Quick Answer Box

- What the case is: Multiple concurrent legal actions challenge Bank of America’s mortgage record-keeping, including a $12 million CFPB penalty for falsified HMDA demographic data, a RESPA class action alleging denied record requests, and an ongoing federal appellate dispute over escrow interest payments.

- Who qualifies: Borrowers with BofA residential mortgages from 2016 to 2025 who were denied call recordings or requested documents, received false demographic data entries, or paid escrow interest in states where state law may require payment.

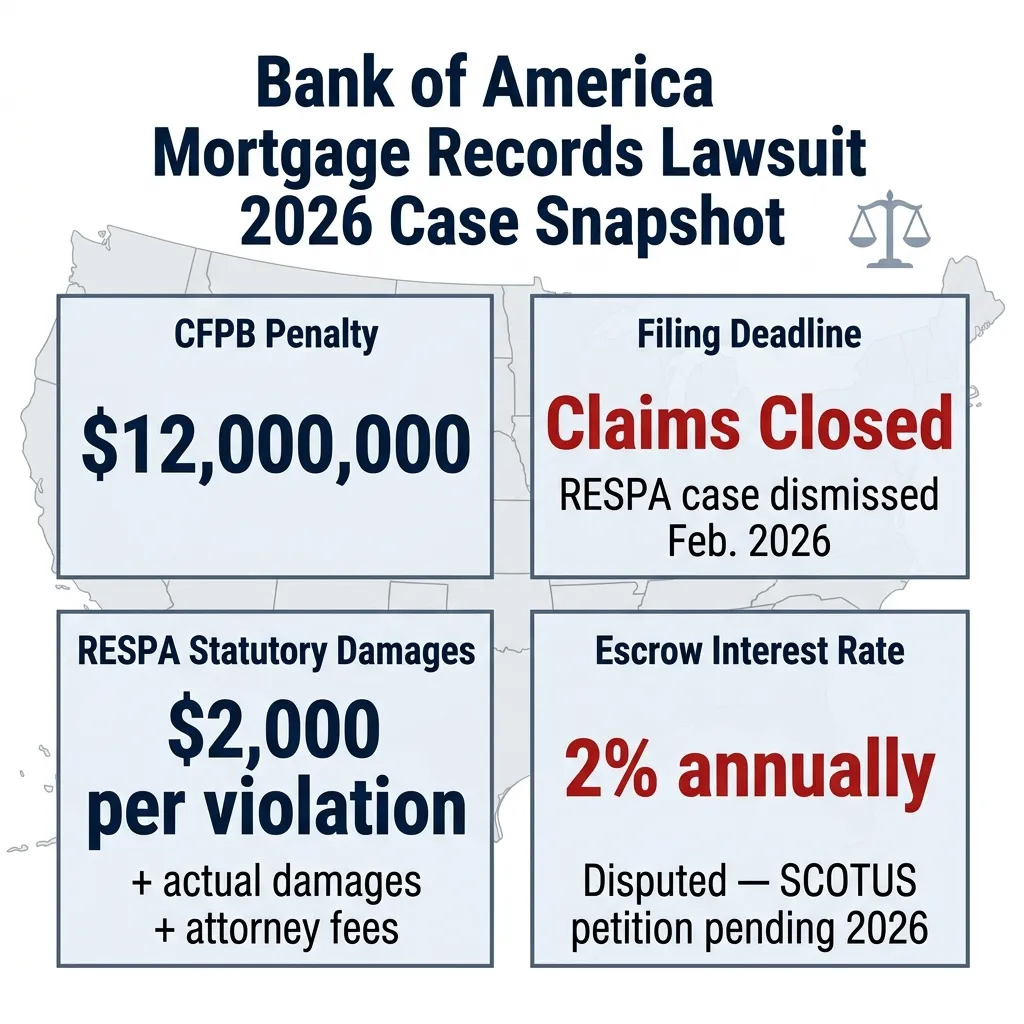

- What it’s worth: The CFPB extracted a 12million∗∗civilpenalty.IndividualRESPAstatutorydamagesreach∗∗12million∗∗civilpenalty.IndividualRESPAstatutorydamagesreach∗∗2,000 per violation plus actual damages and attorney’s fees. Escrow interest claims vary by state law and outstanding loan balance.

