Quick Answer: National Life Group has faced two major legal battles: a class action pyramid scheme lawsuit involving its subsidiary Life Insurance Company of the Southwest and marketing partner Premier Financial Alliance, which reached a $50 million settlement (fully approved and paid out as of late 2024); and a separate, still-active IUL (Indexed Universal Life) lawsuit filed in October 2024 alleging misleading policy illustrations. If you were a PFA associate who bought a Living Life policy in California between 2014 and 2023, payments have already been distributed. If you hold a National Life IUL policy and believe you were misled, you may still have legal options. Lawsuit in Spanish

This guide covers both cases, what they mean for current and former policyholders, and what steps you can take right now.

What Is the National Life Group Lawsuit About?

“National Life Group lawsuit” is actually a term that covers two distinct legal battles — and it’s important to understand which one applies to you.

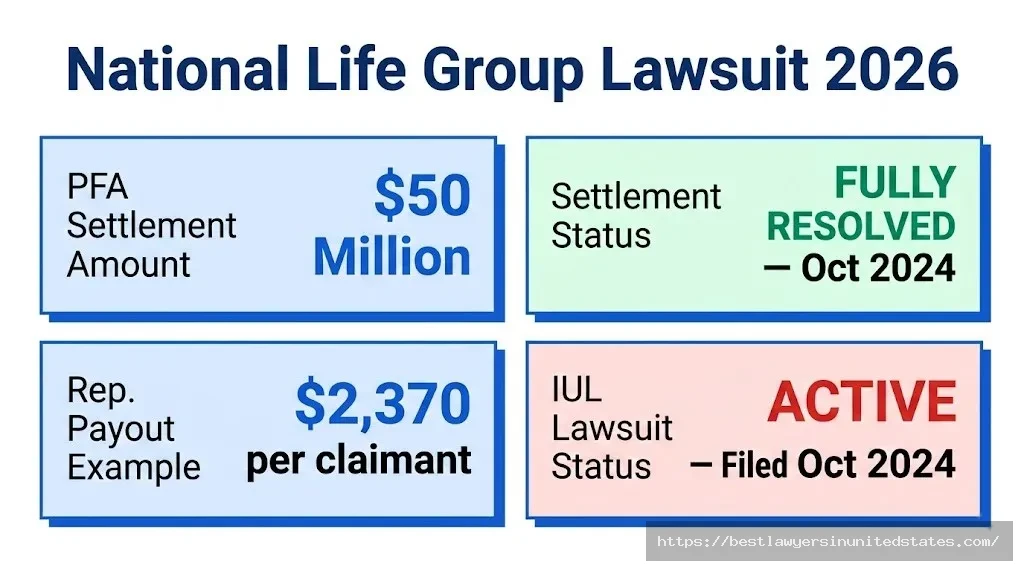

The first is the PFA Pyramid Scheme Class Action, a major class action filed in 2018 alleging that National Life’s subsidiary Life Insurance Company of the Southwest, along with marketing partner Premier Financial Alliance (PFA), ran an illegal pyramid scheme targeting Chinese, Vietnamese, and Filipino immigrants. That case settled for up to $50 million and received final court approval on February 5, 2024. Payments were distributed to eligible class members in October 2024.

The second is the IUL Illustrations Lawsuit, filed in October 2024 by an Indiana policyholder who says National Life’s Indexed Universal Life policy returned 0% interest despite market gains — a result she calls “a fraudulent sham.” This case is still active as of early 2026, with an amended complaint adding state-level claims.

If you’re wondering which case affects you, use this quick guide:

- Were you a PFA associate who bought a Living Life IUL policy in California between 2014–2023? → The pyramid scheme settlement affects you. Payments have been distributed.

- Do you hold a National Life IUL policy and feel the returns were misrepresented? → The ongoing IUL lawsuit may be relevant to your situation.

- Are you a general National Life policyholder with claim delays or denials? → This guide covers your options too.

