NetCredit, an online lender owned by Enova International, has faced a wave of lawsuits, federal enforcement actions, and state investigations over its high-interest loans — some carrying APRs as high as 99.99%. If you’ve ever borrowed from NetCredit or are currently repaying a loan, there’s a real chance your loan is legally challenged and you may owe less than you think — or nothing at all.

This guide covers every active legal action against NetCredit, who is affected, what your rights are, and exactly what steps to take right now.

Quick Answer: There is no single finalized class action settlement with an open claims portal for NetCredit borrowers as of March 2026. What does exist is significant: a $15 million federal enforcement penalty against NetCredit’s parent Enova International, an active federal class action lawsuit filed in 2024, ongoing law firm investigations actively recruiting borrowers, and a legal theory — the “true lender” doctrine — that could make your NetCredit loan partially or entirely unenforceable depending on your state. Emuaid Lawsuit

NetCredit Lawsuit Overview: Fast Facts

| Topic | Details |

|---|---|

| Company | NetCredit (brand of Enova International, Inc.) |

| Parent Company | Enova International, Inc. (NYSE: ENVA) |

| Headquarters | Chicago, Illinois |

| Loan Range | $1,000 – $10,000 personal loans; $500 – $4,500 lines of credit |

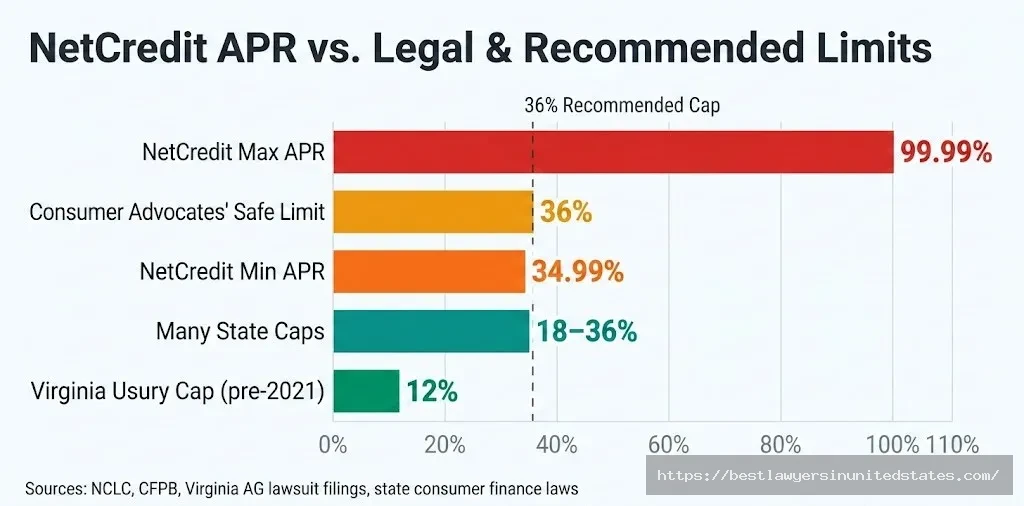

| APR Range | 34.99% – 99.99% |

| Bank Partners | Republic Bank & Trust (KY), Capital Community Bank (UT) |

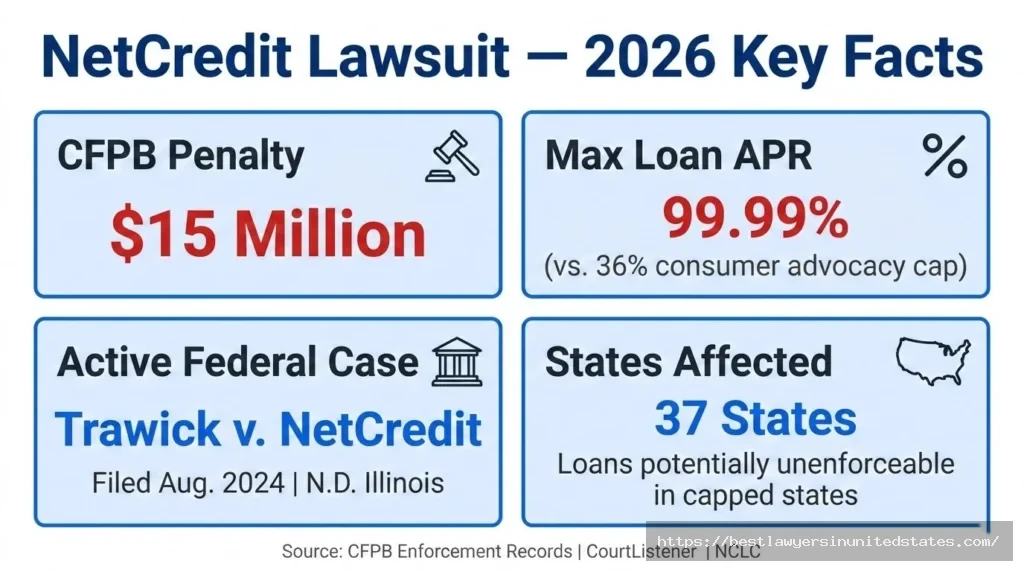

| CFPB Fine (2023) | $15 million civil penalty |

| Active Federal Case | Trawick v. NetCredit Loan Services, LLC, N.D. Ill., Case 1:24-cv-07481 |

| Investigating Law Firms | Warren Terzian LLP (active) |

| Key Legal Theory | “True Lender” / Rent-a-Bank scheme |

| States with Rate Cap Issues | Virginia, California, Illinois, North Carolina, and others |

What Is the NetCredit Lawsuit About?

The Core Allegation: Charging Interest Rates That Break State Law

Here’s the short version: most states cap interest rates on personal loans. NetCredit charges up to 99.99% APR. The lawsuit argument is that NetCredit uses a legal workaround — partnering with out-of-state banks — to escape those caps. Critics say the bank is just a front, and that NetCredit is the real lender all along.

If courts agree, your loan may have been illegal from the start.

NetCredit targets people with bad or no credit who can’t get loans from traditional banks. That part is legal. The controversy is how much it charges them, and whether the structure used to justify those charges holds up in court.

What Is the “Rent-a-Bank” Scheme?