Case Snapshot

| Detail | Info |

|---|---|

| Court (HMDA Enforcement) | Consumer Financial Protection Bureau (Administrative Proceeding) |

| CFPB Docket No. | 2023-CFPB-0016 |

| Court (RESPA Class Action) | U.S. District Court, Southern District of Florida |

| Case No. (RESPA) | 0:25-cv-60136 |

| Presiding Judge (RESPA) | Judge Rodney Smith |

| RESPA Filing Date | January 2025 |

| RESPA Status | Dismissed Feb. 9, 2026; reconsideration motion filed March 2026 |

| HMDA Consent Order Date | November 28, 2023 |

| HMDA Order Terminated | June 5, 2025 |

| CFPB Penalty Amount | $12,000,000 |

| Escrow Case (Appellate) | Cantero v. Bank of America, N.A., 2d Cir. |

| Supreme Court Docket | No. 22-529 |

| Second Circuit Ruling | May 5, 2026 |

| New Certiorari Petition | Filed May 22, 2026 |

Bank of America is the subject of three distinct legal proceedings that directly affect residential mortgage borrowers. Each targets a different failure in how the bank handled mortgage records, reporting obligations, and escrow accounts.

The broadest regulatory action, CFPB Docket No. 2023-CFPB-0016, resulted in a $12 million penalty for falsified demographic data across at least four years of mortgage applications. A separate RESPA class action filed in January 2025 targeted the bank’s refusal to produce call recordings and respond to borrowers’ formal record requests.

The third front is appellate. On May 5, 2026, the U.S. Court of Appeals for the Second Circuit ruled in Cantero v. Bank of America that New York’s escrow interest law is preempted by federal banking law. A new Supreme Court petition followed on May 22, 2026.

These are not the same case. They involve different courts, different statutes, and different classes of potential plaintiffs. Understanding which case applies to a given borrower’s situation is the first task any competent attorney in this space will perform.

What Is the Bank of America Mortgage Records Lawsuit?

The bank of america mortgage records lawsuit is not a single filing. It is a category of legal actions alleging that Bank of America, N.A. systematically failed to maintain accurate mortgage records, respond lawfully to borrower document requests, and report required lending data truthfully to federal regulators.

Three primary legal theories form the foundation:

- HMDA violations: The bank falsely recorded that mortgage applicants declined to provide demographic information when, in fact, loan officers never asked.

- RESPA Section 6 violations: The bank failed to respond to qualified written requests and notices of error, and denied borrowers access to call recordings.

- Escrow account disputes: The bank refused to pay interest on mortgage escrow accounts in states where state law may require such payment.

Each theory generates a separate class of potential plaintiffs. A borrower affected by the HMDA false-entry problem is a different claimant from one whose requests for records were ignored.

Attorneys handling these claims point to the importance of identifying which specific legal theory applies before drafting any demand or filing, since the applicable statute of limitations, damage structure, and court vary significantly.

| Legal Theory | Governing Statute | Forum | Damages Structure |

|---|---|---|---|

| False demographic reporting | HMDA / Regulation C | CFPB Administrative | Civil penalty to victims fund |

| Record request denial | RESPA Section 6 | Federal District Court | $2,000 statutory + actual damages |

| Escrow interest withholding | State law / National Bank Act | Federal Appellate | Interest owed on escrow balance |

Bank of America Mortgage Lawsuit 2026: Where Things Stand Now

The litigation landscape as of June 2026 is in motion on multiple fronts. No single settlement fund is currently accepting consumer claims for the RESPA or HMDA matters.

The CFPB consent order (Docket No. 2023-CFPB-0016) closed on June 5, 2025, after Bank of America paid its $12 million penalty and submitted a HMDA compliance plan. That payment flowed into the CFPB’s victims relief fund, not directly to individual borrowers.