Here’s a quick-reference overview of both lawsuits:

Table 1: National Life Group Lawsuit — Quick Reference Overview

| Detail | PFA Pyramid Scheme Case | IUL Illustrations Case |

|---|---|---|

| Case Name | In re PFA Insurance Marketing Litigation | Virani v. NLV Financial Corporation et al. |

| Case Number | 4:18-cv-03771-YGR (N.D. Cal.) | Filed Oct. 31, 2024 (D. Vt.) |

| Filed | June 2018 | October 31, 2024 |

| Defendants | PFA, Life Insurance Co. of the Southwest, National Life Insurance Co. | NLV Financial Corp., National Life Insurance Co., Life Insurance Co. of the Southwest |

| Key Allegations | Pyramid scheme targeting immigrants | Misleading IUL illustrations, 0% returns, RICO violations |

| Settlement Amount | Up to $50 million | No settlement — still active |

| Final Status | Fully resolved; payments distributed Oct. 2024 | Active litigation as of 2026 |

| Who It Affects | CA-based PFA associates who bought Living Life policies 2014–2023 | IUL policyholders nationwide |

Case #1: The PFA Pyramid Scheme Lawsuit — Full History

Background of the Lawsuit

This case started with a core allegation: that National Life’s marketing partner Premier Financial Alliance wasn’t really selling insurance — it was recruiting people to recruit more people. The defendants are accused of exploiting trust within tight-knit immigrant communities, specifically targeting Chinese, Vietnamese, and Filipino Americans with promises of financial independence and entrepreneurial success.

The scheme allegedly worked like this: recruits paid a $125 membership fee, purchased an expensive Living Life Indexed Universal Life Insurance policy, and then pressured their friends and family to do the same. The policy itself was significantly more expensive than comparable National Life products sold outside the PFA network — which meant the only way to “sell” it was to recruit more associates, not find genuine customers.

According to the complaint, 95% or more of PFA sales came from affiliates purchasing policies themselves, and over 95% of PFA associates averaged net losses rather than profit. One PFA training presentation allegedly made it explicit: “Recruiting is the game.”

Timeline of Key Events

| Date | Event | Details |

|---|---|---|

| June 2018 | Original class action filed | N.D. California; alleged “classic pyramid scheme” |

| February 2019 | Second lawsuit filed | New plaintiffs; added targeting of Asian immigrants |

| May 2019 | Claims against NLV/National Life dismissed | Dismissed for lack of personal jurisdiction |

| April 2020 | Cases consolidated | In re PFA Insurance Marketing Litigation, No. 4:18-cv-03771 |

| November 2021 | Class certification granted | Court certified the class |

| March 17, 2023 | $50 million settlement reached | Settlement stipulation filed with court |

| July 21, 2023 | Preliminary approval granted | U.S. District Court, N.D. California |

| January 16–23, 2024 | Fairness Hearing held | Court reviewed settlement terms |

| February 5, 2024 | Final approval granted | Judge Yvonne Gonzalez Rogers signed off |

| August 21, 2024 | Ninth Circuit upholds settlement | Appeal denied; settlement confirmed |

| October 23, 2024 | Payments distributed | Class members received checks/direct deposits |

Who Filed the Lawsuit?

The original 2018 case was filed by two plaintiffs who had enrolled as PFA associates and felt trapped in a scheme. A second lawsuit was filed in February 2019 with additional plaintiffs, including Wang and Chen, both New Jersey residents. The cases were consolidated in April 2020 under lead plaintiff Dalton Chen. dailynewslaw

Class Counsel — the attorneys representing the class — pursued the case in the U.S. District Court for the Northern District of California before Judge Yvonne Gonzalez Rogers. The defendants named include Premier Financial Alliance, Inc., Life Insurance Company of the Southwest (a National Life Group subsidiary), and various high-level PFA executives and promoters.

What Are the Allegations?

The lawsuit alleged multiple violations of California law, including the California Unfair Competition Law and California’s Endless Chain Law (which prohibits pyramid schemes).

Key allegations against the defendants:

- ✅ Operating an illegal pyramid scheme — Revenue generated primarily through chain recruitment of associates, not genuine insurance sales

- ✅ Targeting vulnerable immigrant communities — Specifically exploiting trust within Chinese, Vietnamese, and Filipino communities through affinity fraud

- ✅ Misleading income representations — Promising recruits they could “earn millions” and achieve financial independence

- ✅ Overpriced, captive products — Selling Living Life IUL policies at inflated prices that could only realistically be sold within the pyramid

- ✅ Failure to disclose — Not telling recruits that money flowed upward to those at the top of the chain, not to new associates

- ✅ False projection of premium costs — Providing inaccurate or misleading projections about future premium payments

Who Qualified for the PFA Settlement?

