The Affirm lawsuit is one of the biggest consumer lending cases making headlines in 2026. Multiple legal actions accuse Affirm Holdings Inc of hiding fees, inflating interest rates, and misleading millions of buy now pay later customers.

If you’ve ever used Affirm to split a purchase into payments, you could be affected. Some consumers report being charged interest they never agreed to. Others say Affirm damaged their credit scores without proper notice.

This article covers every detail you need. You’ll learn what the lawsuits allege, who qualifies, how much money you might receive, and exactly how to file a claim before the deadline. Over 49 million Affirm accounts have been opened since the company launched, and a significant number of those users may be eligible for compensation.

The stakes are high. The information here is current as of 2026.

What Is the Affirm Lawsuit About

The Affirm lawsuit is a collection of legal actions accusing Affirm Holdings Inc of deceptive lending practices. At its core, plaintiffs say Affirm promised “no hidden fees” but charged consumers undisclosed costs.

Affirm markets itself as a transparent alternative to credit cards. The company lets shoppers split purchases into installments at checkout. But several lawsuits claim that transparency was a lie.

Plaintiffs allege three main categories of harm:

- Hidden finance charges that weren’t disclosed before purchase

- Misleading APR rates that jumped higher than advertised

- Credit score damage from hard pulls and late payment reporting consumers didn’t authorize

The cases have been filed in multiple federal courts. The primary case sits in the U.S. District Court for the Northern District of California, where Affirm is headquartered in San Francisco.

| Detail | Info |

|---|---|

| Defendant | Affirm Holdings Inc |

| Headquarters | San Francisco, CA |

| Primary Court | N.D. California |

| Core Allegation | Deceptive lending practices |

| Laws Cited | Truth in Lending Act, EFTA |

Think of it like ordering a meal where the menu says “no extra charges,” but your bill comes back 30% higher than expected. That’s essentially what Affirm users are alleging happened to them.

Affirm Lawsuit 2026: What’s New This Year

The Affirm lawsuit in 2026 has entered a critical phase. Several cases have survived motions to dismiss, meaning courts found enough evidence to let them proceed.

Early in 2026, a federal judge denied Affirm’s attempt to force all claims into individual arbitration. That ruling was a turning point. It means consumers can band together in a class action rather than fighting Affirm one by one.

The CFPB also ramped up its investigation into Affirm’s lending disclosures this year. New regulatory pressure has pushed Affirm toward potential settlement discussions.

Key developments in 2026 include:

- January 2026: Court denied Affirm’s motion to compel arbitration in lead class action

- March 2026: CFPB issued civil investigative demand to Affirm for lending records

- May 2026: Amended complaint added new claims under state consumer protection laws

- July 2026: Settlement mediation discussions reportedly began

These developments make 2026 the most important year yet for affected consumers. The window to file claims could open soon.

Affirm Class Action Lawsuit Explained

An Affirm class action lawsuit allows thousands of affected users to sue together as one group. Instead of each person hiring a lawyer and filing separately, a small number of lead plaintiffs represent everyone.

Class actions work well for cases like this. Most individual Affirm users might only be owed $50 to $500. That’s not enough to justify a solo lawsuit. But when you multiply that by millions of users, the total becomes enormous.

The lead class action case was filed by consumers in California, New York, and Texas. They represent a proposed class of all U.S. residents who used Affirm’s installment payment services and were charged undisclosed fees or interest.

| Class Action Detail | Info |

|---|---|

| Case Type | Consumer class action |

| Lead Plaintiffs | Consumers from CA, NY, TX |

| Proposed Class | All U.S. Affirm users charged undisclosed fees |

| Class Size Estimate | Potentially millions of users |

| Status | Class certification pending |

Class certification is the next big hurdle. If the court certifies the class, every qualifying Affirm user becomes part of the lawsuit automatically. You don’t have to do anything unless you want to opt out.

Key Takeaway: Multiple lawsuits against Affirm have gained serious traction in 2026, with courts allowing cases to proceed, the CFPB investigating, and class certification on the horizon for millions of affected users.

