If you’ve been sued by Jefferson Capital Systems, you’re holding legal papers with your name on them and a deadline you can’t ignore. Jefferson Capital Systems is a debt buyer that files thousands of lawsuits each year against consumers. The good news? You have legal rights and real options to fight back. This guide shows you exactly what to do, what defenses work, and how to protect yourself. hawthorne residential partners lawsuit

Quick Answer: Jefferson Capital Systems is a debt collection company that buys old debts and sues consumers to collect. If sued, you typically have 14-35 days to file an Answer with the court. Many cases get dismissed when you respond properly because debt buyers often lack the documentation to prove their case. You can defend yourself, negotiate a settlement, or fight the lawsuit in court. OGX Shampoo Lawsuit

What Is Jefferson Capital Systems?

Jefferson Capital Systems, LLC is a debt buyer based in St. Cloud, Minnesota. They’ve been in business since 2002 and currently claim to be the fourth-largest debt buyer in the United States.

Here’s how they operate: Jefferson Capital doesn’t lend money or issue credit cards. Instead, they buy charged-off debts from original creditors like banks, credit card companies, cell phone providers, and medical facilities. They typically pay just pennies on the dollar for these old accounts—sometimes as little as 1-10 cents per dollar of debt.

Once they buy your debt, Jefferson Capital steps in as the new creditor. They’ll try to collect the full amount from you, even though they paid a fraction of what you supposedly owe. If collection calls and letters don’t work, they’ll file a lawsuit to force you to pay.

Jefferson Capital Systems Company Details

| Information | Details |

|---|---|

| Legal Name | Jefferson Capital Systems, LLC |

| Headquarters | 200 14th Avenue East, Sartell, MN 56377 (formerly 16 McLeland Road, St. Cloud, MN) |

| Phone Number | 1-833-851-5552 |

| Parent Company | CL Holdings, LLC (previously owned by CompuCredit Corporation until 2012) |

| Business Type | Debt buyer and debt collector |

| Founded | 2002 |

| Other Locations | Minneapolis, MN; Denver, CO; International offices in UK and Canada |

| BBB Rating | A- (with 1,252 complaints in last 3 years as of January 2025) |

| CFPB Complaints | 1,314 complaints (3-year lookback as of January 2025) |

What Types of Debts Does Jefferson Capital Buy?

Jefferson Capital purchases charged-off consumer debts from various industries:

- Credit card debt – From major banks and credit card companies

- Personal loans – Including payday loans and installment loans

- Medical bills – From hospitals and medical providers

- Cell phone bills – From Verizon, AT&T, and other carriers

- Utility bills – Electric, gas, water, and cable companies

- Retail accounts – Store credit cards and financing

- Student loans – Private student loan debt (not federal loans)

- Gym memberships and subscriptions

- Auto deficiency balances – After vehicle repossession

You never opened an account with “Jefferson Capital Systems.” Your original debt was with someone else. They bought it, often years later, and now they’re coming after you for the full amount.

Why Is Jefferson Capital Suing You?

Jefferson Capital files lawsuits as a collection tactic. They know most people won’t respond, which makes it easy for them to win default judgments.

Here’s their playbook:

Step 1: Buy your old debt for pennies on the dollar

Step 2: Send collection letters and make phone calls

Step 3: If you don’t pay, file a lawsuit against you

Step 4: Hope you don’t respond to the lawsuit

Step 5: Get a default judgment when you fail to respond

Step 6: Use the judgment to garnish your wages or freeze your bank account

The biggest mistake you can make is ignoring the lawsuit. When you don’t respond, Jefferson Capital wins automatically—even if their case is weak or they can’t actually prove you owe the debt.