Quick Answer: If you enrolled as a PFA associate and purchased a Living Life or Living Life by Design IUL policy in California between January 1, 2014, and March 17, 2023, you were a class member. Payments were distributed in October 2024. If you haven’t received payment and believe you were eligible, contact the claims administrator.

Eligibility Requirements (PFA Settlement — Now Closed)

| Requirement | Details | What Was Needed |

|---|---|---|

| PFA Enrollment | Must have enrolled as a PFA associate | PFA membership records |

| Policy Purchase | Purchased Living Life or Living Life by Design policy | Policy documents |

| Location | Policy purchased in California | State of purchase documentation |

| Date Range | Between January 1, 2014 and March 17, 2023 | Policy issue date |

| Policy Type | LICS-issued Living Life IUL policies only | Policy number |

Who Was NOT Eligible?

You were not covered by the PFA settlement if:

- ❌ You purchased a Living Life policy outside of California

- ❌ You enrolled with PFA but never purchased a qualifying policy

- ❌ You were a judicial officer assigned to the case

- ❌ You reached high leadership levels within PFA (Senior Executive Field Director and above were excluded from certain relief)

- ❌ You opted out of the class during the exclusion period

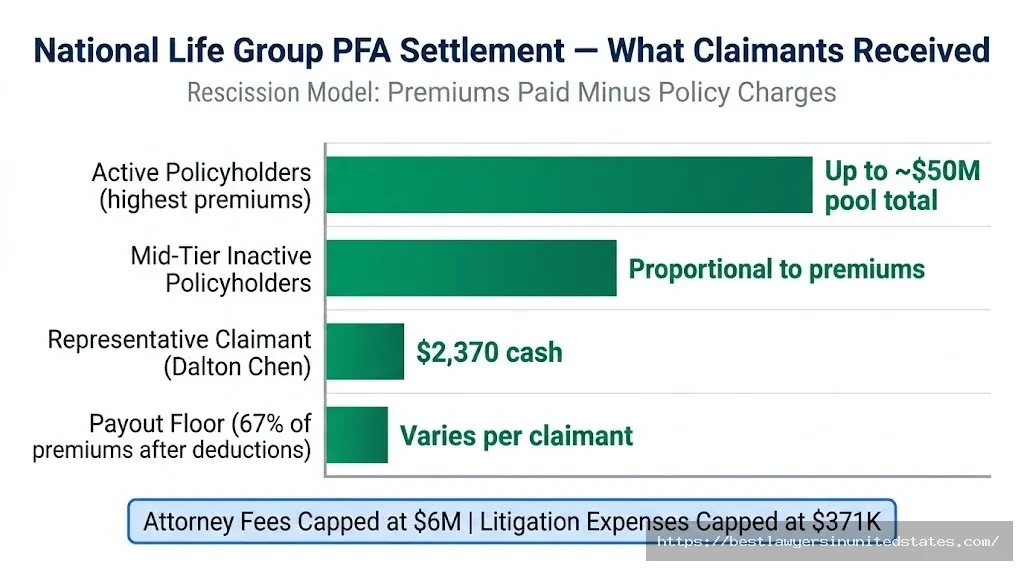

How Much Money Did the PFA Settlement Pay Out?

Quick Answer: The settlement ceiling was approximately $50 million over and above cash surrender values. Individual payouts depended on premiums paid and whether the policy was still active. The lead plaintiff Dalton Chen’s claim of $2,370 was cited as a representative example for inactive policyholders.

Settlement Fund Breakdown

| Category | Amount | Purpose |

|---|---|---|

| Total Settlement Ceiling | Up to ~$50 million | Total available above cash surrender values |

| Attorney Fees | Up to $6,000,000 | Class counsel legal fees |

| Litigation Expenses | Up to $371,000 | Case administration costs |

| Class Representative Awards | $10,000 per named plaintiff | Additional compensation for lead plaintiffs |

| Net Available to Class Members | Remaining balance | Distributed proportionally based on premiums paid |

How Individual Payouts Were Calculated

The settlement used a rescission-based model — meaning it aimed to put class members back in the position they’d be in if they had never bought the policy.

For inactive policyholders (policies already lapsed or surrendered), relief was calculated as premiums paid minus policy charges, overhead, and the value of any life insurance coverage you received.

For active policyholders, relief included the termination of their policy and a cash payment calculated under the same model.