This is the central legal theory behind most NetCredit litigation, and it’s worth understanding because it directly affects whether you owe money on your loan.

Banks chartered in certain states (particularly Utah and Kentucky) aren’t subject to interest rate caps in other states. NetCredit’s loans are technically originated by two partner banks — Republic Bank & Trust of Kentucky, and Capital Community Bank of Utah. Because those banks aren’t bound by your state’s usury laws, the loans carry much higher rates than your state normally allows.

NetCredit then immediately purchases those loans back from the bank and services them itself. Critics — including the National Consumer Law Center (NCLC), consumer advocacy groups, and several state attorneys general — argue that the bank is just “renting” its charter to NetCredit to get around the law. The bank takes on little actual risk; NetCredit runs the whole operation.

The legal argument is that NetCredit is the true lender, not the bank. And if NetCredit is the true lender, your state’s interest rate limits apply — which means the rate on your loan may be illegal.

Who Filed the Most Recent Lawsuit?

The most active federal case right now is Trawick v. NetCredit Loan Services, LLC (Case No. 1:24-cv-07481, U.S. District Court for the Northern District of Illinois). Lead plaintiff Janet Trawick filed the class action complaint on August 20, 2024, represented by attorneys from Edelman, Combs, Latturner & Goodwin. The case was assigned to Judge April M. Perry.

As of late 2025, the case is still in active litigation. NetCredit moved to compel arbitration — a common defense tactic — and the court has been weighing the impact of a related Seventh Circuit ruling on that motion.

Separately, the law firm Warren Terzian LLP is actively investigating potential class actions and arbitrations against NetCredit. They are currently recruiting borrowers who want to challenge their loans. You can find their intake form at warrenterzian.com/cases/enova-netcredit-class-action.

Timeline of Key Legal Actions Against NetCredit

| Date | Event | Details |

|---|---|---|

| 2018 | Virginia AG sues NetCredit | Claims $47M+ in illegal loans above state’s 12% usury cap; NetCredit charged up to ~150% APR |

| 2019 | CFPB Order #1 | Enova/NetCredit ordered to stop unauthorized bank withdrawals; pay consumer redress |

| 2020–2021 | State investigations expand | Illinois, North Carolina, California borrowers complain to CFPB in large numbers |

| 2021 | Virginia Supreme Court proceedings | Case reaches U.S. Supreme Court level on “true lender” / preemption questions |

| November 15, 2023 | CFPB $15M Penalty | CFPB fines Enova $15 million for violating 2019 order and repeating unauthorized withdrawals |