The RESPA class action (Warshaw v. Bank of America, Case No. 0:25-cv-60136) was dismissed by Judge Rodney Smith on February 9, 2026. The named plaintiff’s claims were dismissed with prejudice. Class claims were dismissed without prejudice, meaning other plaintiffs may refile. A motion for reconsideration was filed in March 2026 and, as of this writing, remains pending.

Attorneys handling these claims point to the March 2026 reconsideration motion as a potential inflection point. If the court reverses on class certification grounds, new plaintiffs could join a refiled action.

Key 2026 Dates

| Date | Event |

|---|---|

| November 28, 2023 | CFPB consent order issued against BofA (HMDA) |

| January 2025 | Warshaw v. BofA RESPA class action filed |

| June 5, 2025 | CFPB terminates consent order after full compliance |

| February 9, 2026 | Judge Smith dismisses Warshaw case |

| March 2026 | Plaintiff files motion for reconsideration |

| May 5, 2026 | Second Circuit rules for BofA in Cantero escrow case |

| May 22, 2026 | New Supreme Court petition filed in Cantero |

What Is the Bank of America HMDA False Records Lawsuit?

The HMDA enforcement action is the most documented case in this cluster. Between 2016 and 2021, hundreds of Bank of America loan officers failed to ask mortgage applicants the demographic questions required by the Home Mortgage Disclosure Act.

Rather than leaving those fields blank, the officers entered a false code indicating the applicant had declined to provide the information. The CFPB found this was a systemic, multi-year practice across multiple lending offices.

The CFPB issued its consent order on November 28, 2023, under Docket No. 2023-CFPB-0016. Bank of America was ordered to pay a $12 million civil money penalty to the CFPB’s victims relief fund and to implement a revised HMDA compliance management system.

Attorneys handling these claims point to the distinction between regulatory penalties and individual recovery: the $12 million went to the CFPB, not to a settlement fund that borrowers can claim from directly.

What the HMDA False-Entry Problem Means for Borrowers

- Borrowers whose race, ethnicity, or sex was falsely coded as “declined to state” have their data corrupted in the federal HMDA database.

- This data is used by regulators to assess fair lending compliance across the industry.

- Individual borrowers whose applications were affected may have grounds for separate ECOA or fair lending claims, depending on whether the false coding accompanied discriminatory treatment.

Bold Callout: The CFPB found the false recording practice spanned at least four years and involved “hundreds” of loan officers across Bank of America’s national mortgage operation.

CFPB Enforcement Action Against Bank of America Mortgage

The CFPB is the primary federal regulator that brought the largest documented action in this litigation cluster. Its November 28, 2023 consent order against Bank of America, N.A. established both the factual record and the penalty structure for the HMDA false-data case.

The order required Bank of America to:

- Pay $12 million into the CFPB’s victims relief fund

- Develop new policies and procedures governing HMDA data collection

- Submit a compliance plan reviewed by the CFPB

- Implement improvements to its HMDA compliance management system

The CFPB terminated the order on June 5, 2025, confirming that all obligations were met. The agency characterized the termination as a sign of completed compliance, not exoneration of underlying conduct.

Attorneys handling these claims point to CFPB enforcement records as a critical tool in private litigation. A completed consent order creates a documented admission of deficient practice that plaintiff’s counsel can reference.

CFPB Action at a Glance

| Element | Detail |

|---|---|

| CFPB Docket No. | 2023-CFPB-0016 |

| Order Date | November 28, 2023 |

| Penalty | $12 million |

| Recipient of Penalty | CFPB Victims Relief Fund |

| Order Terminated | June 5, 2025 |

| Basis | HMDA / Regulation C violations |

Litigation Watch: The CFPB’s documented finding that BofA loan officers falsely recorded demographic data for at least four years, as confirmed in Docket No. 2023-CFPB-0016, remains the most court-ready evidentiary record in any of these concurrent proceedings.

Who Qualifies for the Bank of America Mortgage Lawsuit?