Is There a Lawsuit Against Affirm Right Now

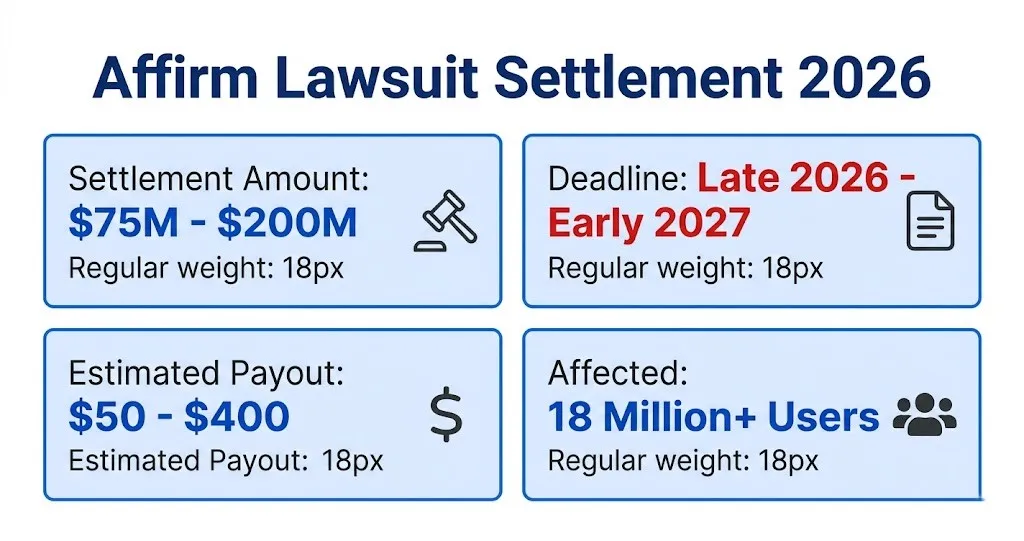

Yes, there are active lawsuits against Affirm in 2026. At least five separate legal actions are currently pending in federal and state courts across the country.

The most significant case is the consolidated class action in the Northern District of California. But individual lawsuits and state attorney general investigations are running parallel to that case.

Here’s a snapshot of the active legal actions:

- Federal class action in N.D. California (consolidated consumer claims)

- State court action in New York Supreme Court (state consumer protection violations)

- CFPB enforcement investigation (federal regulatory probe)

- State AG inquiries from at least three states (Illinois, Massachusetts, Pennsylvania)

- Individual arbitration claims filed by consumers who signed arbitration agreements

Not all of these are traditional “lawsuits” in the courtroom sense. The CFPB investigation and state AG probes are regulatory actions. But they carry real consequences for Affirm. Regulatory penalties can reach into the hundreds of millions.

If you’ve been wondering whether Affirm is really being sued, the answer is a definitive yes.

Affirm Lawsuit Update 2026

The latest Affirm lawsuit update shows the case moving toward resolution. As of mid-2026, settlement talks between Affirm and plaintiffs’ attorneys have reportedly begun.

Court filings from the spring reveal that both sides agreed to enter mediation. A retired federal judge was appointed as mediator. This is a strong signal that Affirm may want to settle rather than risk a trial.

The amended complaint filed in May 2026 expanded the claims significantly. Plaintiffs added allegations under the laws of 14 additional states. That move broadened who qualifies and increased Affirm’s potential financial exposure.

| Timeline | Event |

|---|---|

| Q1 2026 | Arbitration motion denied |

| Q2 2026 | Amended complaint filed; mediation ordered |

| Q3 2026 | Settlement negotiations underway |

| Q4 2026 (expected) | Preliminary settlement or trial date set |

One important note: Affirm’s stock price dropped 12% following the arbitration ruling in January 2026. Investors are watching this closely because a large settlement would directly impact the company’s bottom line.

Affirm Hidden Fees Lawsuit Details

The Affirm hidden fees lawsuit centers on charges consumers say they never knew about. Plaintiffs claim Affirm’s checkout process buried fee disclosures in fine print or displayed them only after the purchase was already confirmed.

Specific hidden fee allegations include:

- Late payment fees that weren’t clearly disclosed at checkout

- Merchant processing fees passed through to consumers indirectly

- Returned payment fees charged without adequate prior notice

- Interest charges on loans that were advertised as “0% APR”

The irony is thick. Affirm built its entire brand on the promise of “no hidden fees.” The company’s own advertising says, “We never charge hidden fees or late fees.” But the lawsuits tell a very different story.

