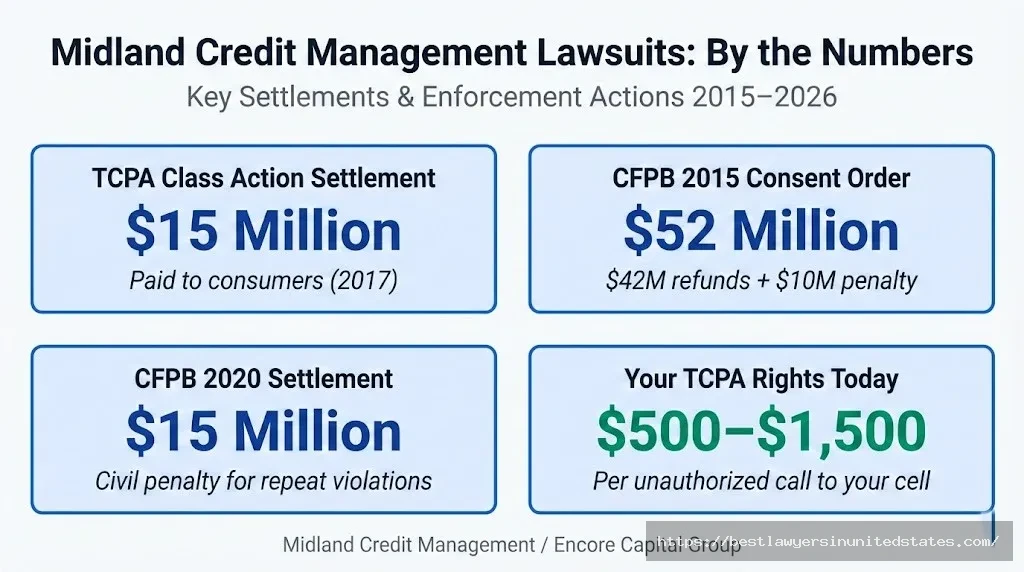

Quick Answer: Midland Credit Management has been the target of major class action and government lawsuits including a $15 million TCPA class action settlement (2017), a $42 million + $10 million CFPB consent order (2015), and a second $15 million CFPB penalty (2020) for violating that order. If MCM is calling you without consent or suing you for a debt, you may have legal rights under the FDCPA and TCPA — including the right to up to $1,500 per illegal call and free attorney representation.

Midland Credit Management Lawsuit Overview

| Key Fact | Details |

|---|---|

| Company Name | Midland Credit Management, Inc. (MCM) |

| Parent Company | Encore Capital Group, Inc. (NASDAQ: ECPG) |

| Headquarters | San Diego, California |

| What They Do | Buy and collect delinquent consumer debt |

| TCPA Class Action Settlement | $15 million (2017, closed) |

| CFPB 2015 Consent Order | $42M consumer refunds + $10M civil penalty |

| CFPB 2020 Settlement | $15M civil penalty + $79,308 in consumer redress |

| 42-State AG Settlement | 2018, addressed robo-signed affidavits |

| CFPB Complaints (2024) | 1,300+ filed against MCM |

| Governing Laws | FDCPA, TCPA, CFPA, FCRA |

What Is the Midland Credit Management Class Action Lawsuit?

There isn’t just one lawsuit — there’s a long history of them. MCM is one of the most sued debt collectors in America, and understanding the different cases helps you figure out where you stand.

Background: Who Is Midland Credit Management?

MCM is a debt buyer, not the company you originally owed money to. They purchase defaulted accounts — credit cards, personal loans, medical bills, auto loans — from original creditors for pennies on the dollar. According to available data, MCM pays roughly 3 cents per dollar for these portfolios. Then they attempt to collect the full balance from consumers like you.