Common Reasons Jefferson Capital Sues

| Reason | Explanation |

|---|---|

| Debt validation ignored | You didn’t respond to their collection letters |

| Settlement negotiations failed | They couldn’t get you to agree to a payment plan |

| Statute of limitations still active | The debt is still new enough to sue (usually 3-6 years depending on your state) |

| Large enough debt amount | Usually over $500-$1,000; smaller debts aren’t worth the court filing fees |

| You’re employed | They research whether you have wages to garnish |

| You have bank accounts | They can freeze your accounts after winning a judgment |

What Happens When Jefferson Capital Sues You?

The lawsuit process begins when Jefferson Capital files a civil complaint in your local court. Here’s what happens step by step:

The Lawsuit Process Timeline

| Stage | Timeline | What Happens |

|---|---|---|

| Complaint Filed | Day 0 | Jefferson Capital files lawsuit with the court |

| Summons Served | Within 30 days | You receive summons and complaint (delivered by process server, sheriff, or certified mail) |

| Response Deadline | 14-35 days after service | You must file an Answer with the court |

| Default Judgment | If you don’t respond | Jefferson Capital wins automatically without a trial |

| Discovery | 30-90 days | Both sides request documents and evidence |

| Settlement Negotiations | Ongoing | You can negotiate at any time before trial |

| Trial | 3-12 months after filing | If no settlement, case goes to court |

| Judgment | After trial or by default | Court decides who wins |

| Post-Judgment Collection | Immediately after judgment | Wage garnishment, bank levy, property liens |

You’ll Receive Two Documents

When you’re served with a lawsuit, you’ll get:

1. Summons – This is the official notice that you’re being sued. It tells you:

- Which court the case is in

- Your case number

- The deadline to respond (THIS IS CRITICAL)

- What happens if you don’t respond

2. Complaint or Petition – This document lays out Jefferson Capital’s claims:

- How much they say you owe

- The original creditor’s name

- Account numbers (sometimes partial)

- When the debt supposedly originated

- Why they claim you owe the money

Read both documents carefully. Look for the response deadline—it’s usually prominently displayed on the summons.

Your Response Deadlines: DON’T MISS THESE DATES

Missing your deadline is the #1 reason people lose to Jefferson Capital. Here are the response deadlines by state and court type:

Response Deadlines by State

| State | Deadline to Respond | Court Type |

|---|---|---|

| Texas | 14 days | Justice of the Peace Court |

| Texas | 20 days (Monday after 20th day) | County or District Court |

| California | 30 days | All courts |

| Florida | 20 days | County Court |

| New York | 20-30 days | Depends on how served |

| Illinois | 30 days | Circuit Court |

| Georgia | 30 days | State/Magistrate Court |

| Pennsylvania | 20 days | Magisterial District Court |

| Ohio | 28 days | Municipal/Common Pleas |

| Most Other States | 20-30 days | Check your summons |

⚠️ CRITICAL: Your summons will state the exact deadline. Count from the date you were served, not the filing date. If the deadline falls on a weekend or holiday, it usually extends to the next business day—but don’t count on this. File early.

How to Defend Yourself Against a Jefferson Capital Lawsuit

You have multiple ways to fight back. The best strategy depends on your specific situation.

Defense Strategy #1: File an Answer to the Lawsuit

Filing an Answer is your first and most important step. This is a legal document you file with the court that says “I’m fighting this lawsuit.”

What an Answer does:

- Stops a default judgment from being entered against you

- Forces Jefferson Capital to prove their case

- Preserves all your legal rights and defenses

- Shows you’re not an easy target

- Opens the door to settlement negotiations

What to include in your Answer:

- Response to each claim in the Complaint (admit, deny, or state you lack knowledge)

- Affirmative defenses (reasons the lawsuit should be dismissed)

- Any counterclaims if Jefferson Capital violated your rights

Many people use online services like SoloSuit to create their Answer in 15 minutes. Or you can hire a debt defense attorney to file it for you. Hello Toothpaste Lawsuit

Defense Strategy #2: Demand Debt Validation and Proof

Jefferson Capital has the burden of proof. They must prove:

- You are the person who owes the debt

- Jefferson Capital owns the debt (complete chain of assignment from original creditor to them)

- The amount they claim is accurate

- They have the legal right to sue you

Most debt buyers struggle with #2 and #3. Debts get sold multiple times, and the documentation gets lost or incomplete.