Representative example: Lead plaintiff Dalton Chen, as an inactive policyholder, received $2,370 — equaling roughly 67% of his total premiums paid after subtracting policy charges and overhead. Chris Brown Lawsuit 2026

Comparison with Similar IUL/Insurance Lawsuits

| Lawsuit | Settlement Amount | Affected Parties | Payout Range | Status |

|---|---|---|---|---|

| PFA / National Life (THIS CASE) | ~$50 million | CA-based PFA associates | Varies by premiums paid | Fully resolved, Oct. 2024 |

| Transamerica Universal Life | $195 million | ~70,000 policyholders | Credits or cash | Resolved |

| US Financial Life Insurance | $28 million | ~12,000 policyholders | Proportional | Resolved |

| Pacific Life IUL (jury verdict) | $1.5 million | 1 retiree | Full damages | Resolved May 2024 |

Case #2: The Active IUL Illustrations Lawsuit (2024–Present)

This is the lawsuit that’s still playing out — and if you hold a National Life IUL policy that hasn’t performed as sold, it’s worth paying close attention.

Background: The Virani Case

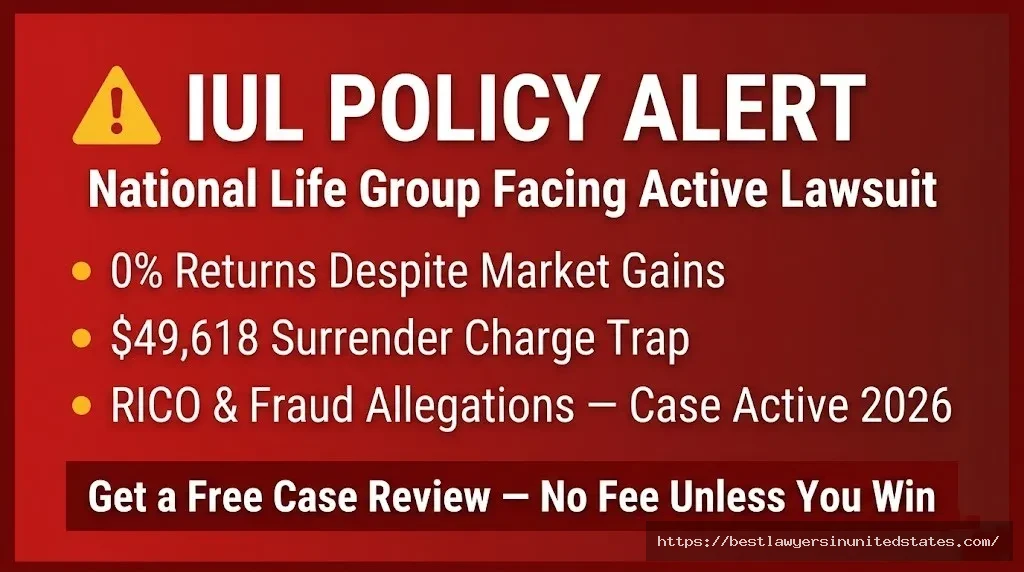

In October 2024, Indiana resident Sanya Virani sued NLV Financial Corporation and two of its subsidiaries — National Life Insurance Co. and Life Insurance Company of the Southwest — in the U.S. District Court for the District of Vermont, where National Life is headquartered.

Virani purchased an IUL policy on September 8, 2023, with a face coverage amount of $2,767,336. She allocated 100% of her accumulated value to the “US Pacesetter No Cap Annual Point-to-Point Indexed Strategy.” After one full year, her policy earned 0% interest — despite the market index posting gains during that period.

She also faces a surrender charge of $49,618.33 if she tries to exit the policy.

Virani’s complaint calls the IUL “a fraudulent sham” that relies on back-tested historical data that doesn’t reflect actual policy performance. She argues that the illustrations she was shown were designed to look impressive on paper but were structurally incapable of delivering those results.