As of early 2025, MCM and its affiliate Midland Funding were averaging roughly 500 lawsuits per week in Pennsylvania alone. That gives you a sense of the scale. Their parent company, Encore Capital Group, collected $2.16 billion from consumers in 2024 — including $561 million through court judgments. This is a massive, aggressive operation. OGX Shampoo Lawsuit

Timeline of Major Legal Actions Against MCM

| Date | Event | Details |

|---|---|---|

| 2011 | Robo-signed affidavit lawsuit | ~1.5 million consumers targeted with false affidavits |

| September 2015 | CFPB Consent Order | $42M consumer refunds + $10M civil penalty |

| November 2016 | TCPA Class Action Settlement | $15M settlement (Robinson v. Midland) approved |

| May 2017 | TCPA Settlement checks mailed | Payments sent to class members |

| 2018 | 42-State Attorney General Settlement | Addressed robo-signing practices across 38-42 states |

| September 2020 | CFPB files new lawsuit | Alleged violations of 2015 consent order |

| October 16, 2020 | CFPB Second Settlement | $15M civil penalty + $79,308 consumer redress |

| 2022 | Massachusetts Settlement | $12 million in consumer relief |

| 2024 | CFPB complaints spike | 1,300+ complaints filed in a single year |

Who Has Filed These Lawsuits?

Several different parties have taken legal action against MCM and its parent Encore Capital:

The CFPB (Consumer Financial Protection Bureau) — the federal agency — filed two major enforcement actions (2015 and 2020) after finding systematic violations of consumer protection law. The 2015 action was filed in the U.S. District Court for the Southern District of California.

Private plaintiffs in class actions — including Christopher Robinson, Eduardo Tovar, and Dave Scardina in the TCPA case (Case No. 11-MD-2286 MMA (MDD), Southern District of California) — filed on behalf of millions of consumers who received unauthorized robocalls.

State attorneys general — a coalition of 38–42 state AGs negotiated a settlement over robo-signed court affidavits, and Massachusetts secured a separate $12 million deal in 2022.

What Were the Allegations?

The lawsuits against MCM have centered on a consistent set of illegal practices:

- Collecting debts consumers did not owe — and filing court cases without proper documentation to prove the debt was valid

- Suing on time-barred debts — pursuing consumers in court for debts past the statute of limitations without required disclosures

- Robo-signed affidavits — filing court documents that falsely claimed firsthand knowledge of the debt

- Unauthorized robocalls — using automatic telephone dialing systems (autodialers) to call cell phones without the consumer’s prior express consent, in violation of the TCPA

- Deceptive collection letters — using misleading language, “Final Notice” labels when no prior notice existed, and false threats of legal action

- Violating a consent order — continuing prohibited practices after the 2015 CFPB settlement, which led to the 2020 lawsuit

The $15 Million TCPA Class Action Settlement (Closed)

This is the largest consumer-facing class action settlement MCM has faced.

What the TCPA Settlement Covered

MCM agreed to pay $15 million to resolve claims that it used an autodialer to call consumers’ cell phones without their consent while trying to collect debts. The settlement covered calls made between November 2011 and a defined cut-off date to a class of millions of Americans. Hello Toothpaste Lawsuit

How the Settlement Funds Were Distributed

| Fund Category | Amount | Who It Went To |

|---|---|---|

| Debt Forgiveness Fund | $13 million | Class members who still owed MCM money |

| Cash Payout Fund | $2 million | Class members who owed nothing to MCM |

| Total Settlement | $15 million | All qualifying class members |

Class members with outstanding MCM debt received a portion of the $13 million debt forgiveness pool — meaning their balance was reduced. Class members who had no outstanding MCM debt received a cash payment from the $2 million pool, divided among all who filed valid claims.

Important: This settlement is closed. Checks were mailed in May 2017. If you’re looking for compensation related to calls MCM made to you, you need to pursue an individual FDCPA or TCPA claim today — not a class action claim from this settlement.

The CFPB Enforcement Actions

The federal government has gone after MCM twice, and both times MCM (through Encore Capital) was forced to pay significant penalties.