Common Legal Defenses That Work

Here are the most powerful defenses against Jefferson Capital lawsuits:

| Defense | How It Works | Success Rate |

|---|---|---|

| Statute of Limitations Expired | Debt is too old to sue (3-6 years in most states) | Very High if debt is truly time-barred |

| Lack of Standing | Jefferson Capital can’t prove they own the debt | High—many cases dismissed for this |

| Incorrect Amount | The amount claimed is wrong or inflated | Medium—forces negotiation |

| Mistaken Identity | The debt doesn’t belong to you | Very High if you can prove it |

| Debt Already Paid | You have proof you paid this debt | Very High with documentation |

| Discharged in Bankruptcy | Debt was included in bankruptcy | Very High—collection is illegal |

| FDCPA Violations | Jefferson Capital violated collection laws | Can result in counterclaim |

| Improper Service | Lawsuit wasn’t served correctly | Medium—may buy you time |

Defense Strategy #3: Raise Affirmative Defenses

Affirmative defenses are legal reasons the court should dismiss the case even if the debt is real. Include these in your Answer:

Statute of Limitations: If the debt is older than your state’s time limit, Jefferson Capital cannot legally sue you. This is one of the strongest defenses.

Statute of Limitations by State

| State | Written Contracts | Credit Cards | Most Common Debts |

|---|---|---|---|

| Texas | 4 years | 4 years | 4 years |

| California | 4 years | 4 years | 4 years |

| Florida | 5 years | 4 years | 4-5 years |

| New York | 6 years | 6 years | 6 years |

| Illinois | 10 years | 5 years | 5-10 years |

| Georgia | 6 years | 4-6 years | 4-6 years |

| Pennsylvania | 4 years | 4 years | 4 years |

| Ohio | 8 years (written) | 6 years | 6-8 years |

| North Carolina | 3 years | 3 years | 3 years |

| Michigan | 6 years | 6 years | 6 years |

Important: The statute of limitations starts from your last payment or last activity on the account. Making even a small payment can restart the clock.

Lack of Proof of Ownership: Jefferson Capital must provide a complete chain of title showing:

- Original creditor’s assignment to first debt buyer

- Each subsequent sale/assignment

- Final assignment to Jefferson Capital

If any link in the chain is missing, they can’t prove they have the right to sue.

Improper Documentation: Courts have dismissed cases where Jefferson Capital couldn’t produce:

- The original contract you signed

- Itemized statements showing how they calculated the amount

- Proper business records proving the debt exists

What Happens If You Don’t Respond?

Ignoring a Jefferson Capital lawsuit leads to serious consequences:

Default Judgment Consequences

| What Jefferson Capital Can Do | How It Affects You |

|---|---|

| Wage Garnishment | Up to 25% of your paycheck taken directly (varies by state; Texas limits this for consumer debts) |

| Bank Account Levy | Your bank account frozen and money seized |

| Property Liens | Lien placed on your house or property |

| Vehicle Seizure | In some states, your car can be seized |

| Credit Report Damage | Judgment appears on credit report for 7+ years |

| Additional Fees | Court costs, interest, and attorney fees added to your debt |

| Renewal of Judgment | Judgment can be renewed for additional 5-10 years |

In Texas, wages cannot be garnished for consumer debt, but bank accounts can still be levied.

In most other states, Jefferson Capital can garnish up to 25% of your disposable income (the amount left after taxes and required deductions).

How to Negotiate a Settlement with Jefferson Capital

Jefferson Capital bought your debt for pennies on the dollar. This means they’re often willing to settle for far less than the full amount they’re suing you for.