Key Allegations in the IUL Case

- ✅ Misleading performance illustrations — IUL projections relied on back-tested index data, not realistic forward-looking returns

- ✅ Breach of contract — Policy performance did not match representations made at sale

- ✅ RICO violations — Complaint alleges a pattern of mail and wire fraud in marketing IUL products

- ✅ Inadequate fee disclosure — Internal fees, cost of insurance charges, and other deductions allegedly not clearly communicated

- ✅ 0% interest despite market gains — The US Pacesetter Index credited nothing for the September 2023–September 2024 period

- ✅ Costly exit traps — Surrender fees prevent policyholders from leaving without significant financial loss

Timeline of the IUL Case

| Date | Event | Details |

|---|---|---|

| October 31, 2024 | Original complaint filed | U.S. District Court, D. Vermont |

| January 2025 | NLV files motion to dismiss | Argues IUL illustrations are “heavily regulated” and not a contract |

| June 2025 | Amended complaint filed | State-level claims added to federal allegations |

| September 2025 | Partial dismissal granted | Vermont judge dismissed two National Life entities; case continues against remaining defendants |

| 2026 | Case ongoing | Active litigation; no settlement announced |

National Life’s spokesperson has stated consistently: “We strongly dispute the plaintiff’s allegations, and we intend to vigorously contest them.”

How the US Pacesetter Index Works — And Why It’s Controversial

The US Pacesetter Index is a proprietary index launched by National Life in December 2021. It tracks multiple asset classes and U.S. equity markets, and uses volatility-reduction mechanisms to produce a smoother return profile.

The problem, critics say, is that National Life’s IUL illustrations used back-tested historical performance of the index — meaning they showed hypothetical returns based on how the index would have performed in the past, not how it actually performed after launch. The index returned 0% for the Virani policy year, despite real-world equity market gains during that period.

This is a broader issue across the IUL industry. Multiple insurance carriers — including Allianz, Minnesota Life, Transamerica, Pacific Life, and Prudential — face similar litigation. Regulators, including the Department of Financial Services (DFS), have warned consumers about universal life insurance illustrations that may not reflect achievable returns. techlawnews

What National Life IUL Policyholders Should Know Right Now

If you hold a National Life IUL policy and feel the returns don’t match what you were shown during the sales process, here’s what to do:

Step 1: Pull your Annual Statement Your Annual Statement shows exactly how much interest was credited to your policy for the year. If the amount was 0% or far below what illustrations projected, document this.

Step 2: Find your original policy illustrations The illustrations shown to you at purchase are the benchmarks for any misrepresentation claim. Locate the original projections and compare them to actual performance.

Step 3: Calculate any surrender charges Your policy documents list the surrender charge schedule. These charges are often substantial in the early policy years and represent real financial harm if you want to exit.

Step 4: Document all fees Request a full fee disclosure from National Life. IUL policies can carry internal fees that reduce your effective returns significantly — sometimes exceeding 8% on premiums and cash values.

Step 5: Contact an IUL litigation attorney Firms like RP Legal LLC have handled over 400 IUL cases and recovered over $100 million for clients. Many offer free initial consultations on a no-recovery-no-fee basis.

Filing Process at a Glance

| Step | Action | Notes |

|---|---|---|

| 1 | Gather annual statements and illustrations | Compare projected vs. actual returns |

| 2 | Document all fees paid | Request full fee disclosure from National Life |

| 3 | Note surrender charges | These quantify your exit costs |

| 4 | Contact an IUL attorney | Free consultations available |

| 5 | Attorney reviews your claim | Assesses viability, files if warranted |

| 6 | Arbitration or litigation | Most IUL disputes go through arbitration |

Do You Need a Lawyer?

Quick Answer: For the PFA settlement, the filing period is closed and no attorney is needed at this stage. For the IUL lawsuit, you don’t need a lawyer to raise a complaint, but legal representation significantly improves your chances of recovery — and most IUL attorneys work on a contingency basis, meaning no upfront cost.

Filing Without a Lawyer

If you were a PFA class member and didn’t receive payment, your first step is to contact the settlement administrator directly at the official settlement website (pfasettlement.com) or reach out to class counsel.

For IUL policyholders pursuing a separate claim, you can file a complaint with your state’s Department of Insurance without an attorney. The DFS and similar regulators take IUL complaints seriously, and a formal complaint can trigger a regulatory investigation.

When Legal Help Makes Sense

Consider consulting an attorney if:

- Your policy has returned significantly less than illustrated projections

- You’re locked into a policy with high surrender charges and can’t afford to exit

- You were sold the policy through a PFA-affiliated agent and feel you were misled

- Your claim is denied or delayed without clear explanation

- You experienced misrepresentation about tax advantages, guaranteed returns, or borrowing strategies

Free Legal Consultation Options

For IUL-related claims, RP Legal LLC has represented IUL clients nationally, including high-profile clients. Many IUL firms offer free claim reviews. You can also contact [email protected] for attorney referrals tailored to your situation.