2015 CFPB Consent Order: $42M + $10M Penalty

The CFPB found that Encore and its subsidiaries — including MCM and Midland Funding — had engaged in a pattern of illegal behavior between 2011 and 2015:

- Collected debts consumers did not owe

- Filed court affidavits falsely claiming personal knowledge of the debt

- Sued consumers on time-barred debts without required disclosures

- Stated incorrect debt balances and interest rates

- Halted collection on more than $125 million in debts as part of the order

The 2015 order required up to $42 million in consumer refunds, a $10 million civil penalty, and a set of ongoing conduct requirements MCM had to follow.

2020 CFPB Settlement: Another $15M Penalty

MCM violated the 2015 consent order. The CFPB filed a new lawsuit in September 2020 and settled it within weeks, on October 16, 2020. The violations included suing consumers without possessing required documentation, using law firms without providing required disclosures, and failing to give consumers required loan documentation when asked.

The settlement: $15 million civil money penalty + $79,308.81 in direct consumer redress + five more years of the 2015 conduct provisions.

Who Can Sue MCM Today? Your Rights Under the FDCPA and TCPA

Even though the major class action settlements are closed, your individual rights are alive and potentially very valuable. Here’s what the law gives you.

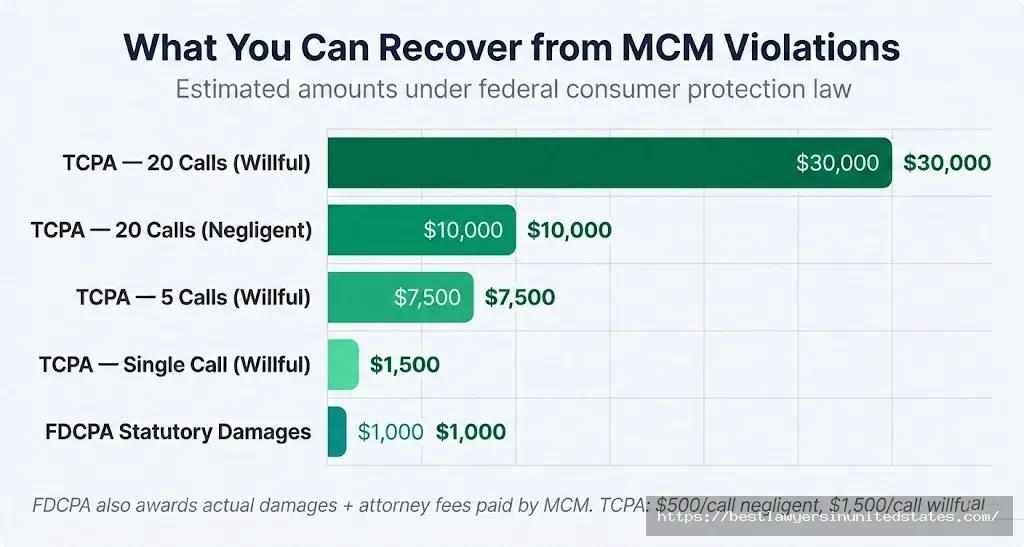

Quick Answer: If MCM called your cell phone without your consent, you may be entitled to $500–$1,500 per call under the TCPA. If they violated the FDCPA (deceptive letters, false threats, collecting debts you don’t owe), you may recover up to $1,000 in statutory damages plus actual damages and attorney’s fees — often at no cost to you.

