Quick Answer

- Lawsuit funding is a cash advance against an expected settlement, not a traditional loan, repaid only if the case wins or settles.

- Plaintiffs in active personal injury, mass tort, or civil litigation generally qualify, provided their attorney confirms the case and cooperates with underwriting.

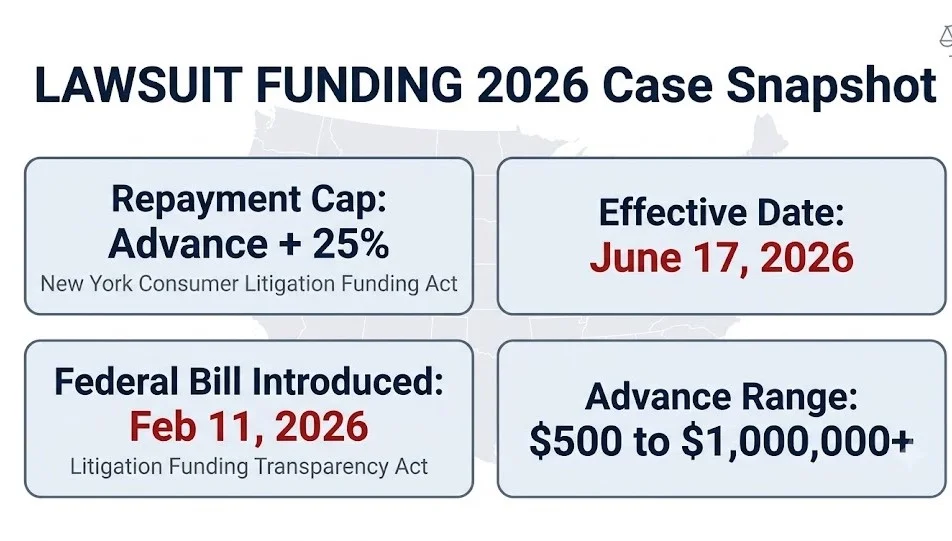

- Costs vary sharply by state. New York now caps total repayment at the advance plus 25% of gross recovery, while many states still have no cap at all.

Case Snapshot

| Detail | Info |

|---|---|

| Governing Law | State consumer legal funding statutes, plus pending federal disclosure bill |

| Key 2026 Statute | New York Consumer Litigation Funding Act |

| Effective Date | June 17, 2026 |

| Federal Bill | Litigation Funding Transparency Act, introduced February 11, 2026 |

| Status | State laws active and expanding; federal bill pending in Senate Judiciary Committee |

Lawsuit funding is now a multibillion-dollar industry operating mostly outside traditional lending law. That gap is closing fast in 2026. New York’s repayment cap takes effect this June, and a federal bill introduced by four senators would force disclosure of funding deals in mass torts and class actions nationwide.

For a plaintiff sitting on a slip-and-fall claim or a mass tort filing, the funding decision can determine how much of a settlement actually reaches their pocket. Rates and caps differ by state, sometimes by a factor of three or four. This piece breaks down what lawsuit funding actually is, what it costs, and which states are changing the rules in 2026.

Lawsuit Funding

Lawsuit funding is a cash advance paid to a plaintiff against the future proceeds of a pending legal claim. It is not a loan in the traditional sense. Repayment comes only out of a settlement or verdict, and most contracts are structured as non-recourse, meaning the plaintiff owes nothing if the case is lost.

The money typically covers rent, medical bills, or lost wages while a case drags through discovery or negotiation. Funding companies underwrite the advance based on the strength of the claim, not the plaintiff’s credit score or employment history.

Quick facts:

- No credit check or income verification required by most funders

- Funded within 24 to 48 hours of approval in many cases

- Advance amounts commonly range from $500 to several million dollars depending on case value

Attorneys handling these claims point to the non-recourse structure as the defining legal feature that separates funding from a conventional loan.

How Does Lawsuit Funding Work

How lawsuit funding works is straightforward at the surface and complicated underneath. A plaintiff applies, the funder contacts the plaintiff’s attorney to verify the case, and underwriters estimate the claim’s settlement value.