| August 20, 2024 | Trawick class action filed | Federal class action filed in N.D. Illinois over unlawful lending practices |

| Early 2025 | NetCredit moves to compel arbitration | Standard legal defense attempt to block class action; court weighing Seventh Circuit precedent |

| August 22, 2025 | Court opinion issued | Judge Perry issues opinion in Trawick case (full ruling available on Justia/CourtListener) |

| September 2, 2025 | CFPB terminates 2023 order | Post-administration change, CFPB waives alleged non-compliance under 2023 order |

| November 2025 | Tenth Circuit rent-a-bank ruling | Federal appeals court limits rent-a-bank schemes in Colorado — could influence NetCredit cases nationally |

| March 2026 | Warren Terzian LLP active | Law firm actively recruiting NetCredit borrowers for arbitration/class action |

Who Is Being Sued, and Who’s Behind It?

The defendant: NetCredit Loan Services, LLC, and its parent Enova International, Inc. (NYSE: ENVA), headquartered in Chicago. Enova also operates CashNetUSA and OnDeck.

Law firms currently active on these cases:

| Law Firm | Role | Contact |

|---|---|---|

| Warren Terzian LLP | Investigating class actions and arbitrations; currently recruiting borrowers | warrenterzian.com |

| Edelman, Combs, Latturner & Goodwin | Lead counsel in Trawick class action | ecattorneys.com |

| State attorneys general offices | Enforcement actions in Virginia, Illinois, and others | Your state AG’s website |

The CFPB $15 Million Penalty: What Happened and What It Means for You

In November 2023, the Consumer Financial Protection Bureau (CFPB) hit Enova International — NetCredit’s parent — with a $15 million civil money penalty. This wasn’t the first time. The CFPB had issued a prior order in 2019 for the same type of conduct.

What did Enova do? According to the CFPB, the company debited consumers’ bank accounts without their authorization. In plain terms: they took money from borrowers’ accounts without permission, or after those borrowers had been granted loan extensions. The 2023 action found Enova had violated the 2019 order by repeating that same behavior.

The order required Enova to:

- Provide redress to all consumers whose accounts were debited without proper consent

- Pay the $15 million penalty

- Come into compliance with the Consumer Financial Protection Act

Important update for 2025–2026: On September 2, 2025, the CFPB — under new leadership after the change in presidential administration — terminated the 2023 enforcement order and “waived any alleged non-compliance.” This is a significant development worth noting. Critics of the change argue it leaves affected borrowers without a federal enforcement backstop; supporters frame it as regulatory correction.

Even with the federal order terminated, the underlying conduct still forms the basis for private lawsuits, and state-level enforcement remains active.

What Are the Main Legal Claims Against NetCredit?

Lawsuits and enforcement actions against NetCredit cluster around four main arguments:

1. Unlawful Interest Rates Many states cap personal loan APRs at 36% or lower. Virginia’s cap is 12%. NetCredit charges up to 99.99%. The legal question is whether the bank-partnership structure legally allows this, or whether it’s a sham that should be disregarded.

2. Rent-a-Bank / True Lender Doctrine This is the big one. Attorneys argue that NetCredit — not its bank partners — is the true lender on these loans, because NetCredit: markets the loans, makes the credit decisions, funds the loans, and immediately purchases them back from the bank. If that argument succeeds in your state, your loan’s interest rate becomes subject to your state’s cap.

3. Unauthorized Bank Account Withdrawals The CFPB found that Enova debited borrowers’ accounts without proper authorization — twice. This is a concrete harm affecting specific borrowers, separate from the interest rate debate.

4. Failure to Clearly Disclose Loan Terms Borrowers consistently report that the true total cost of their loans wasn’t made clear at the time of borrowing. Multiple consumer complaints to the CFPB cite surprise at the total repayment amount — often two or three times the original loan amount.

Which States Are Most Affected?