FDCPA Rights: What MCM Cannot Do

The Fair Debt Collection Practices Act prohibits MCM from:

| Prohibited Conduct | What It Means |

|---|---|

| Collecting debts you don’t owe | They must be able to prove the debt is valid and belongs to you |

| Calling at unreasonable hours | No calls before 8 AM or after 9 PM in your time zone |

| Threatening legal action they can’t take | They cannot threaten to sue if they don’t intend to |

| Misrepresenting the debt amount | They must state the correct balance |

| Contacting third parties | They generally can’t call your employer, neighbors, or family |

| Ignoring cease communication requests | Once you send a written stop-contact letter, they must stop |

| Collecting time-barred debts without disclosure | They must tell you if the debt is past the statute of limitations |

| Harassment or abuse | No threatening language, repeated calls intended to harass |

TCPA Rights: The Power of Unauthorized Calls

If MCM called your cell phone using an autodialer or prerecorded message without your consent:

- Negligent violation: $500 per call

- Willful/knowing violation: Up to $1,500 per call

- No proof of actual harm required

Think about how many times MCM may have called you. Even 10 calls could be worth $5,000–$15,000.

FCRA Rights: Credit Report Violations

If MCM is reporting inaccurate information to credit bureaus — or reporting a debt they cannot verify — you may have claims under the Fair Credit Reporting Act as well.

How to File a Claim Against MCM (FDCPA or TCPA)

If MCM has violated your rights, you don’t need to sit back. Here’s how the process works.

Step 1: Document Everything

Start keeping records immediately. This is the most critical step.

- Write down every phone call: date, time, number called from, what was said

- Save every letter MCM sends — keep the envelopes (postmarks matter)

- Note if they contacted your employer, neighbors, or family members

- Screenshot any voicemails

- Keep all credit reports that show MCM’s reporting

Step 2: Request Debt Verification

Under the FDCPA, you have the right to demand written verification of any debt MCM claims you owe. Send this request in writing (certified mail, return receipt requested) within 30 days of their first contact. Once you send it, MCM must stop collection activity until they verify the debt.

Request them to provide:

- The original creditor’s name

- The original account number

- A copy of the original agreement

- A complete account history

- Documentation proving MCM legally owns or has standing to collect the debt

Many times, MCM cannot produce this documentation — especially for older debts.

Step 3: Send a Cease Communication Letter (Optional)

You have the right to send MCM a written letter telling them to stop all contact. Once they receive it, they may only contact you to confirm they’re stopping or to notify you of a specific legal action. Send this by certified mail.

Step 4: Consult a Consumer Rights Attorney (Free)

Here’s the best part of FDCPA cases: attorneys take them on contingency, with zero upfront cost to you. If you win, MCM pays your attorney’s fees. This means it costs you nothing to explore whether you have a valid claim.

An attorney can also identify violations you might not notice — like improper letter formatting, missing disclosures, or problematic collection timing.

Step 5: File a Complaint with the CFPB

Go to consumerfinance.gov/complaint and file a detailed complaint. The CFPB tracks these, investigates patterns, and their records were a key part of building the 2015 and 2020 enforcement cases. Your complaint helps the next person too.

You can also file with the FTC at reportfraud.ftc.gov and your state attorney general’s office.

Required Documentation Checklist

| Document | Why You Need It | Where to Find It |

|---|---|---|

| Collection letters from MCM | Proves contact and content of demands | Your own records; request copies if needed |

| Call logs / phone records | Shows frequency and timing of calls | Your cell carrier (request statement) |

| Voicemail recordings | Proves autodialer or prerecorded calls | Your phone |

| Credit report | Shows MCM’s reporting | AnnualCreditReport.com (free) |

| Original creditor account records | Helps verify or dispute the debt | Request from original creditor |

| Certified mail receipts | Proves you sent verification/stop requests | USPS |

If MCM Is Suing You: How to Defend Yourself

This is increasingly common. MCM files hundreds of lawsuits every week across the country. Here’s what you need to know if you’ve been served.

Quick Answer: Do NOT ignore a lawsuit from MCM. Ignoring it gives them an automatic default judgment, which can lead to wage garnishment and bank levies. You typically have 14–30 days to respond, depending on your state.