Eligibility varies by which legal proceeding is relevant to a borrower’s specific situation. There is no single open claims portal as of June 2026.

HMDA False-Reporting Claims

Borrowers who applied for a Bank of America residential mortgage between 2016 and 2021 and whose demographic data may have been falsely recorded as “declined to state” are within the scope of the CFPB’s factual findings. Individual recovery through a private HMDA cause of action is limited; HMDA itself does not create a private right of action. However, the same conduct may support claims under the Equal Credit Opportunity Act (ECOA) if discriminatory treatment accompanied the false data entry.

RESPA Record-Request Claims

Borrowers who sent a formal qualified written request (QWR) or notice of error to Bank of America regarding their residential mortgage and:

- Were denied call recordings they requested

- Received a response past the legal deadline (typically 30 to 60 days under RESPA)

- Received a response with a misleading or false postmark date

…may have viable RESPA Section 6 claims.

Attorneys handling these claims point to the importance of documentation: the date a QWR was sent, how it was sent, and what response the borrower received are the three variables that determine whether a RESPA claim survives.

Escrow Interest Claims

Borrowers with BofA mortgages in states that have escrow interest statutes, including New York, are directly affected by the Cantero litigation. A Supreme Court certiorari petition filed May 22, 2026 means that outcome remains unresolved for New York borrowers.

| Claim Type | Who Qualifies | Statute |

|---|---|---|

| HMDA false data | 2016-2021 BofA mortgage applicants | HMDA / Regulation C |

| RESPA record request | Borrowers who sent a QWR and were denied or given false dates | RESPA Section 6 |

| Escrow interest | BofA borrowers in escrow-interest states (NY and others) | State law / NBA |

Warshaw v. Bank of America: The RESPA Class Action

Warshaw v. Bank of America, N.A. is the case most closely aligned with the “mortgage records” framing that many borrowers are searching for. Filed in January 2025 in the U.S. District Court for the Southern District of Florida, it carried docket number 0:25-cv-60136.

The named plaintiff, Lynne Warshaw, alleged that Bank of America:

- Failed to respond to qualified written requests within legal deadlines

- Refused to provide call recordings to which borrowers are entitled under RESPA

- Sent letters with misleading postmark dates to create the appearance of timely compliance

- Provided inaccurate information about response deadlines

On February 9, 2026, Judge Rodney Smith granted Bank of America’s motion to dismiss. The named plaintiff’s claims were dismissed with prejudice. The class claims were dismissed without prejudice. A motion for reconsideration was filed in March 2026 and remains pending.

Attorneys handling these claims point to the without-prejudice dismissal of class claims as a significant legal door left open. A refiled or restructured class action remains procedurally available if the reconsideration motion fails.

Bold Callout: The state-level parallel matter in the Florida Fourth District Court of Appeal (Docket No. 4D2023-1169, involving the same plaintiff by name) was affirmed on February 27, 2025, indicating the appellate record on these issues is already being built.

Bank of America Mortgage Records and RESPA Violations

RESPA Section 6 creates specific, enforceable obligations for mortgage servicers. When a borrower sends a qualified written request, the servicer must acknowledge receipt within five business days and provide a substantive response within 30 to 60 business days depending on the type of request.

The Warshaw complaint alleged conduct that, if proven, would represent textbook RESPA violations:

- Refusing to produce call recordings despite a lawful records request

- Backdating or falsely postmarking response letters to manufacture timely compliance

- Providing substantively inaccurate information about the servicer’s own deadlines

RESPA statutory damages for servicer violations are 2,000perviolation∗∗forindividualclaims.Inclassactions,thestatutecapsadditionalclassdamagesatthelesserof∗∗2,000perviolation∗∗forindividualclaims.Inclassactions,thestatutecapsadditionalclassdamagesatthelesserof∗∗1,000,000 or 1% of the servicer’s net worth, in addition to actual damages and attorney’s fees.