According to court filings, some consumers were charged fees ranging from $5 to $35 per occurrence that they didn’t expect. For users with multiple Affirm loans, those charges added up fast.

One plaintiff described finding $287 in unexpected charges across six Affirm purchases over 18 months. She only discovered them by reviewing her bank statements line by line.

| Fee Type | Alleged Range | Disclosure Issue |

|---|---|---|

| Late Payment | $5 to $25 | Not shown at checkout |

| Returned Payment | $15 to $35 | Buried in terms |

| Interest on “0% APR” | Varies | Appeared after purchase |

| Processing Surcharge | $3 to $10 | Passed through silently |

Key Takeaway: The hidden fees allegations strike at the heart of Affirm’s brand promise, with plaintiffs documenting unexpected charges ranging from a few dollars to hundreds across multiple transactions.

Affirm Interest Rate Lawsuit Claims

The Affirm interest rate lawsuit alleges the company charged APR rates far higher than what consumers agreed to at checkout. Some borrowers report seeing 0% APR at purchase but later discovering rates as high as 36% on their statements.

Affirm offers loans with rates from 0% to 36% APR depending on creditworthiness. The problem isn’t the range itself. The problem is what consumers say they were shown versus what they were actually charged.

Court documents include screenshots from plaintiffs showing a 0% APR offer at checkout. Their loan documents later reflected a 29.99% APR. Affirm has argued this was due to “real-time underwriting” that adjusts rates before final approval.

But plaintiffs say the bait-and-switch happened after they’d already committed to the purchase. By the time the real rate appeared, many felt locked in.

Key claims in the interest rate lawsuit:

- APR displayed at checkout didn’t match the final loan agreement

- Rate increases happened without clear consumer consent

- Affirm’s “prequalification” rates were misleading

- Some consumers weren’t shown the final rate until after the transaction processed

The Truth in Lending Act (TILA) requires lenders to disclose the actual APR before a consumer commits. If Affirm showed one rate and charged another, that’s a potential federal violation.

Affirm Deceptive Lending Lawsuit Allegations

The Affirm deceptive lending lawsuit goes beyond fees and interest. It targets Affirm’s entire lending model as fundamentally misleading to consumers.

Plaintiffs argue that Affirm presents itself as a “pay over time” convenience tool. In reality, they say it operates like a high-interest lender that profits from consumer confusion. The marketing emphasizes simplicity and transparency while the actual terms are complex and costly.

Specific deceptive lending claims include:

- Loan terms changed between prequalification and final approval without notice

- Payment schedules shifted causing consumers to miss payments they didn’t know were due

- Credit reporting practices damaged scores without consumers understanding the consequences

- Automatic payment withdrawals occurred on dates different from what was disclosed

One of the most troubling allegations involves Affirm’s partnerships with retailers. Plaintiffs say merchants pushed Affirm aggressively at checkout, but neither the merchant nor Affirm adequately explained the loan terms.

It’s like signing up for what looks like a layaway plan, only to find out you actually took out a personal loan with a bank you’ve never heard of. That’s the experience many consumers describe.

The lending partners behind Affirm loans include Cross River Bank and Celtic Bank. Some plaintiffs argue these banks share liability for the deceptive practices.

Affirm Buy Now Pay Later Lawsuit

The Affirm buy now pay later lawsuit is part of a broader wave of legal actions targeting the entire BNPL industry in 2026. But Affirm, as one of the largest BNPL providers in the U.S., faces the most scrutiny.

BNPL services exploded in popularity during 2020 and 2021. By 2023, Affirm processed over $20 billion in gross merchandise volume. That rapid growth happened faster than regulation could keep up.

The BNPL-specific claims against Affirm include:

- Encouraging consumers to take on debt they couldn’t afford

- Failing to assess ability to repay before approving loans

- Allowing consumers to stack multiple BNPL loans simultaneously

- Not reporting loan activity consistently to credit bureaus

| BNPL Industry Concern | Affirm-Specific Allegation |

|---|---|

| Debt stacking | Users allowed unlimited concurrent loans |

| Affordability checks | Minimal income verification |

| Credit reporting | Inconsistent reporting harmed some users |

| Young consumers | Marketing targeted users under 25 heavily |

The average Affirm user carries between 2 and 4 active loans at any given time, according to industry research. Plaintiffs argue that Affirm’s system was designed to encourage this kind of loan stacking.

