Quick Answer Box

- The SeaWorld class action lawsuit settlement refers to multiple separate legal actions against SeaWorld Entertainment Inc., the most significant being a $65 million securities fraud settlement in Case No. 3:14-cv-02129-MMA-AGS, U.S. District Court for the Southern District of California, resolving investor claims tied to the Blackfish documentary.

- Investors who purchased SeaWorld Entertainment (NYSE: SEAS) stock between August 29, 2013, and August 12, 2014, are the primary class in the securities settlement; separate consumer cases cover annual pass holders and COVID-19 refund claimants.

- The securities class produced a per-share recovery that varied by purchase price and timing; consumer refund cases produced park credit and partial cash refunds depending on the specific case and jurisdiction.

Case Snapshot

| Detail | Information |

|---|---|

| Primary Court | U.S. District Court for the Southern District of California |

| Securities Case Number | Case No. 3:14-cv-02129-MMA-AGS |

| Presiding Judge | Hon. Michael M. Anello |

| Lead Plaintiff | Arkansas Teacher Retirement System |

| Lead Plaintiffs’ Firm | Robbins Geller Rudman and Dowd LLP |

| Filing Date | September 9, 2014 (securities complaint) |

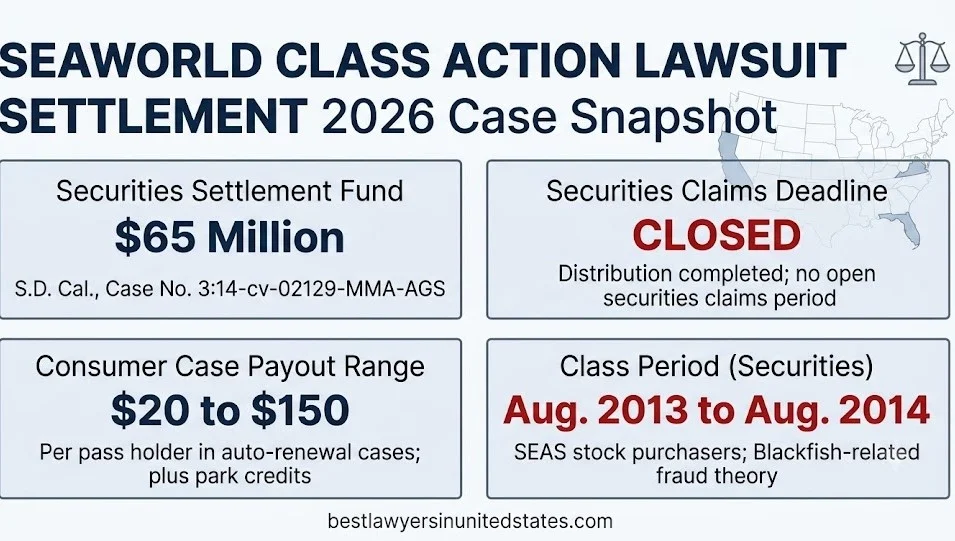

| Securities Settlement Fund | $65 million |

| Class Period (Securities) | August 29, 2013 to August 12, 2014 |

| Consumer COVID Refund Cases | Multiple state courts; California, Florida, Virginia |

| Pass-Holder Cases | San Diego Superior Court; various state venues |

| Securities Case Status | Settled and closed; distribution completed |

| Consumer Cases Status | Varies by case; some resolved, some ongoing as of 2026 |

The SeaWorld class action lawsuit settlement landscape involves at least three distinct litigation tracks, each with separate courts, class definitions, and outcomes. The largest and most consequential was the $65 million securities fraud settlement in the Southern District of California, anchored by investor claims that SeaWorld executives misled the market about the financial impact of the 2013 documentary Blackfish.

The securities case did not stand alone. SeaWorld simultaneously faced consumer class actions from pass holders alleging deceptive practices and, starting in 2020, COVID-19 refund litigation from customers whose visits were cancelled during pandemic-related park closures. Each case produced separate claims administrators, separate eligibility criteria, and separate timelines.