Attorneys handling these claims point to the false-postmark allegation as particularly significant: it transforms a procedural violation into a pattern of affirmative misrepresentation, which supports greater damages and makes class certification more defensible.

| RESPA Violation Type | Statutory Damages | Attorney’s Fees Available |

|---|---|---|

| Failure to respond to QWR | Up to $2,000 per violation | Yes |

| Failure to acknowledge within 5 days | Up to $2,000 per violation | Yes |

| Class action damages | Up to $1M or 1% net worth | Yes |

| Actual damages | No cap | Yes |

Litigation Watch: The Warshaw RESPA case was dismissed in February 2026 but class claims survived in procedural form. The pending reconsideration motion and the potential for a refiled class action keep this legal theory active. Any borrower who sent a formal records request to BofA and received a delayed or incomplete response between 2019 and 2025 should preserve all written communications with the bank.

Bank of America Mortgage Settlement 2026: What Exists and What Doesn’t

No open mortgage records settlement fund is currently accepting consumer claims from Bank of America borrowers as of June 2026.

The $12 million CFPB penalty paid under Docket No. 2023-CFPB-0016 went to the CFPB’s victims relief fund. That fund does not operate like a class action settlement where individual claimants submit a claim form and receive a check. The CFPB allocates those funds at its discretion.

The RESPA class action was dismissed before any settlement was negotiated. No settlement talks were publicly reported before the February 2026 dismissal. If the reconsideration motion succeeds or a new class action is filed, a settlement fund could eventually be established, but that has not occurred.

The escrow interest dispute in Cantero involves a legal determination about whether the bank owes interest, not a damages settlement. If the Supreme Court accepts the new certiorari petition and ultimately rules for borrowers, affected New York mortgage holders could become entitled to the statutory 2% interest they were never paid.

Attorneys handling these claims point to the difference between a regulatory penalty and a private right of recovery: borrowers should not assume that the $12 million penalty translates into money they can claim.

What Does and Does Not Exist in 2026

| Matter | Open Claims Portal | Consumer Access |

|---|---|---|

| CFPB HMDA penalty ($12M) | No | CFPB victims fund, not consumer claims |

| RESPA class action (Warshaw) | No | Dismissed; reconsideration pending |

| Escrow interest (Cantero) | No | Appellate ruling pending SCOTUS review |

| Infosys McCamish data breach | Claims period closed December 2025 | Payouts expected 2026 |

Cantero v. Bank of America: The Escrow Interest Ruling

Cantero v. Bank of America, N.A. is the most consequential Bank of America mortgage case currently before the federal judiciary. The Supreme Court first addressed it in Case No. 22-529 on May 30, 2024, vacating a prior Second Circuit ruling and ordering a more careful analysis.

On May 5, 2026, the Second Circuit, on remand, again ruled in favor of Bank of America in a 2-1 decision. The court held that New York General Obligations Law Section 5-601, which requires banks to pay at least 2% annual interest on mortgage escrow accounts, is preempted by the National Bank Act as applied to national banks.

The majority concluded that requiring interest payments on escrow funds interferes with a national bank’s ability to efficiently make real estate loans. The dissent disagreed, arguing the New York law does not significantly interfere with federal banking powers.

Attorneys handling these claims point to the circuit split as the strongest argument for another Supreme Court grant. The First Circuit ruled in 2025 in Conti v. Citizens Bank that similar state escrow laws are not preempted, creating direct conflict between circuits on the same legal question.

Circuit Split on Escrow Interest

| Circuit | Case | Ruling |

|---|---|---|

| Second Circuit | Cantero v. Bank of America (May 5, 2026) | State escrow law preempted |

| First Circuit | Conti v. Citizens Bank, N.A. (2025) | State escrow law not preempted |

| Ninth Circuit | Pending | Not yet resolved |

Bank of America Mortgage Data Breach Lawsuit

A separate line of litigation targets Bank of America’s third-party vendor relationships. In early 2025, investigators reported that a third-party provider breach exposed sensitive mortgage customer information, including names, addresses, Social Security numbers, and loan numbers.