Regulators worldwide are cracking down on BNPL. The UK introduced mandatory affordability checks. Australia tightened lending rules. The U.S. is following suit, and Affirm is in the crosshairs.

Key Takeaway: Affirm faces allegations spanning hidden fees, misleading interest rates, deceptive lending terms, and irresponsible BNPL practices, with regulators and courts applying increasing pressure in 2026.

Affirm CFPB Investigation and Regulatory Actions

The CFPB launched a formal investigation into Affirm’s lending and disclosure practices. In March 2026, the agency issued a civil investigative demand requiring Affirm to turn over years of lending records.

This isn’t Affirm’s first encounter with the CFPB. In 2023, Affirm was required to submit data to the CFPB as part of a broader BNPL market inquiry. The current investigation goes much further. It targets specific consumer harm.

The CFPB is examining:

- Whether Affirm’s APR disclosures comply with the Truth in Lending Act

- How Affirm handles consumer disputes and refunds

- Whether Affirm’s credit reporting practices violate the Fair Credit Reporting Act

- The adequacy of Affirm’s ability-to-repay assessments

A CFPB enforcement action could result in fines, mandatory consumer refunds, and changes to Affirm’s business model. The agency fined a competing BNPL company $40 million in 2025 for similar violations.

Separately, state attorneys general in Illinois, Massachusetts, and Pennsylvania have opened their own inquiries. These state-level actions could produce additional settlements or consent orders.

The regulatory walls are closing in. Affirm’s legal exposure in 2026 isn’t just from private lawsuits. It’s from the federal government and multiple state enforcement agencies too.

Affirm Lawsuit Eligibility Requirements

Affirm lawsuit eligibility depends on whether you experienced specific harms while using Affirm’s services. Not every Affirm user qualifies automatically.

To be eligible for the class action, you generally need to meet these criteria:

- You used Affirm’s installment payment service in the United States

- Your Affirm account was active between 2019 and 2025

- You were charged fees or interest rates that weren’t clearly disclosed before your purchase

- You experienced credit score damage from Affirm’s reporting practices

- You had automatic payments withdrawn on incorrect dates or in incorrect amounts

| Eligibility Factor | Requirement |

|---|---|

| Location | U.S. resident |

| Account Period | 2019 to 2025 |

| Harm Type | Hidden fees, rate mismatch, credit damage |

| Proof Needed | Account statements, transaction records |

| Excluded | Users who already settled individually |

You don’t need to have filed a complaint with Affirm to be eligible. You also don’t need to have canceled your account. If you fit the class definition, you’re in.

One exception: consumers who previously settled individual arbitration claims with Affirm may be excluded. Check your email records for any past Affirm legal correspondence.

Who Qualifies for the Affirm Lawsuit

Who qualifies for the Affirm lawsuit comes down to one question: did Affirm charge you more than you expected or damage your credit without proper notice?

The broadest potential class includes anyone who:

- Made at least one purchase through Affirm’s platform

- Was charged a fee or interest rate not displayed at checkout

- Had a hard credit inquiry they didn’t authorize

- Received a late payment mark on their credit report from Affirm

Some specific groups may have stronger claims than others.

Strongest claims:

- Consumers who were shown 0% APR but charged interest

- Users who discovered hidden fees only after reviewing bank statements

- People whose credit scores dropped because of Affirm’s reporting

Moderate claims:

- Users charged late fees they weren’t warned about

- Consumers with auto-pay debited on wrong dates

Weaker claims (but still potentially eligible):

- Users who are unhappy with Affirm’s service but can’t document specific overcharges

The class hasn’t been officially certified yet. Once it is, the court will define exactly who is included. For now, if you have documentation of unexpected charges or credit damage, you’re likely a strong candidate.

Key Takeaway: Eligibility for the Affirm lawsuit centers on documented financial harm including hidden fees, rate discrepancies, and credit damage, with the broadest class potentially covering millions of U.S. consumers who used Affirm between 2019 and 2025.