Current Status & 2026 Updates

PFA Pyramid Scheme Case — Closed

The PFA class action is fully resolved. The Ninth Circuit upheld the settlement on August 21, 2024, and class members received payments in October 2024. If you believe you were eligible but didn’t receive a payment, you should contact Class Counsel or the claims administrator as soon as possible.

IUL Illustrations Case — Active

The Virani v. NLV Financial case is ongoing. As of early 2026, the amended complaint (adding state law claims) is pending. No trial date has been set, and no settlement has been announced. National Life continues to dispute all allegations.

Separately, a RICO lawsuit was filed in January 2025 in the U.S. District Court for the District of Vermont, challenging proprietary interest crediting strategies used across multiple IUL carriers. This represents a broader escalation of IUL litigation industry-wide, and National Life is among the carriers targeted.

What to Watch in 2026

| Upcoming Development | Expected Timeframe | Significance |

|---|---|---|

| Ruling on NLV motion to dismiss | 2026 | Will determine if IUL case proceeds |

| Vermont RICO litigation progress | 2026 | Could result in significant industry-wide exposure |

| Potential new state-level IUL regulations | Ongoing | Regulators increasing oversight of IUL illustrations |

| Additional class action filings | Likely | IUL litigation volume continues to grow |

Frequently Asked Questions

What is the National Life Group lawsuit?

Quick Answer: It’s two separate lawsuits — a pyramid scheme class action involving marketing partner Premier Financial Alliance (settled for $50M in 2024) and an active IUL misrepresentation lawsuit filed in October 2024.

The pyramid scheme case alleged that PFA and National Life’s subsidiary targeted immigrant communities with an illegal recruitment scheme. The IUL case alleges that National Life’s indexed life insurance policies used misleading illustrations and delivered 0% returns despite market gains.

Is the National Life Group settlement still open?

Quick Answer: No. The PFA settlement claim period has closed. Payments were distributed to eligible class members in October 2024.

If you believe you were eligible but missed out, contact class counsel immediately. Courts occasionally allow late claims in narrow circumstances.

Who was eligible for the PFA settlement?

Quick Answer: People who enrolled as PFA associates and bought a Living Life or Living Life by Design IUL policy in California between January 1, 2014, and March 17, 2023.

The class was limited to California-based purchases under California’s Unfair Competition Law and Endless Chain Law.

How much did class members receive?

Quick Answer: It varied based on premiums paid and whether policies were active or lapsed. The representative plaintiff received $2,370 — about 67% of premiums paid after deductions.

The total settlement ceiling was approximately $50 million over and above cash surrender values. Individual amounts reflected a rescission model that aimed to return claimants to their pre-policy financial position.

What immigrant communities were targeted in the pyramid scheme lawsuit?

Quick Answer: The lawsuit specifically identified Chinese, Vietnamese, and Filipino immigrant communities as the primary targets of the alleged recruitment scheme.

The scheme exploited affinity trust within these communities — the same social bonds that normally help communities support each other were weaponized to pressure recruits to bring in friends and family members.

What is an IUL policy and why is it controversial?

Quick Answer: An Indexed Universal Life (IUL) policy is a permanent life insurance product where cash value growth is tied to a stock market index, with a floor (usually 0%) and a cap on gains.

Controversy arises because insurers show illustrations based on hypothetical or back-tested index performance, which may significantly overstate what policyholders will actually earn. Internal fees can also erode returns substantially. The result is that many policyholders find their policies severely underperform projections.

What is the Virani v. NLV Financial lawsuit about?

Quick Answer: Indiana resident Sanya Virani sued National Life after her IUL policy earned 0% interest in its first year, while she faced a $49,618 surrender charge to exit.

She alleges breach of contract and RICO violations, arguing that National Life’s policy illustrations relied on fraudulent back-tested index data. The case was filed October 31, 2024, in Vermont federal court and is still active. Crown Asset Management Lawsuit

Did National Life admit wrongdoing in the PFA settlement?

Quick Answer: No. Neither PFA nor Life Insurance Company of the Southwest admitted liability as part of the settlement.

However, both agreed to significant changes in business practices — including restrictions on deceptive marketing — as part of the settlement terms. Legal experts have noted that settling for $50 million speaks for itself.

What is the US Pacesetter Index?