Settlement Strategies That Work

1. File Your Answer First

Never negotiate until after you’ve filed an Answer to the lawsuit. Why? Because once you file, you have leverage. Jefferson Capital now has to:

- Prove their case

- Spend money on attorney fees

- Risk losing if they can’t prove ownership

This puts you in a much stronger bargaining position.

2. Start with a Low Offer

Debt collectors often accept 30-50% of the claimed amount. Start even lower—offer 20-30% and negotiate up.

Example: If Jefferson Capital is suing you for $2,000, start by offering $400-$600. They may counter at $1,000, and you might settle for $700-$800.

3. Request Documentation First

Before you pay anything, demand that Jefferson Capital prove:

- They own the debt

- The amount is accurate

- All charges are legitimate

If they can’t provide proof, don’t pay. Use this as leverage.

4. Get Everything in Writing

NEVER agree to anything verbally. Require:

- Written settlement agreement signed by Jefferson Capital

- Statement that they’ll dismiss the lawsuit upon payment

- Confirmation of the exact settlement amount

- Payment method and deadline

- Agreement that the debt will be reported as “settled” or “paid” to credit bureaus

5. Pay Only When You Have the Written Agreement

Do not send money until you have a signed settlement agreement. Scammers and unscrupulous collectors will take your money and still pursue the judgment.

Typical Settlement Amounts

| Original Debt Amount | Typical Settlement Range | Aggressive Settlement |

|---|---|---|

| $500-$1,000 | $150-$400 (30-40%) | $100-$200 (20-30%) |

| $1,000-$3,000 | $400-$1,200 (30-40%) | $300-$700 (20-30%) |

| $3,000-$5,000 | $1,200-$2,500 (30-50%) | $900-$1,500 (20-30%) |

| $5,000-$10,000 | $2,000-$5,000 (30-50%) | $1,500-$3,000 (20-30%) |

| Over $10,000 | $4,000-$7,000 (30-50%) | $3,000-$5,000 (20-30%) |

Remember: Jefferson Capital paid 1-10 cents per dollar for your debt. Even if you settle at 30%, they’re still making a profit.

Your Rights Under the Fair Debt Collection Practices Act (FDCPA)

The FDCPA is a federal law that protects you from abusive debt collection practices. Jefferson Capital must follow these rules:

What Debt Collectors CANNOT Do

Jefferson Capital and their attorneys are prohibited from:

Harassment:

- Calling you before 8 AM or after 9 PM

- Calling you repeatedly to harass or annoy you

- Using obscene or profane language

- Threatening violence or harm

- Publishing your name as someone who doesn’t pay debts

False Statements:

- Lying about how much you owe

- Falsely claiming to be an attorney or government official

- Threatening legal action they don’t intend to take

- Claiming you committed a crime

- Sending fake legal documents

Unfair Practices:

- Collecting more than you actually owe

- Depositing post-dated checks early

- Threatening to seize your property illegally

- Contacting you at work if they know your employer prohibits it

Privacy Violations:

- Discussing your debt with third parties (except your spouse or attorney)

- Sending postcards about your debt

- Calling your family, friends, or employer about the debt

What to Do If Jefferson Capital Violates the FDCPA

If Jefferson Capital breaks these rules, you can:

- File a complaint with:

- Consumer Financial Protection Bureau (CFPB): www.consumerfinance.gov/complaint

- Federal Trade Commission (FTC): www.ftc.gov/complaint

- Your state Attorney General’s office

- Sue them for FDCPA violations:

- You can recover up to $1,000 per violation

- Plus actual damages (emotional distress, lost wages, etc.)

- Plus attorney fees (the court makes Jefferson Capital pay your lawyer)

- You have one year from the violation to file

- Use violations as a defense in their lawsuit against you:

- FDCPA violations can lead to case dismissal

- You can file a counterclaim for damages

Many debt defense attorneys work on contingency for FDCPA cases, meaning you don’t pay unless you win.