Affirm Settlement Amount in 2026

The Affirm settlement amount hasn’t been officially announced yet. Settlement talks are ongoing as of mid-2026. But based on comparable BNPL and fintech settlements, analysts project a range.

Industry experts estimate Affirm’s total settlement exposure at $75 million to $200 million depending on the scope of the class and the strength of the evidence.

Here’s how that compares to similar fintech settlements:

| Company | Settlement Year | Amount | Users Affected |

|---|---|---|---|

| Afterpay | 2024 | $25 million | 2.1 million |

| PayPal (BNPL) | 2025 | $40 million | 3.8 million |

| Klarna (projected) | 2026 | $55 million | 5 million |

| Affirm (estimated) | 2026 | $75M to $200M | 10M+ |

Affirm’s potential settlement is higher because its user base is larger. The company reported over 18 million active users in its most recent earnings disclosure.

A settlement in the $100 million range seems most likely based on the case trajectory. That number could go higher if the CFPB adds its own penalties on top of the private class action settlement.

Keep watching for court filings in Q4 2026. A preliminary settlement agreement could drop before the end of the year.

Affirm Lawsuit Payout Estimates

Affirm lawsuit payout estimates depend on class size and how the settlement fund gets divided. Individual payments will vary based on how much each person was overcharged.

If the settlement lands at $100 million and 10 million users qualify, the average per-person payout would be roughly $10. But class action payouts rarely work that way. Not everyone files a claim.

Typically, only 5% to 15% of eligible class members submit claims. That dramatically increases the per-person payment for those who do file.

| Scenario | Settlement Fund | Claimants | Est. Payout Per Person |

|---|---|---|---|

| Low Estimate | $75 million | 1.5 million | $50 |

| Mid Estimate | $100 million | 1 million | $100 |

| High Estimate | $200 million | 750,000 | $267 |

| Best Case | $200 million | 500,000 | $400 |

Your individual payout could be higher if you:

- Had multiple Affirm loans with hidden charges

- Can document specific dollar amounts you were overcharged

- Experienced measurable credit score damage

- Filed a complaint with Affirm that went unresolved

People with heavy Affirm usage and strong documentation will likely receive the most. Casual one-time users with no evidence of harm will receive less.

How Much Will I Get from the Affirm Lawsuit

How much you’ll get from the Affirm lawsuit depends on your personal situation. Most claimants can expect somewhere between $50 and $400 based on current projections.

That range shifts based on a few factors.

Your payout goes up if:

- You had 3 or more Affirm loans with undisclosed charges

- You can show bank statements proving unexpected fees

- Your credit score dropped because of Affirm’s actions

- You complained to Affirm and have records of their response

Your payout goes down if:

- You only used Affirm once

- You can’t locate your account records

- You didn’t experience a fee or interest rate mismatch

- You signed an individual arbitration agreement and already settled

The settlement administrator will likely create a tiered payout structure. Tier 1 claimants with strong documentation get the most. Tier 3 claimants with minimal proof get a smaller flat payment.

Don’t let the dollar amount discourage you from filing. The claim process is free. It takes about 15 minutes. And you might end up with a check for a few hundred dollars simply for filling out a form and uploading a screenshot.

Key Takeaway: Individual payouts from the Affirm lawsuit are projected between $50 and $400, with higher amounts going to consumers who document multiple overcharges, credit damage, and unresolved complaints.

How to File an Affirm Lawsuit Claim

Filing an Affirm lawsuit claim is straightforward once the claims process opens. Here’s what to expect step by step.

Step 1: Verify your eligibility. Check whether you used Affirm during the relevant time period (2019 to 2025) and experienced hidden fees, interest discrepancies, or credit damage.

Step 2: Gather your documents. Pull your Affirm account history, bank statements showing Affirm charges, and any emails from Affirm about your loans.

Step 3: Complete the claim form. Once a settlement is approved, a claims administrator will publish an online form. Fill it out with your personal details and describe your experience.

Step 4: Upload supporting evidence. Attach screenshots, statements, or other documents that prove your claim.

Step 5: Submit and wait. After filing, the administrator reviews your claim. Payments go out after final court approval.

| Filing Step | What You Need |

|---|---|

| Eligibility Check | Affirm account from 2019 to 2025 |

| Documentation | Bank statements, loan agreements, emails |

| Claim Form | Personal info, harm description |

| Evidence Upload | Screenshots, PDFs, credit reports |

| Timeline | Claims expected to open late 2026 or early 2027 |

You won’t need a lawyer to file. Class action claims are designed for regular people to complete on their own.