Your ability to challenge a NetCredit loan depends significantly on where you live. These are the states where legal exposure for NetCredit is highest:

| State | Why It Matters | Status |

|---|---|---|

| Virginia | AG sued NetCredit; state usury cap is 12% | NetCredit no longer operates in VA as of 2021 |

| California | AG active on rent-a-bank schemes; 36% cap (CCCFA 2020) | California borrowers may have viable claims |

| Illinois | Active CFPB complaint volume; Trawick case filed in N.D. Ill. | Active litigation |

| North Carolina | Strong state usury enforcement | High-risk state for NetCredit’s model |

| Colorado | Tenth Circuit (Nov. 2025) limited rent-a-bank in this state | Most protected as of late 2025 |

| Ohio | Rate caps on certain loan types | Potential exposure |

| Pennsylvania | Long-standing usury laws | Borrowers should consult an attorney |

| Arkansas | Constitutional 17% rate cap | NetCredit does not operate here |

If you’re in a state with a rate cap below NetCredit’s APR, your loan may be subject to challenge.

Could You Actually Get Your Money Back — or Stop Owing?

Possibly, yes. Here’s what outcomes are being sought across different legal actions:

Loan Cancellation: If a court or arbitrator finds NetCredit is the true lender and your state’s rate cap applies, the loan may be unenforceable — meaning you might not have to pay any remaining balance.

Refund of Interest Overpaid: If you’ve already paid off a loan that charged an illegal rate, you could be owed a refund of the interest portion that exceeded your state’s legal cap.

Credit Report Correction: If NetCredit’s loans are found unenforceable, negative credit reporting related to those loans could be removed.

Damages for Unauthorized Withdrawals: If NetCredit debited your bank account without proper authorization, you may be entitled to damages under the Electronic Fund Transfer Act (EFTA) and/or the Consumer Financial Protection Act.

None of these outcomes are guaranteed. The litigation is ongoing, and results will vary by state and by individual circumstances.

Do You Qualify? Questions to Ask About Your Loan

You may have a viable legal claim if:

- You took out a NetCredit loan and your state has a rate cap below your loan’s APR

- You paid more in interest than would have been allowed under your state’s law

- NetCredit debited your bank account after you cancelled authorization or were granted a loan extension

- You were not clearly informed of the total repayment amount before taking the loan

- Your loan was originated on or after approximately 2016 (when the bank partnership model was in active use)

You likely have weaker grounds if:

- You took out a loan in a state without applicable rate caps

- You signed an arbitration agreement (though attorneys are actively challenging these)

- Your loan has been fully repaid and you suffered no documented harm beyond the interest rate itself

The Arbitration Clause Problem — and Why It May Not Stop You

NetCredit’s loan agreements contain arbitration clauses — language requiring disputes to go to private arbitration rather than court. This is a common tactic among high-interest lenders and makes class action lawsuits significantly harder to bring.

In the Trawick case, NetCredit moved to push the lawsuit into arbitration. The court has been weighing this closely, including considering the impact of a related Seventh Circuit Court of Appeals decision. Jardiance Lawsuit 2026

Here’s what you should know:

Arbitration isn’t necessarily bad for you. Warren Terzian LLP specifically offers individual arbitrations against NetCredit in addition to class actions. For some borrowers, individual arbitration may actually result in faster, more favorable outcomes than waiting for a class action to resolve — which can take years.

Arbitration clauses can sometimes be challenged. Courts have found arbitration clauses unenforceable in some circumstances, particularly when the clause is found to be unconscionable or when the lending itself is found to be illegal.

Practical step: Before assuming arbitration bars your claim, consult with a consumer rights attorney. The landscape here is evolving rapidly.

What to Do Right Now If You Have a NetCredit Loan

Here’s a practical action plan — in order of priority:

Step 1: Gather your loan documents Pull together your original loan agreement, all payment records, any email communications with NetCredit, and your bank statements showing payment history. These documents are essential for any legal challenge.

Step 2: Check your state’s interest rate cap Search “[your state] consumer loan interest rate cap” or contact your state attorney general’s consumer protection office. If your NetCredit APR exceeds that cap, you have a stronger potential claim.

Step 3: Pull your credit reports Go to AnnualCreditReport.com for free reports from all three bureaus. Check what NetCredit is reporting — this is relevant if you want to challenge the reporting as part of any legal action.

Step 4: File a CFPB complaint Even with recent changes to the CFPB, filing a complaint at consumerfinance.gov/complaint creates an official record of your experience. It’s free, takes about 10–15 minutes, and contributes to the documented record regulators and attorneys use to build cases.

Step 5: Contact an attorney Warren Terzian LLP is actively taking cases. Their intake form is at warrenterzian.com/cases/enova-netcredit-class-action. You can also use your state bar’s lawyer referral service to find a consumer rights or predatory lending attorney. Most offer free initial consultations.