Response Deadlines by Court Type

| Court Type | Response Deadline | Notes |

|---|---|---|

| Texas Justice of the Peace Court | 14 days | From date of service |

| Texas County or District Court | 20 days | From date of service |

| Most other states | 20–30 days | Varies by state |

| Federal Court | 21 days | From date of service |

Your Defense Strategies

1. Challenge the documentation. Demand that MCM prove: (a) you owe the debt, (b) the amount is correct, (c) they legally own the debt. They purchased it from someone else — they need a valid “bill of sale” and the complete account history. Many times they don’t have it.

2. Check the statute of limitations. Every state has a time limit on how long a creditor can sue you for a debt. In Texas, it’s 4 years for written contracts. If the debt is older than that, MCM may be time-barred from suing you. This is one of the most powerful defenses available.

3. Verify the debt is actually yours. Identity theft and database errors are real. MCM buys large portfolios of accounts — mistakes happen. You have no obligation to pay a debt that isn’t yours.

4. File a counterclaim for FDCPA violations. If MCM violated the law in their collection efforts, you can file a counterclaim right in the same lawsuit. Instead of just defending, you can go on offense.

5. Negotiate a settlement. If the debt is valid and MCM has proper documentation, settling for a reduced amount is often better than going to trial. MCM paid roughly 3 cents per dollar — they have room to negotiate.

State-Specific: Being Sued in Texas

Texas has specific rules that affect MCM cases:

| Texas Rule | Details |

|---|---|

| Response deadline (JP Court) | 14 days from service |

| Response deadline (County/District) | 20 days from service |

| Statute of Limitations | 4 years for written contracts (credit cards) |

| Wage Garnishment | Texas is one of the most debtor-friendly states — wages largely exempt |

| Homestead Protection | Texas has strong homestead exemptions protecting your home |

| Counterclaim for FDCPA | You can file in the same Texas court action |

Texas is actually one of the best states to be sued in by MCM — because your wages are largely protected from garnishment, and your homestead is strongly protected. Even if MCM wins a judgment, collecting on it in Texas is difficult. That said, bank accounts can still be levied, so don’t ignore it.

Comparison: MCM Settlements vs. Similar Debt Collector Cases

| Case / Settlement | Amount | Key Issue | Year |

|---|---|---|---|

| MCM TCPA Class Action | $15M | Unauthorized robocalls | 2017 |

| MCM / Encore CFPB Consent Order | $42M refunds + $10M penalty | Illegal collection tactics | 2015 |

| MCM / Encore CFPB Second Settlement | $15M penalty | Violating 2015 consent order | 2020 |

| MCM Massachusetts Settlement | $12M | Consumer relief | 2022 |

| Portfolio Recovery Associates (CFPB) | $19M | Similar debt buyer violations | 2015 |

| Asset Acceptance (FTC) | $2.5M | FDCPA violations | 2012 |

| Cavalry Portfolio Services (CFPB) | $3.25M | Suing on time-barred debts | 2017 |

The pattern is clear: debt buyers who purchase old accounts and aggressively collect without proper documentation have faced significant federal enforcement. MCM has faced more regulatory action than almost any other debt buyer.

Current Status & Latest Updates (February 2026)

What’s Still Active

The 2020 CFPB stipulated judgment extended the 2015 consent order’s conduct provisions through at least 2025. This means MCM is still under federal oversight requirements — including obligations around documentation, time-barred debt disclosures, and consumer notices.

According to data from Encore Capital’s own SEC filings through 2024, MCM continues to face “ancillary state attorney general investigations related to similar debt collection practices” and has “entered into settlement agreements with the Attorneys General of various U.S. states.”

CFPB complaint volume against MCM trended sharply upward: approximately 495 complaints in 2022, 705 in 2023, and over 1,300 in 2024. The dominant complaint theme: consumers saying the debt isn’t theirs or has already been paid — the exact violations the CFPB flagged in 2015.

What This Means for You in 2026

The legal landscape for MCM has not changed in your favor. If MCM is contacting you right now with a debt you don’t recognize, a debt past the statute of limitations, or using tactics that feel harassing, the law still gives you strong protections — and attorneys who handle these cases are still very active.