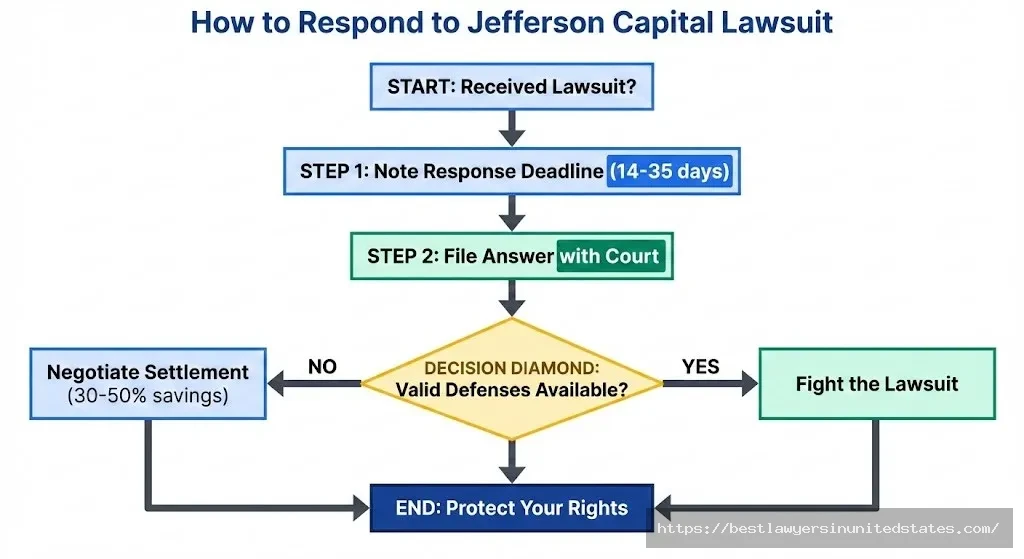

Step-by-Step: How to Respond to a Jefferson Capital Lawsuit

Here’s exactly what to do when you’re served with a lawsuit:

Step 1: Read the Summons and Complaint Immediately

Don’t put it aside. Read both documents carefully and note:

- Your response deadline

- The court’s name and address

- Your case number

- The amount they’re claiming

- The original creditor’s name

Step 2: Calculate Your Response Deadline

Count the days from when you were served. Mark the deadline on your calendar, phone, and everywhere you’ll see it.

Pro tip: File your Answer at least 3-5 days early in case there are issues with the court’s filing system.

Step 3: Gather All Documents Related to the Debt

Collect everything you have:

- Collection letters from Jefferson Capital

- Letters from the original creditor

- Account statements

- Payment records

- Emails or correspondence

- Credit card agreements

If you don’t have documentation, that’s okay. Jefferson Capital has to prove their case, not you.

Step 4: Request Debt Validation (If You Haven’t Already)

Send a debt validation letter to Jefferson Capital demanding:

- Proof they own the debt

- The original creditor’s name and account number

- Itemization of the amount claimed

- Copy of the original contract

- Complete chain of assignment

Send this letter via certified mail with return receipt.

Step 5: Decide Your Defense Strategy

Based on your situation, choose your approach:

Option A: Fight the lawsuit if:

- The debt is past the statute of limitations

- You don’t recognize the debt

- The amount is wrong

- You already paid it

- It was discharged in bankruptcy

- Jefferson Capital lacks proper documentation

Option B: Negotiate a settlement if:

- The debt is valid and recent

- Jefferson Capital has proper documentation

- You can afford to pay a reduced amount

- You want to resolve it quickly

Option C: File for bankruptcy if:

- You have multiple debts you can’t pay

- Creditors are garnishing your wages

- You’re being sued by multiple companies

- Your financial situation is overwhelming

Step 6: File Your Answer with the Court

Your Answer must be filed by the deadline. Here’s how:

If filing yourself:

- Download or obtain the proper Answer form from your court’s website

- Fill it out responding to each allegation in the Complaint

- Include your affirmative defenses

- Make 2-3 copies (one for you, one for the court, one for Jefferson Capital’s attorney)