This breach is distinct from the Infosys McCamish Systems data breach of 2023, which involved a different BofA vendor and resulted in a $17.5 million class action settlement. The Infosys McCamish claims period closed in December 2025, with payouts expected during 2026.

The 2025 third-party mortgage data breach generated attorney investigations, but no confirmed class action had been filed under a public docket number as of June 2026. The applicable legal theories would include negligence, breach of contract, and potentially state data protection statutes depending on where affected borrowers reside.

Attorneys handling these claims point to the importance of breach notification letters as the trigger document: if a borrower received a notification letter dated in 2025 regarding mortgage data exposure at Bank of America or a BofA vendor, that letter establishes standing and starts the statute of limitations clock.

BofA Data Breach Litigation Status

| Breach | Vendor | Settlement Status | Claims Deadline |

|---|---|---|---|

| 2023 Infosys McCamish | Infosys McCamish Systems | $17.5M settlement | Closed Dec. 2025 |

| 2025 third-party incident | Not publicly identified | Under investigation | TBD |

Litigation Watch: The Infosys McCamish $17.5 million settlement claims window closed in December 2025. Borrowers who did not file a claim before that deadline cannot recover from that fund. The 2025 third-party mortgage breach investigation remains at an early stage, with no public docket or settlement announced.

Bank of America Mortgage Borrower Rights in 2026

Federal law gives residential mortgage borrowers specific, enforceable rights that Bank of America is legally required to honor. These rights exist regardless of whether a lawsuit is pending.

Under RESPA Section 6:

- The right to send a qualified written request demanding account information, payment histories, and call recordings

- The right to receive an acknowledgment within five business days

- The right to a substantive response within 30 to 60 business days

- The right to actual damages, statutory damages of up to $2,000, and attorney’s fees if the servicer fails to comply

Under HMDA / Regulation C:

- The right to have demographic application data collected accurately and reported truthfully to the federal HMDA database

- No private right of action under HMDA itself, but falsified records may support ECOA claims

Under the Fair Credit Reporting Act:

- The right to dispute inaccurate mortgage account information reported to credit bureaus

- The right to require both the credit bureau and the furnisher (BofA) to investigate and correct errors

Attorneys handling these claims point to a QWR as the single most important document a mortgage borrower can generate: it starts the compliance clock, creates a paper record of the request, and, if ignored or mishandled, becomes Exhibit A in a RESPA claim.

How to File a Complaint Against Bank of America Mortgage

Borrowers who believe their rights under RESPA, HMDA, or state mortgage law have been violated have formal channels for registering complaints and preserving legal claims.

Step 1: Written Notice to the Servicer Send a qualified written request to Bank of America’s designated address for QWRs. Send it via certified mail with return receipt. Keep a copy of the letter and the postal receipt. The five-business-day acknowledgment clock starts from the date of receipt, not the date of sending.

Step 2: File a CFPB Complaint The Consumer Financial Protection Bureau accepts mortgage complaints at consumerfinance.gov. The CFPB forwards the complaint to the bank, which must respond within 60 days. CFPB complaint records are public and can support future litigation.

Step 3: Preserve All Documentation Document every phone call with the bank: date, time, name of representative, and what was said. Keep every letter, email, and statement. If the bank sends a response with a postmark that appears inconsistent with internal references to dates in the letter, preserve that envelope.

Step 4: Consult an Attorney RESPA, ECOA, and FCRA claims carry statutes of limitations ranging from one to three years depending on the claim. Waiting to consult an attorney risks losing the ability to file.

Attorneys handling these claims point to the certified mail record as the most frequently overlooked piece of evidence: it establishes when the bank received a request and anchors the compliance deadline.

State-by-State Impact of the Bank of America Mortgage Lawsuit

The Cantero escrow interest ruling affects borrowers differently depending on their state of residence. The geographic dimension of this litigation is one of the most underreported aspects of the broader BofA mortgage legal picture.

New York: Directly affected by the May 5, 2026 Second Circuit ruling. New York’s 2% escrow interest requirement was held preempted. New York borrowers with BofA mortgages who did not receive escrow interest cannot yet recover unless the Supreme Court reverses on the pending certiorari petition.