The most important thing: don’t assume you have to pay just because MCM says so.

Frequently Asked Questions

What is the Midland Credit Management class action lawsuit?

There have been several. The most notable is a $15 million TCPA settlement (Robinson v. Midland, 2017) for unauthorized robocalls to cell phones. There have also been major CFPB enforcement actions in 2015 ($42M + $10M penalty) and 2020 ($15M penalty) for illegal debt collection practices including collecting on unverified debts and robo-signed affidavits.

Can I still file a claim from the TCPA class action settlement?

No. The $15 million TCPA class action settlement closed in 2017 and payments were sent in May 2017. That settlement is no longer accepting claims. However, if MCM has called your cell phone without consent recently, you may have a new individual TCPA claim.

How much money can I get if MCM violated the TCPA?

Each unauthorized call to your cell phone using an autodialer or prerecorded message is worth $500–$1,500 under the TCPA. If MCM called you 20 times without consent, your potential recovery ranges from $10,000 to $30,000. Attorney fees are paid by MCM if you win.

How much can I get for FDCPA violations?

Up to $1,000 in statutory damages for the case (not per violation), plus any actual damages you suffered, plus attorney’s fees paid by MCM. The attorney’s fee provision is what makes these cases economically viable to bring, even for small claims.

Is Midland Credit Management a legitimate company?

Yes. MCM is a real, legal company. It is the in-house collection arm of Encore Capital Group (publicly traded on NASDAQ). Being legitimate doesn’t mean they always follow the law — federal regulators have found otherwise — but they are not a scam operation.

What if MCM is suing me right now?

Respond to the lawsuit immediately. Ignoring it leads to a default judgment, which gives MCM the ability to pursue bank levies and (in most states) wage garnishment. In Texas, you have 14 days if sued in JP Court or 20 days in County/District Court. Consult a consumer defense attorney right away — many offer free consultations and work on contingency.

Can MCM garnish my wages?

Only if they win a court judgment against you first. They cannot garnish wages just by threatening to. In Texas specifically, wages are largely exempt from garnishment, making Texas one of the more consumer-friendly states. However, bank accounts can still be levied in Texas after a judgment.

What if the debt is too old — past the statute of limitations?

If the debt is past your state’s statute of limitations (4 years in Texas for credit card debt), MCM generally cannot win a lawsuit against you. However, they are still technically allowed to ask you to pay — they just can’t get a court judgment. If they sued you and the debt is time-barred, that’s a complete defense. Some states also require MCM to disclose when a debt is time-barred; failing to do so is itself an FDCPA violation.

Can I stop MCM from contacting me?

Yes. Send MCM a written cease communication letter by certified mail. Under the FDCPA, once they receive it, they must stop all collection contact (with limited exceptions for notifying you of specific actions). Keep your certified mail receipt as proof.

What if the debt MCM is collecting isn’t mine?

This happens more than you’d think — identity theft and data errors in bulk debt purchases are real. You have the right to demand written verification of the debt. If MCM continues collecting without verification, or can’t prove the debt is yours, that’s an FDCPA violation. Dispute it in writing immediately and consult an attorney.

What should I do if I receive a collection letter from MCM?

Don’t ignore it. Read it carefully. Note the date, the amount, and who the original creditor was. Within 30 days, send a written debt verification request by certified mail. Don’t make any payment or even verbally acknowledge the debt before verifying it — partial payment in some states can restart the statute of limitations clock.

Do I need a lawyer to fight MCM?

Not always. For the initial response to a lawsuit, you can file an answer yourself. But having a consumer defense attorney substantially improves your chances. For FDCPA/TCPA claims, attorneys typically take these cases for free (MCM pays fees if you win), so there’s no financial reason not to consult one.

Will fighting MCM hurt my credit score?