Once approved, funds typically arrive by direct deposit. Repayment is deducted from the settlement at the time the case resolves, handled directly between the funder and the law firm’s trust account.

The underwriting process looks at:

- Strength of liability evidence, including police reports and witness statements

- Severity of damages, including medical bills and lost income

- Defendant’s insurance coverage and ability to pay

- Estimated time to resolution

Attorneys handling these claims point to the verification step as the moment a poorly documented case gets flagged before funds change hands.

Litigation Watch: Funding decisions hinge almost entirely on case strength and projected settlement value, not the plaintiff’s personal finances.

Lawsuit Settlement Funding

Lawsuit settlement funding refers to advances issued against a case that already has a pending settlement or strong likelihood of resolution. It is functionally the same product as pre-settlement funding, just marketed under a different name by some companies.

This stage of funding often carries somewhat lower risk for the funder, since a settlement may already be under negotiation. That can translate to marginally better terms for the plaintiff, though this is not guaranteed.

| Funding Stage | Typical Risk Level | Plaintiff Leverage |

|---|---|---|

| Early litigation | Higher for funder | Lower, terms less favorable |

| Post-settlement offer | Lower for funder | Higher, may negotiate better rate |

| Post-verdict, pending appeal | Moderate | Depends on appeal timeline |

Attorneys handling these claims point to timing as the single biggest factor in negotiating favorable rates.

Lawsuit Funding Companies

Lawsuit funding companies are private finance firms that purchase a contingent interest in a plaintiff’s future settlement in exchange for upfront cash. Some operate as direct funders, lending their own capital, while others broker deals between plaintiffs and outside investors.

The industry is loosely organized around the American Legal Finance Association, a trade group some funders cite as a marker of ethical practice, though membership is voluntary and not a substitute for state licensing.

Key distinctions among funding companies:

- Direct funders provide capital themselves and tend to have more flexible terms

- Brokers add a markup to connect plaintiffs with third-party capital

- Mass tort funders specialize in large multi-plaintiff litigation, including pharmaceutical and product liability cases

Attorneys handling these claims point to broker markups as the least transparent cost in the entire funding process.

Who Qualifies For Lawsuit Funding

Who qualifies for lawsuit funding depends on case type and documentation, not personal credit. Plaintiffs with active personal injury, mass tort, product liability, employment, or whistleblower claims are the most common applicants.

Funders generally require that the plaintiff already has legal representation. The attorney’s cooperation in verifying case facts is treated as a near-mandatory step in underwriting.

Common qualifying case types:

- Car accident and other motor vehicle injury claims

- Premises liability and slip-and-fall cases

- Medical malpractice claims

- Product liability and mass tort litigation

- Workplace discrimination and employment disputes

- Qui tam whistleblower actions

Attorneys handling these claims point out that funders almost always decline cases with weak liability evidence, regardless of how badly a plaintiff needs the cash.

Lawsuit Funding Interest Rates

Lawsuit funding interest rates are not capped nationally and vary enormously by company and state. Because funding is not classified as a loan in many jurisdictions, traditional usury caps frequently do not apply.

Some contracts charge simple interest. Others compound monthly, which can roughly double the amount owed within two to three years if a case drags on.

| Rate Structure | Risk to Plaintiff |

|---|---|

| Simple, non-compounding | Lower total cost over time |

| Compounding monthly | Cost can balloon on long cases |

| Capped repayment (e.g. New York’s 25% cap) | Predictable, limited cost |

Bold callout: A $10,000 advance under a compounding structure can exceed $20,000 owed within roughly three years, depending on the contract terms.

Attorneys handling these claims point to compounding interest as the clause most likely to surprise a plaintiff at settlement time.

Lawsuit Funding Regulations By State

Lawsuit funding regulations by state range from strict caps to almost no oversight at all. Because funding has historically avoided classification as a consumer loan, most states regulate it separately, if they regulate it at all.