Affirm Lawsuit Proof of Claim Requirements

Proof of claim for the Affirm lawsuit means showing evidence that Affirm overcharged you or harmed your credit. The stronger your proof, the higher your potential payout.

Here’s what counts as valid proof:

- Affirm account screenshots showing loan terms at checkout versus final terms

- Bank or credit card statements showing charges from Affirm you didn’t authorize or expect

- Credit reports showing hard inquiries or late payment marks from Affirm

- Email correspondence with Affirm customer service about billing disputes

- The Affirm app itself, where your loan history and payment records are stored

You don’t need all of these. Even one or two items can support your claim.

The best piece of evidence is a side-by-side comparison. Show what Affirm promised at checkout next to what actually appeared on your statement. If those numbers don’t match, that’s powerful proof.

Quick tip: Log into your Affirm account now and take screenshots of every loan, every payment, and every fee. If Affirm closes your account or changes its interface, you’ll lose access to that information.

Download your full transaction history as a PDF if the app allows it. Save it somewhere safe. This data is your leverage in the claims process.

Affirm Lawsuit Deadline You Need to Know

The Affirm lawsuit deadline for filing claims hasn’t been officially set yet. But based on the case timeline, consumers should expect a claims window opening in late 2026 or early 2027.

Once a settlement receives preliminary court approval, the claims administrator will set a specific filing deadline. Historically, BNPL and fintech settlement deadlines give consumers 60 to 120 days to submit claims after the window opens.

| Deadline Scenario | Estimated Date |

|---|---|

| Preliminary Settlement Approval | Q4 2026 |

| Claims Window Opens | Late 2026 to Early 2027 |

| Filing Deadline | 60 to 120 days after opening |

| Final Approval Hearing | Mid-2027 |

| Payments Distributed | Late 2027 |

Missing the deadline means losing your right to compensation. This is non-negotiable. Courts enforce claim deadlines strictly.

To stay informed about the deadline:

- Sign up for case notifications through the court’s electronic filing system (PACER)

- Monitor the settlement administrator’s website once it’s established

- Check consumer rights news outlets that track class action deadlines

- Save any notice you receive by mail or email from the claims administrator

The single most important thing you can do right now is gather your evidence while you still have access to your Affirm account. Don’t wait for the deadline announcement to start preparing.

Key Takeaway: While no official deadline has been set, the claims window is expected to open in late 2026 or early 2027 with a 60 to 120 day filing period, making it critical to gather evidence from your Affirm account now.

Frequently Asked Questions

Is there a class action lawsuit against Affirm in 2026?

Yes, multiple lawsuits are active against Affirm in 2026.

The primary class action is pending in the U.S. District Court for the Northern District of California.

Additional state-level actions and a CFPB investigation are also underway.

How much money can I get from the Affirm lawsuit?

Most claimants can expect between $50 and $400 per person.

The exact amount depends on your number of Affirm loans, documented overcharges, and credit damage.

Payments are expected to begin in late 2027 after final court approval.

Who qualifies for the Affirm class action lawsuit?

U.S. residents who used Affirm between 2019 and 2025 and were charged undisclosed fees or experienced credit damage may qualify.

You don’t need to have filed a prior complaint with Affirm.

Consumers who already settled individual arbitration claims may be excluded.

What is the deadline to file an Affirm lawsuit claim?

The official filing deadline hasn’t been set yet.

The claims window is expected to open in late 2026 or early 2027.

Consumers will likely have 60 to 120 days to submit their claims after the window opens.

How do I file a claim against Affirm?

You’ll file through an online claim form published by the settlement administrator.

Gather your Affirm account history, bank statements, and any fee-related emails before the form goes live.

No lawyer is needed to file a claim.

Right now is the time to prepare your Affirm lawsuit claim. Log into your account, screenshot every transaction, and save your loan records before anything changes.

The case is moving fast in 2026. Settlement talks are underway and a claims window could open within months.

Don’t sit on this. Gather your evidence today so you’re ready to file the moment the deadline is announced.