States in the First Circuit (Maine, Massachusetts, New Hampshire, Rhode Island, Puerto Rico): The First Circuit’s 2025 ruling in Conti v. Citizens Bank holds that similar state escrow interest laws are not preempted. BofA borrowers in those states whose state law includes an escrow interest requirement may be in a stronger legal position pending further appellate resolution.

Florida: The RESPA class action (Warshaw, Case No. 0:25-cv-60136) was filed in the Southern District of Florida. The February 2026 dismissal applies to that case. RESPA itself is a federal statute, so borrowers in any state can bring RESPA claims in federal court.

Attorneys handling these claims point to the circuit split as a reason why borrowers in different states should get individualized counsel rather than assuming a national class action will cover their situation.

| State/Region | Relevant Case | Borrower Status |

|---|---|---|

| New York | Cantero v. BofA | Escrow interest claim blocked (2d Cir.) unless SCOTUS reverses |

| First Circuit states | Conti v. Citizens Bank | Potentially stronger escrow interest position |

| Florida | Warshaw v. BofA | RESPA class dismissed; reconsideration pending |

| All states | HMDA enforcement | No direct consumer recovery from $12M CFPB penalty |

Litigation Watch: The circuit split between the Second Circuit’s May 2026 ruling in Cantero and the First Circuit’s 2025 ruling in Conti creates a direct conflict that the Supreme Court will be asked to resolve. That outcome will determine whether millions of borrowers in escrow-interest states are owed money that BofA has never paid.

What Attorneys Handle Bank of America Mortgage Claims

Not all plaintiff’s attorneys are equipped to handle every type of BofA mortgage claim. The case type determines the practice area, the applicable statute, and the damages structure.

Consumer Protection Attorneys handle RESPA Section 6 claims involving qualified written requests, notice of error violations, and servicer misconduct. They are experienced in the document-intensive nature of RESPA litigation and know how to structure class certification arguments around common practices.

Fair Lending and Civil Rights Attorneys are the appropriate counsel for borrowers who believe the HMDA false-entry problem was accompanied by discriminatory treatment, such as a denial or adverse loan terms tied to race or ethnicity. ECOA claims and fair housing claims require counsel with regulatory agency experience.

Class Action Attorneys with financial institution experience handle the broader class certification issues in cases like Warshaw. After a dismissal and reconsideration cycle, the attorney’s ability to restructure the class definition becomes critical to whether the case moves forward.

Data Privacy Attorneys handle breach notification claims arising from the Infosys McCamish incident and the 2025 third-party vendor breach. These claims involve state data protection statutes, negligence theories, and potentially state consumer protection laws.

Attorneys handling these claims point to fee-shifting statutes: RESPA, ECOA, and FCRA all provide for attorney’s fees to prevailing plaintiffs, which means a borrower with a strong case may not need to pay hourly legal fees out of pocket.

| Claim Type | Attorney Type | Fee Structure |

|---|---|---|

| RESPA record-request violation | Consumer protection attorney | Fees shifted to defendant if successful |

| HMDA / ECOA fair lending | Civil rights / fair lending attorney | Fees shifted; regulatory complaint route also available |

| Class action RESPA | Class action attorney | Contingency / fee-shifting |

| Data breach claim | Data privacy attorney | Contingency |

Bank of America Mortgage Lawsuit Timeline: From 2016 to 2026

The history of these proceedings spans a decade of alleged mortgage record failures. Viewing the cases in sequence reveals a pattern that regulators and plaintiff’s attorneys have both documented.

2016 to 2021: Bank of America loan officers falsely record mortgage applicants as having declined to provide demographic data required by HMDA, rather than asking the required questions. This practice spans “at least four years” according to the CFPB’s findings.

November 28, 2023: CFPB issues consent order under Docket No. 2023-CFPB-0016. Bank of America ordered to pay $12 million and implement compliance reforms.