New York’s new statute is the most aggressive consumer protection law in the country as of 2026. Florida, Oklahoma, Ohio, and Missouri have also passed targeted consumer legal funding statutes in recent years, each with different disclosure and registration requirements.

| State | 2026 Status |

|---|---|

| New York | Consumer Litigation Funding Act caps repayment at advance plus 25% of recovery, effective June 17, 2026 |

| Florida | SB 1396 imposes disclosure and licensing requirements on funders |

| Missouri | Regulates consumer legal funding directly; commercial funding remains unregulated |

| Most other states | No dedicated funding statute; usury exemptions often apply |

Attorneys handling these claims point to the state-by-state patchwork as the reason two plaintiffs with identical cases can owe wildly different amounts depending on where they live.

Litigation Watch: A plaintiff’s home state, not just their case type, can determine whether their funding contract is capped or effectively open-ended.

Lawsuit Funding Laws 2026

Lawsuit funding laws in 2026 are shifting toward federal disclosure requirements layered on top of existing state statutes. The most significant development is the Litigation Funding Transparency Act, introduced in the Senate on February 11, 2026 by Judiciary Committee Chairman Chuck Grassley along with Senators Thom Tillis, John Kennedy, and John Cornyn.

The bill would require disclosure of third-party funding, including foreign funding, in mass tort and class action cases. It would also bar funders from influencing litigation strategy or accessing protected discovery material.

Key provisions of the federal bill:

- Mandatory disclosure when a funder is a commercial enterprise, foreign state, or sovereign wealth fund

- Exemption for nonprofit legal organizations and standard loan-style fee arrangements

- Prohibition on funders directing settlement decisions

- Endorsed by the U.S. Chamber of Commerce and the American Property Casualty Insurance Association

The bill also prohibits any third-party funder from influencing litigation strategy or settlement negotiations, as well as obtaining, inspecting, copying, or viewing material produced in discovery that is subject to a protective order.

Separately, individual federal judges have begun issuing standing orders requiring parties to disclose outside funder involvement in their courtrooms, even without a statute requiring it.

Attorneys handling these claims point to these judicial standing orders as a sign that disclosure may arrive case by case before Congress acts at all.

Lawsuit Funding Vs Lawsuit Loan

Lawsuit funding and a lawsuit loan are often used interchangeably, but the legal distinction matters. True funding is structured as a non-recourse purchase of a stake in future proceeds. A loan implies a debt obligation that exists regardless of case outcome.

Some companies market themselves with “loan” in the name while still operating on a non-recourse basis. The contract language, not the marketing label, determines what a plaintiff actually owes if the case fails.

What to check in any contract:

- Does repayment depend on winning the case

- Is the obligation classified as a loan or an asset purchase

- Does the contract reference a specific state’s loan licensing law

Attorneys handling these claims point to the recourse clause as the single sentence that matters most in any funding agreement.

Pre-Settlement Funding

Pre-settlement funding is the formal industry term for an advance issued before a case has settled or gone to verdict. It is the most common form of lawsuit funding and the term most often used in funder marketing.

Because the case outcome is still uncertain at this stage, funders typically charge higher rates than they would for funding issued after a settlement is already on the table.

Quick facts:

- Most common case types: personal injury, medical malpractice, wrongful death

- Approval often does not require employment verification

- Attorney cooperation in underwriting is standard practice

Attorneys handling these claims point to early-stage funding as carrying the highest cost relative to case value, simply because risk to the funder is highest at that point.

Lawsuit Funding News

Lawsuit funding news in 2026 has centered on two competing pressures: industry growth and regulatory pushback. Commercial litigation funding, distinct from consumer advances, has expanded into financing entire law firm caseloads in exchange for a share of proceeds, drawing scrutiny over outside control of litigation strategy.

Once discussed primarily in the context of consumer advances to individual plaintiffs, the funding landscape now includes a growing commercial sector in which third parties finance lawsuits brought by law firms or business entities in exchange for a share of the proceeds. That expansion has fueled congressional interest in disclosure rules.

Foreign funding has also drawn national security concerns. A 2024 Bloomberg Law investigation, cited repeatedly in 2026 policy debates, found that a subsidiary tied to a Russian conglomerate had backed lawsuits in the United States and the United Kingdom, with no disclosure requirement forcing that involvement into public view at the time.

Notable 2026 developments:

- Federal Litigation Funding Transparency Act introduced February 2026

- New York’s consumer funding cap law set to take effect June 2026

- Multiple federal judges issuing individual standing orders on funder disclosure

- Continued state-level divide between populist and establishment Republicans over regulation approach

Attorneys handling these claims point to the bipartisan, and intra-party, disagreement over regulation as a sign this issue is far from settled.