Step 6: File a complaint with your state AG If you’re in a state actively enforcing usury laws, a complaint to your state attorney general’s consumer protection division adds to their enforcement record against NetCredit.

Required Documents Checklist

| Document | Why You Need It | Where to Find It |

|---|---|---|

| Original loan agreement | Proves loan terms, APR, bank partnership structure | Your NetCredit account or email inbox from loan origination |

| Payment history / account statements | Documents what you’ve paid, including interest | NetCredit account dashboard or your bank statements |

| Bank statements showing deductions | Proves when and how much was withdrawn | Your bank’s online portal |

| Any communication about loan extensions | Critical if unauthorized withdrawals occurred after extension | Your email inbox |

| Credit reports | Shows what NetCredit reported to bureaus | AnnualCreditReport.com (free) |

| Your state’s rate cap documentation | Supports your claim that your APR exceeded legal limits | State AG website or NCLC resources |

How This Compares to Similar Predatory Lending Cases

NetCredit’s situation isn’t unique. Several similar lenders have faced enforcement actions and settlements that give useful context:

| Company | Action | Outcome |

|---|---|---|

| Enova / NetCredit (2023) | CFPB enforcement | $15M civil penalty, consumer redress for unauthorized withdrawals |

| OppLoans / OppFi | DC AG lawsuit over rent-a-bank scheme | $2 million settlement, ceased DC operations |

| EasyPay Finance | Massachusetts AG settlement (May 2024) | $625,000 in restitution, ceased loan collection |

| CashCall | CFPB action on true lender doctrine | Found to be true lender; loans voided |

| Think Finance | State AG actions, CFPB | $40M+ settlement across multiple states |

| Plain Green Loans (tribal lender) | FTC action | $3.5M settlement, consumer refunds |

The CashCall case is the most instructive. A federal court found that CashCall — not its tribal bank partner — was the true lender, and voided the loans entirely. Attorneys pursuing NetCredit cases are using very similar arguments.

The 2025 Tenth Circuit Ruling: A Game-Changer for Rent-a-Bank Cases

In November 2025, the U.S. Court of Appeals for the Tenth Circuit issued a ruling in National Association of Industrial Bankers v. Weiser that significantly limits rent-a-bank schemes in Colorado. The court found that when a state opts out of federal rate exportation rules, that opt-out protects consumers from loans made by out-of-state banks — exactly the kind of loans NetCredit makes.

This matters nationally because:

- It validates the legal theory that borrowers’ home state law should apply

- Other states can now pass similar opt-out legislation with greater confidence it’ll hold up

- The reasoning may influence how courts in other circuits approach similar cases

As of March 2026, Colorado borrowers have the strongest protections. Other states may follow. If you live in a state currently considering usury reform legislation, this ruling is directly relevant.

Frequently Asked Questions

Is there a NetCredit class action settlement I can file a claim for right now?

No. As of March 2026, there is no finalized NetCredit class action with an open claims portal. The active federal case (Trawick) is still being litigated. What does exist is an active law firm recruiting borrowers for individual arbitrations and potential future class actions. If a settlement is reached, this page will be updated immediately with filing details.

My NetCredit APR was over 36% — can I sue?

It depends on your state. If your state has a rate cap lower than your loan’s APR and if a court accepts the “true lender” argument, you may have a viable claim. Contact a consumer rights attorney to evaluate your specific situation.

NetCredit took money from my bank account without my permission. What should I do?

File a CFPB complaint immediately at consumerfinance.gov/complaint. Also contact your bank to dispute the unauthorized transaction. This specific conduct was what led to the CFPB’s $15 million fine against Enova in 2023. You may have a claim under the Electronic Fund Transfer Act.

What is the “true lender” doctrine?

It’s the legal principle that the entity that actually controls a loan — makes the credit decision, bears the risk, and profits from it — is the true lender, regardless of who’s technically listed on the paperwork. If NetCredit is found to be the true lender rather than its bank partners, your state’s interest rate limits would apply to your loan.

I already paid off my NetCredit loan. Can I still make a claim?

Possibly. If you overpaid interest above your state’s legal cap, you may be owed a refund of the excess. Statutes of limitations vary by state, but consumer protection claims often run 4–6 years. Contact an attorney to evaluate whether your payoff date falls within the filing window.