January 2025: Warshaw v. Bank of America (Case No. 0:25-cv-60136) filed in the U.S. District Court for the Southern District of Florida, alleging RESPA and Florida Consumer Collection Practices Act violations tied to the bank’s refusal to produce mortgage records.

May 30, 2024: The U.S. Supreme Court (Case No. 22-529) vacates the Second Circuit’s prior ruling in Cantero v. Bank of America and remands for a more careful preemption analysis.

June 5, 2025: CFPB terminates the 2023 consent order after confirming full compliance, including the $12 million payment.

February 9, 2026: Judge Rodney Smith dismisses Warshaw with prejudice as to the named plaintiff; class claims dismissed without prejudice.

March 2026: Plaintiff files motion for reconsideration in Warshaw.

May 5, 2026: Second Circuit rules 2-1 for Bank of America in Cantero, holding New York’s escrow interest statute preempted by the National Bank Act.

May 22, 2026: New petition for certiorari filed with the U.S. Supreme Court in Cantero, citing the circuit split with the First Circuit’s 2025 ruling.

Attorneys handling these claims point to the compressed 2026 timeline as unusual: two separate major rulings on BofA mortgage cases in the same three-month window signals a level of appellate activity that may produce a definitive Supreme Court ruling within the next term.

Frequently Asked Questions

Is there an active Bank of America mortgage settlement in 2026?

No open mortgage records settlement fund is accepting consumer claims as of June 2026. The CFPB’s $12 million penalty went to its internal victims relief fund. The Warshaw RESPA class action was dismissed before any settlement was negotiated, and the Cantero escrow case remains in the certiorari petition stage.

What is CFPB Docket No. 2023-CFPB-0016?

This is the formal docket number for the CFPB’s administrative enforcement action against Bank of America, issued on November 28, 2023. It documented that BofA loan officers falsely recorded mortgage applicants’ demographic data as “declined to state” for at least four years, covering 2016 to 2021. The order was terminated on June 5, 2025.

What happened to the Warshaw v. Bank of America RESPA lawsuit?

The case (No. 0:25-cv-60136, S.D. Fla.) was dismissed by Judge Rodney Smith on February 9, 2026. The named plaintiff’s claims were dismissed with prejudice. Class claims were dismissed without prejudice, leaving a procedural path for a refiled action. A motion for reconsideration was filed in March 2026.

What does the Cantero Second Circuit ruling mean for my mortgage?

If you hold a Bank of America mortgage in New York, the May 5, 2026 Second Circuit ruling means New York’s 2% escrow interest law is currently held to be preempted by federal law. That outcome may change if the Supreme Court grants the certiorari petition filed May 22, 2026 and reverses the Second Circuit. Borrowers in First Circuit states may be in a stronger position under that circuit’s contrary ruling.

Can I sue Bank of America for mortgage records that were falsified?

HMDA does not create a private right of action, so the false-demographic-data issue alone does not entitle a borrower to sue under HMDA. If the falsified records accompanied discriminatory treatment in the loan approval or pricing process, an Equal Credit Opportunity Act claim may be available. A consumer protection or fair lending attorney can assess which theory applies to a specific borrower’s facts.

What type of attorney should I contact about a Bank of America mortgage records claim?

The appropriate attorney depends on which legal theory applies to your situation. A consumer protection attorney handles RESPA record-request violations. A civil rights or fair lending attorney handles HMDA-related ECOA claims. A class action attorney with financial services experience is the right fit if a new class filing emerges from the Warshaw reconsideration process.

Closing

Three separate legal proceedings against Bank of America’s mortgage operations are at different stages in 2026. The CFPB’s $12 million HMDA enforcement action is closed but its findings remain on the public record. The RESPA class action remains procedurally alive through a pending reconsideration motion. The escrow interest dispute is heading toward a second Supreme Court review.

Borrowers who sent written record requests to BofA and received incomplete or misleading responses, or who held BofA mortgages during the 2016 to 2021 HMDA period, should document their records carefully and speak with a consumer protection or fair lending attorney. RESPA, ECOA, and FCRA all carry statutes of limitations. Timing matters.