- File with the court clerk (in person or by mail)

- Get a file-stamped copy

- Mail a copy to Jefferson Capital’s attorney

If using an online service:

- SoloSuit and similar services can generate your Answer for $100-$300

- They handle formatting and filing instructions

- Faster and easier than doing it yourself

If hiring an attorney:

- Attorney files the Answer for you

- Usually costs $500-$1,500 depending on complexity

- Attorney can also negotiate settlement

Step 7: Participate in Discovery

After you file your Answer, Jefferson Capital will likely send you discovery requests:

Interrogatories: Written questions you must answer under oath

Request for Production: Demand for documents related to the debt

Request for Admissions: Statements you must admit or deny

You must respond to these within the deadline (usually 30 days). If you don’t respond, the court may rule against you.

Pro tip: Use discovery to your advantage. Send interrogatories and document requests to Jefferson Capital demanding:

- Complete proof they own the debt

- All account statements

- Original signed contract

- Assignment documents

- Payment history

Many times, they can’t produce these documents, which weakens their case.

Step 8: Attend All Court Hearings

If your case goes to court, show up. Even if you don’t have an attorney, you must appear.

What to bring:

- All documents related to the debt

- Your filed Answer

- Any evidence supporting your defenses

- Photo ID

- Notebook and pen

The judge will listen to both sides and make a decision. Be respectful, honest, and clear when presenting your case.

When Should You Hire a Lawyer?

You can defend yourself against a Jefferson Capital lawsuit, but hiring an attorney significantly improves your chances. AFFF Lawsuit

Consider Hiring a Lawyer If:

| Situation | Why You Need a Lawyer |

|---|---|

| Large debt amount (over $5,000) | Stakes are high; attorney fees are worth it |

| Complex legal issues | Multiple defenses, bankruptcy considerations |

| Jefferson Capital has strong documentation | Need professional negotiation skills |

| You’re already being garnished | Urgent need to stop collection |

| FDCPA violations occurred | Attorney can file counterclaim for damages |

| You don’t understand legal procedures | Mistakes can cost you the case |

| Settlement negotiations failed | Need aggressive representation |

| Multiple lawsuits pending | Coordinated defense strategy needed |

How Much Does a Debt Defense Lawyer Cost?

| Fee Structure | Typical Cost | When It’s Used |

|---|---|---|

| Flat Fee | $500-$2,500 | Most debt defense cases |

| Hourly Rate | $150-$400/hour | Complex cases |

| Contingency | No upfront cost (25-40% of damages) | FDCPA violation counterclaims |

| Free Consultation | $0 | Initial case review |

Many debt defense attorneys offer payment plans. Some work on contingency for FDCPA violations, meaning you pay nothing unless you win.

How to Find a Qualified Debt Defense Attorney

1. Search for consumer rights or debt defense attorneys in your area

Websites to use:

- National Association of Consumer Advocates (NACA): www.consumeradvocates.org

- Your state bar association’s lawyer referral service

- Avvo: www.avvo.com

- Martindale: www.martindale.com

2. Ask these questions during consultation:

- How many debt collection cases have you handled?

- What’s your success rate against debt buyers like Jefferson Capital?

- What are your fees and payment options?

- What defense strategy do you recommend for my case?

- How long will the process take?

- Will you handle all court appearances?

3. Check their credentials:

- Licensed to practice law in your state

- No disciplinary actions (check your state bar website)

- Experience with debt collection defense

- Positive client reviews

4. Get it in writing:

- Written fee agreement

- Clear scope of representation

- What services are included

- Payment schedule

Alternative Option: Bankruptcy

If you’re drowning in debt from multiple creditors, bankruptcy might be a better option than fighting individual lawsuits.

Chapter 7 Bankruptcy

What it does: Wipes out most unsecured debts, including credit cards, medical bills, and personal loans.