Quick Answer: It’s a proprietary index launched by National Life in December 2021, used as a crediting strategy in their IUL policies. It tracks multiple asset classes and U.S. equities.

Critics allege that National Life illustrated the index using back-tested historical performance data rather than actual live returns, giving policyholders an unrealistically positive picture of expected gains.

What happened in the September 2025 court ruling?

Quick Answer: A Vermont federal judge dismissed two National Life corporate entities from the Virani lawsuit, but the case continues against the remaining defendants.

NLV Financial Corporation argued that IUL illustrations are “heavily regulated by insurance authorities” and do not constitute a contract. The case continues as of early 2026.

Can I still sue National Life over my IUL policy?

Quick Answer: Possibly, yes — especially if your policy has returned significantly less than illustrated, or if you were sold the product under misleading circumstances.

Your ability to file depends on your state’s statute of limitations, the specific facts of your case, and whether your policy contains an arbitration clause. An IUL attorney can assess your situation for free.

What is “affinity fraud” and how did it apply here?

Quick Answer: Affinity fraud is when scammers exploit trust within a close-knit community — religious groups, ethnic communities, professional associations — to run financial schemes.

The PFA lawsuit alleged a textbook affinity fraud scenario: recruiters targeted Chinese, Vietnamese, and Filipino immigrants specifically because trust within those communities made it easier to pressure friends and family into buying expensive policies and joining the scheme.

What changes did PFA and National Life agree to as part of the settlement?

Quick Answer: The settlement included specific business practice changes, including restrictions on deceptive marketing representations used to recruit PFA associates.

While the exact terms are detailed in the settlement stipulation filed with the court, the practice reforms were a significant non-monetary component of the resolution.

How do I check if I’m a class member in the PFA case?

Quick Answer: You can review the class definition at pfasettlement.com or contact class counsel directly.

The class covers PFA associates who purchased Living Life policies in California between 2014 and March 17, 2023. If you’re unsure whether you qualify, the settlement website has FAQs and contact information for the claims administrator.

What should I do if my National Life claim has been delayed or denied?

Quick Answer: Document everything, file a written complaint with National Life, and if unresolved, escalate to your state’s Department of Insurance.

BBB complaints against National Life show a pattern of delayed disbursements, unanswered calls, and claim processing issues. If you’re experiencing unexplained delays — especially on disability riders, annuity withdrawals, or death benefits — an insurance dispute attorney can help you assert your rights.

Does the pyramid scheme lawsuit affect my existing National Life policy?

Quick Answer: Not directly, unless you were a PFA-enrolled associate who purchased a qualifying Living Life policy in California.

If you purchased your National Life policy through a different channel or in a different state, the PFA class action settlement does not affect your policy. However, the broader IUL litigation landscape does affect how regulators are scrutinizing IUL products, which could lead to industry-wide practice changes that benefit all policyholders.

Are there other active lawsuits against National Life?

Quick Answer: Yes. Beyond the Virani IUL case, National Life is named in broader RICO IUL litigation filed in Vermont in January 2025, alongside other major carriers.

Multiple insurance carriers — including Allianz, Minnesota Life, Transamerica, Pacific Life, and Prudential — are facing similar IUL-related litigation in 2025–2026. This is a systemic industry issue, not isolated to National Life.

Where can I find legal help with a National Life claim?

Quick Answer: IUL litigation firms like RP Legal LLC offer free consultations. You can also contact [email protected] for a referral to attorneys handling National Life claims specifically.

Most IUL attorneys work on a contingency basis — meaning you pay nothing unless they recover money for you.

National Life Group: Company Background

National Life Group is a Vermont-based mutual holding company that has been in business for over 175 years. Its subsidiaries include National Life Insurance Co., Life Insurance Company of the Southwest, and Equity Services, Inc. The company markets life insurance, annuities, and investment products.

Despite the lawsuits, National Life currently holds an A+ rating from both A.M. Best and Standard & Poor’s — reflecting strong financial health. However, class action litigation, RICO allegations, and growing IUL-related scrutiny have placed the company under increased regulatory and reputational pressure.

It’s important to note that National Life Group (headquartered in Vermont) is distinct from National Life and Accident Insurance Company, which was acquired by American General/AIG. These are separate companies.

This article is for informational purposes only and does not constitute legal advice. If you believe you have a claim against National Life Group or any of its subsidiaries, consult a licensed attorney in your state. Laws and case status may have changed since publication. Last updated: March 2026.