MCM has likely already reported the debt to the credit bureaus, which is affecting your credit. A successful dispute or FDCPA claim can result in MCM being required to delete the tradeline from your credit report — which would help, not hurt, your score.

Has MCM been sued by the government?

Yes. Twice by the CFPB (2015 and 2020), resulting in $10 million and $15 million civil penalties respectively, plus $42 million in consumer refunds from the 2015 action. They’ve also settled with 38–42 state attorneys general and reached state-specific settlements including $12 million in Massachusetts.

Where do I file a complaint about MCM?

File with the CFPB at consumerfinance.gov/complaint, with the FTC at reportfraud.ftc.gov, and with your state attorney general’s consumer protection division. You can also file a complaint with the Better Business Bureau. The CFPB complaint database is public, which helps researchers and regulators spot patterns.

What types of debt does MCM collect?

MCM primarily buys and collects credit card debt from major banks including Chase, Citibank, and Capital One, as well as retail credit cards (Synchrony Bank, Comenity Bank), personal loans, telecommunications and utility debts, and some medical debt.

What is Midland Funding vs. Midland Credit Management?

They’re related but different. Midland Funding LLC is the legal entity that actually purchases and owns the debt. Midland Credit Management, Inc. is the servicing/collection arm that contacts consumers and handles the collection process. For practical purposes, both are subsidiaries of Encore Capital Group and you’ll often see both names in the same lawsuit or collection notice.

What is the 2015 CFPB consent order and does it affect me?

The 2015 consent order required MCM to follow specific rules: have proper documentation before suing, provide required disclosures to consumers, and stop collecting on time-barred debts without disclosures. The 2020 settlement extended these requirements through at least 2025. If MCM is violating these rules with you today — which the 2024 CFPB complaint data suggests is still happening — you have grounds for a complaint and potentially a legal claim.

Do You Need a Lawyer?

Quick Answer: You don’t need a lawyer to send a debt verification letter or file a CFPB complaint. But if MCM has sued you or you believe they violated the FDCPA or TCPA, a free consultation with a consumer rights attorney is strongly recommended — and FDCPA/TCPA attorneys typically charge nothing upfront.

When to Handle It Yourself

If you’ve received an initial collection letter and want to verify the debt, you can do that yourself. Write a clear, professional letter requesting debt validation, send it certified mail, and keep the receipt. You don’t need legal help for that first step.

When to Get Legal Help

Get an attorney involved immediately if:

- MCM has filed a lawsuit against you

- MCM is calling your cell phone repeatedly (potential TCPA claim)

- MCM contacted your employer, family members, or neighbors

- You believe the debt isn’t yours or is past the statute of limitations

- MCM threatened legal action they haven’t taken (and the threat appears false)

- MCM’s letters contain misleading information about your rights or the debt status

Free Legal Consultation

Many consumer rights attorneys offer free consultations and take FDCPA/TCPA cases on contingency — you pay nothing, and MCM pays attorney fees if you win. You can search for consumer rights attorneys through the National Association of Consumer Advocates (NACA) at naca.net.

For attorney referrals, you can also contact: [email protected]

The Bottom Line

Midland Credit Management has a documented history of illegal debt collection practices spanning more than a decade, backed by federal enforcement actions, class action settlements, and state attorney general investigations totaling well over $70 million in penalties and consumer relief.

If MCM is contacting you today, that history matters. They’ve been caught collecting debts consumers didn’t owe. They’ve been caught calling people without consent. They’ve been caught filing lawsuits without proper documentation. None of that means your situation is automatically a winner — but it does mean the law takes these violations seriously and gives you real tools to fight back.

Don’t pay a debt you can’t verify. Don’t ignore a lawsuit. Don’t assume MCM follows the rules. Check the statute of limitations. Document everything. And if something feels wrong, get a free legal consultation before you do anything else.

This article is for general informational purposes only and does not constitute legal advice. Laws vary by state and individual circumstances differ. Consult a licensed attorney about your specific situation.

Comments