Cost: $300-$400 filing fee plus $1,000-$3,000 attorney fees

Timeline: 3-4 months from filing to discharge

Effect on Jefferson Capital lawsuit: The lawsuit is immediately stopped by an automatic stay. The debt is discharged and Jefferson Capital cannot collect.

Chapter 13 Bankruptcy

What it does: Creates a 3-5 year repayment plan for your debts.

Cost: $300-$400 filing fee plus $2,500-$5,000 attorney fees

Timeline: 3-5 years

Effect on Jefferson Capital lawsuit: Lawsuit is stopped. Jefferson Capital becomes part of your repayment plan.

Should You File Bankruptcy?

Bankruptcy makes sense if:

- You owe more than $10,000 in total unsecured debt

- You’re being sued by multiple creditors

- You can’t afford minimum payments

- Creditors are garnishing your wages

- You have no assets to protect

Bankruptcy stays on your credit report for 7-10 years, but it gives you a fresh start.

Frequently Asked Questions

Can Jefferson Capital garnish my wages?

It depends on your state. Jefferson Capital can only garnish your wages if they win a judgment against you. In Texas, wage garnishment is not allowed for consumer debts. In most other states, they can garnish up to 25% of your disposable income after getting a court judgment.

How do I know if the lawsuit is real or a scam?

Real lawsuits are served by a process server, sheriff, or sent via certified mail. To verify, call the court clerk listed on the summons and provide your case number. Never call phone numbers on the documents themselves—look up the court’s official number online. Scammers demand immediate payment via gift cards or wire transfers, while real lawsuits give you time to respond.

What if I never got served but Jefferson Capital says they sued me?

If you weren’t properly served, the lawsuit may be invalid. Check with the court using the case number. If they claim you were served but you weren’t, you may be able to challenge the service. File a motion to quash service or vacate any default judgment entered against you.

Can I go to jail for not paying Jefferson Capital?

No. You cannot go to jail for consumer debt. Debt collection is a civil matter, not criminal. However, if you ignore a court order to appear or violate other court orders, you could face contempt charges. As long as you respond to the lawsuit and participate in the legal process, you will not face jail time.

What happens if I move to another state after being sued?

The lawsuit follows you. Jefferson Capital can pursue the judgment in your new state through a process called “domestication” of judgment. It’s better to deal with the lawsuit in the state where it was filed rather than avoid it.

How long does Jefferson Capital have to sue me?

It depends on your state’s statute of limitations, which ranges from 3-6 years for most consumer debts. The clock starts from your last payment or last activity on the account. After the statute expires, Jefferson Capital can still try to collect, but they cannot legally sue you.

Will responding to the lawsuit hurt my credit?

No. Filing an Answer does not hurt your credit. The lawsuit itself may already be reported on your credit report by the court. Fighting the lawsuit can actually help if you get the case dismissed—dismissed cases can sometimes be removed from your credit report.

Can I negotiate with Jefferson Capital after I file my Answer?

Yes. You can negotiate a settlement at any time during the lawsuit process. In fact, filing your Answer gives you more leverage because Jefferson Capital now has to prove their case. Many debt collectors prefer to settle rather than go through a trial.

What if I already made a payment to Jefferson Capital?

Making a payment does not mean you admit to owing the full amount. It also restarts the statute of limitations on the debt. If you’ve already paid something, keep all receipts and documentation. This doesn’t prevent you from fighting the lawsuit, but it does show you acknowledged the debt.

Do I need to show up to court if I filed an Answer?

Yes. If the case goes to trial, you must appear in court. Even if you have an attorney representing you, it’s best to attend. If you don’t show up, the judge may issue a default judgment against you.

Can Jefferson Capital sue me for a debt that’s been charged off?

Yes. “Charged off” means the original creditor wrote off the debt as a loss for tax purposes. It doesn’t mean you don’t owe it. Jefferson Capital buys these charged-off debts and can legally sue to collect them if the statute of limitations hasn’t expired.