Litigation Watch: The funding industry’s biggest 2026 fight is not about consumer rates at all. It is about who controls litigation strategy when outside capital is involved.

Lawsuit Funding Near Me

Lawsuit funding near me searches usually reflect a desire for a company licensed and compliant in the searcher’s own state, since funding terms differ sharply by jurisdiction. A company licensed in New York operates under different repayment caps than one based in a state with no funding statute at all.

Plaintiffs should confirm a funder’s registration status in their state before applying, rather than assuming a company that funds nationally follows the same terms everywhere.

What to verify locally:

- Whether the state has a consumer legal funding statute

- Whether the funder is registered or licensed in that state

- Whether the state imposes a repayment cap or interest rate ceiling

Attorneys handling these claims point out that a national funder’s website often understates how much terms shift from state to state.

Is Lawsuit Funding Worth It

Whether lawsuit funding is worth it depends on the size of the advance relative to the eventual settlement, and on how long the case takes to resolve. A small advance against a strong six-figure case carries far less risk than a large advance against an uncertain claim.

The core trade-off is straightforward. Funding can prevent a plaintiff from accepting a lowball settlement out of financial desperation, but it also reduces the net amount that plaintiff ultimately keeps.

Factors that affect whether funding makes sense:

- Size of the advance compared to expected settlement

- Whether the contract has a repayment cap

- How long the case is realistically expected to take

- Whether other lower-cost options, like a personal loan, are available

Attorneys handling these claims point to undercapitalized small advances, taken only to cover a few months of bills, as generally the lowest-risk use of this product.

How To Apply For Lawsuit Funding

Applying for lawsuit funding starts with contacting a funding company directly or through a referral, followed by the funder reaching out to the plaintiff’s attorney. The attorney’s involvement is not optional in practice, even though it is not always a strict legal requirement.

Approval timelines are often fast. Many companies advertise funding decisions and disbursement within 24 to 48 hours of underwriting completion.

Typical application steps:

- Submit basic case and contact information

- Funder contacts the plaintiff’s attorney for case verification

- Underwriters review liability evidence and estimated case value

- Plaintiff reviews and signs the funding contract

- Funds are disbursed, often by direct deposit

Attorneys handling these claims point to the contract review step as the stage where a plaintiff should slow down, even when the funder is pushing for a quick signature.

Frequently Asked Questions

What is lawsuit funding and how does it work?

Lawsuit funding is a cash advance issued against the expected proceeds of a pending legal claim.

It is repaid out of the settlement, and most contracts are non-recourse, meaning nothing is owed if the case is lost.

Is lawsuit funding considered a loan?

In most states, lawsuit funding is not classified as a traditional loan.

It is typically structured as a non-recourse purchase of a future interest in the case, which is why most state usury laws historically have not applied to it.

How much does lawsuit funding cost?

Cost depends heavily on the state, the contract terms, and whether interest compounds.

In states like New York, total repayment is now capped at the advance plus 25% of gross recovery, while many other states have no such cap.

Do I need my lawyer’s approval to get lawsuit funding?

Most funders require contact with the plaintiff’s attorney as part of underwriting.

While not always a strict legal requirement, attorney involvement is standard practice and protects the plaintiff from signing unfavorable terms.

What happens to lawsuit funding if I lose my case?

Under a non-recourse contract, the plaintiff owes nothing if the case is lost.

This is the central protection that separates lawsuit funding from a conventional personal loan.

Is lawsuit funding regulated in every state?

No, regulation varies significantly by state as of 2026.

States like New York, Florida, Missouri, and Oklahoma have specific consumer legal funding statutes, while many others have no dedicated law governing the practice.

Closing

Lawsuit funding can buy time during a long case, but the cost depends entirely on where a plaintiff lives and what the contract actually says. New York’s new cap and the pending federal disclosure bill are reshaping that picture in real time.

Before signing anything, a plaintiff’s own attorney should review the contract terms. This is the moment a personal injury or mass tort lawyer earns their role in the process.