Do I need a lawyer to fight NetCredit?

For filing a CFPB complaint or contacting your state AG — no. For pursuing individual arbitration or joining a class action — yes, and most attorneys handling these cases work on a contingency basis, meaning no upfront cost to you.

Can NetCredit sue me if I stop paying?

Yes. Not paying is different from successfully challenging a loan. If you stop paying without legal guidance, NetCredit can pursue collection, report the default to credit bureaus, and eventually file suit. Don’t stop paying based solely on what you read online — consult an attorney first.

How do I find out if I’m part of the Trawick class action?

The case is still in litigation and no class has been certified yet. Keep an eye on CourtListener (courtlistener.com) for updates, or sign up through Warren Terzian LLP’s intake form to be connected with the legal team following these cases.

What states does NetCredit not operate in?

NetCredit does not currently offer loans in Arkansas, Colorado (as of recent legal changes), Connecticut, Georgia, Massachusetts, New Hampshire, New Jersey, New York, North Carolina, Pennsylvania, Vermont, Virginia, West Virginia, and some others. If you’re in one of these states and had a past NetCredit loan, your legal exposure is worth discussing with an attorney.

What happened to the CFPB order from 2023?

The CFPB terminated its 2023 enforcement order against Enova on September 2, 2025, under new federal leadership, and waived alleged non-compliance. Critics argue this leaves consumers without federal protection; private lawsuit rights are unaffected.

How long do I have to bring a legal claim?

This varies by claim type and state. CFPB and ECOA violations often have two-year statutes of limitations. State consumer protection claims can range from three to six years. Electronic Fund Transfer Act claims are generally one year. Don’t wait — consult an attorney promptly.

Is NetCredit still making loans right now?

Yes. As of March 2026, NetCredit continues to operate and originate loans in roughly 37 states. Being actively sued hasn’t stopped the lending operation.

What’s the difference between the CFPB fine and a class action?

The CFPB fine is a government enforcement action; the money goes to the government and to directly harmed consumers identified by regulators. A class action is a private lawsuit where affected borrowers sue together and share the recovery. They address overlapping but distinct harms.

I signed an arbitration agreement. Am I completely blocked from suing?

Not necessarily. Arbitration clauses are being challenged in court (including in the Trawick case itself), and individual arbitration against NetCredit is actively being pursued by law firms. Signing an arbitration clause does not automatically end your options.

What if I can’t afford to keep making payments on my NetCredit loan?

Contact a nonprofit credit counselor (find one at nfcc.org), contact your state’s legal aid office for free advice, or reach out to Warren Terzian LLP if you’re interested in exploring whether your loan can be challenged. Do not ignore the situation — missed payments have credit and legal consequences.

Where to Get Help Right Now

| Resource | What They Do | How to Reach Them |

|---|---|---|

| Warren Terzian LLP | Recruiting NetCredit borrowers for arbitration/class action | warrenterzian.com/cases/enova-netcredit-class-action |

| CFPB Complaint Portal | File a formal complaint against NetCredit/Enova | consumerfinance.gov/complaint |

| Your State Attorney General | State-level consumer protection enforcement | Search “[your state] attorney general consumer protection” |

| National Consumer Law Center | Research and consumer advocacy resources | nclc.org |

| Legal Aid / State Bar Referral | Free or low-cost legal help | lawhelp.org or your state bar’s referral service |

| AnnualCreditReport.com | Check what NetCredit is reporting | annualcreditreport.com |

What Happens Next: What to Watch

The Trawick arbitration ruling. The court’s decision on NetCredit’s motion to compel arbitration will either push the class action into private arbitration or allow it to proceed in federal court. This is the most consequential near-term development.

State legislative action. Following the Tenth Circuit’s November 2025 ruling, several states are considering DIDMCA opt-out legislation that would limit rent-a-bank lending within their borders. If your state passes such a law, NetCredit’s model becomes directly challengeable there.

Enova’s bank charter application. Enova has applied to become a national bank itself. If approved, it would no longer need bank partners and the rent-a-bank argument would lose its relevance for future loans. The application status should be monitored through the OCC’s public filings.

Ongoing CFPB posture. Consumer advocacy groups are watching whether the CFPB’s current reduced enforcement posture persists, and whether state AGs fill the gap with more aggressive state-level action. How Long Does a Personal Injury Lawsuit Take?