What if the debt is from a joint account?

If the original debt was a joint account (like a joint credit card with a spouse or family member), both people are responsible. Jefferson Capital can sue either or both of you. If you get sued, you can claim the other person should pay, but you’re both legally liable.

How do I prove the statute of limitations has expired?

You need to know the date of your last payment or last activity on the account. Check old bank statements, credit reports, or letters from the original creditor. If you can’t find this information, request it from Jefferson Capital during discovery. The burden is on you to raise the statute of limitations as a defense.

Can Jefferson Capital add interest to the debt?

It depends on your state law and the original contract. Some states allow post-charge-off interest; others don’t. Jefferson Capital often adds fees and interest to the original amount. You can challenge these charges if they’re not supported by your original agreement or state law.

What happens if I win the lawsuit?

If you win, the case is dismissed and Jefferson Capital cannot collect the debt through that lawsuit. They also can’t report the judgment on your credit report. However, they may try to sue you again if they fix the problems in their case, or they may sell the debt to another collector.

What should I do if I lost my job and can’t afford to pay?

Tell the court about your financial hardship. If you lose the lawsuit, you can file for a hardship exemption to protect your income and assets from garnishment. If you’re truly unable to pay, Jefferson Capital may accept a much lower settlement or agree to a payment plan.

Can Jefferson Capital take my tax refund?

Private debt collectors like Jefferson Capital cannot garnish your federal tax refund. Only the IRS, state tax agencies, and certain government entities (child support, student loans) can seize tax refunds. However, if Jefferson Capital gets a judgment and you deposit your refund in a bank account, they can levy that account.

How do I remove a Jefferson Capital judgment from my credit report?

If you win the case, the judgment shouldn’t appear on your credit report. If it does, dispute it with the credit bureaus. If you lost but paid the judgment, it will show as “satisfied” but remain on your report for 7 years from the filing date. You can’t remove accurate information, but you can negotiate with Jefferson Capital to request deletion as part of a settlement.

What if I think Jefferson Capital violated the FDCPA?

Document everything: dates, times, what was said, who called, and any threats or false statements. File a complaint with the CFPB and your state Attorney General. Consider consulting a consumer rights attorney who can file a lawsuit on your behalf. FDCPA violations can result in Jefferson Capital paying you damages plus your attorney fees.

Can I represent myself in court against Jefferson Capital?

Yes. Many people successfully defend themselves against debt collectors without an attorney. However, having legal representation significantly improves your odds, especially if the debt is large or Jefferson Capital has strong documentation. If you represent yourself, thoroughly research your state’s laws and court procedures.

Final Thoughts: Take Action Today

Jefferson Capital Systems files thousands of lawsuits every year. They win most of them by default because people don’t respond.

Don’t be part of that statistic.

If you’ve been served with a lawsuit:

- Note your response deadline immediately

- Gather all documents related to the debt

- File an Answer with the court before the deadline

- Raise all available defenses

- Demand proof that Jefferson Capital owns the debt

- Negotiate a settlement from a position of strength

- Consider hiring a debt defense attorney

You have rights. Use them.

Even if you owe the debt, Jefferson Capital must prove their case. Many lawsuits get dismissed because debt buyers can’t produce proper documentation. And even when they can prove ownership, you can often settle for 30-50% of what they’re claiming.

The worst thing you can do is nothing. An ignored lawsuit becomes a judgment, which becomes garnished wages and frozen bank accounts.

Take action today. Your financial future depends on it.

Need legal help? Contact a debt defense attorney for a free consultation. Most offer payment plans and some work on contingency for FDCPA violations.

Want to file your Answer yourself? Services like SoloSuit can help you create and file your Answer in minutes.

Filing bankruptcy? Consult with a bankruptcy attorney to explore whether Chapter 7 or Chapter 13 is right for you.

Whatever you choose, don’t wait. Your deadline is approaching.

Comments