Understanding which case applies to a specific claimant requires knowing when they purchased stock, when they held a SeaWorld pass, or whether their park visit was cancelled. Those distinctions determine eligibility, not the general category of “SeaWorld lawsuit.”

This analysis addresses each litigation track in sequence, with the court record specifics that aggregator sites consistently omit.

SeaWorld Class Action Lawsuit Settlement: Overview of All Cases

The SeaWorld class action lawsuit settlement record encompasses at least five distinct legal actions filed across federal and state courts between 2014 and 2022. Each action targeted a different category of alleged corporate misconduct.

No single settlement resolved all of these cases. The $65 million securities fraud settlement in the Southern District of California resolved the investor claims. Separate state court and federal court actions addressed consumer protection, annual pass contracts, and COVID-related closures.

Overview of SeaWorld litigation tracks:

| Case Type | Court | Settlement/Status | Class |

|---|---|---|---|

| Securities fraud (Blackfish) | S.D. Cal., No. 3:14-cv-02129 | $65M settled and closed | SEAS stock purchasers, Aug. 2013 to Aug. 2014 |

| Annual pass holder deception | San Diego Superior Court | Settled with park credits and partial cash | California pass holders |

| COVID-19 refund litigation | Multiple state and federal courts | Partially settled; some active as of 2026 | Ticket and pass purchasers with cancelled visits |

| Animal welfare / orca captivity | Federal court; various state filings | Largely dismissed; some ongoing | Consumer fraud theory; no direct claimant class |

| Employee whistleblower | Multiple venues | Resolved separately | Former SeaWorld employees |

Attorney Insight: Attorneys who tracked the full SeaWorld litigation portfolio note that the simultaneous multi-docket structure created significant confusion among potential claimants, with many investors and consumers unsure which case applied to their specific purchase or investment timeline.

SeaWorld Securities Fraud Class Action

The SeaWorld securities fraud class action is the anchor litigation in the company’s legal history, filed on September 9, 2014, in the U.S. District Court for the Southern District of California, Case No. 3:14-cv-02129-MMA-AGS.

The complaint alleged that SeaWorld Entertainment Inc. and certain of its executive officers violated Section 10(b) of the Securities Exchange Act of 1934 and Rule 10b-5 thereunder by making materially false and misleading statements about the company’s business, operations, and financial condition.

Specifically, plaintiffs alleged that SeaWorld knew the Blackfish documentary, released in July 2013, was damaging attendance, revenue, and corporate partnerships, but that executives made public statements minimizing that impact throughout the class period.

Core securities fraud allegations:

- SeaWorld executives made false public statements downplaying Blackfish’s attendance impact

- Internal documents and communications contradicted public representations

- When the truth emerged through corrective disclosures in August 2014, SEAS stock dropped sharply

- Investors who purchased during the class period suffered quantifiable losses caused by that inflation and subsequent correction

Attorney Insight: Attorneys handling securities fraud class actions note that the corrective disclosure theory in this case was unusually clean, because the gap between SeaWorld’s public minimization of Blackfish’s impact and the eventual admission of its severity was documented in the company’s own quarterly earnings calls and SEC filings.

Litigation Watch: The SeaWorld securities fraud complaint, filed in September 2014 and anchored in documented contradictions between executive public statements and internal corporate data, produced one of the cleaner corrective disclosure theories in entertainment-sector securities litigation of that decade.

SeaWorld Blackfish Lawsuit: How a Documentary Became a Securities Case

The Blackfish lawsuit is the informal name for the SeaWorld securities fraud class action, and the connection between the documentary and the investor claims is more legally precise than most media coverage suggests.

Blackfish, directed by Gabriela Cowperthwaite and released by CNN Films in July 2013, documented the conditions under which orca whales were kept at SeaWorld parks and the consequences for both the animals and SeaWorld trainers. The film received wide distribution after its theatrical release and generated immediate negative media coverage of SeaWorld’s practices.

The legal theory was not that the film was actionable. The theory was that SeaWorld executives, knowing the film was damaging business metrics, continued to make optimistic public statements about attendance, revenue, and corporate partnership stability that were materially false when made. The class period of August 29, 2013, to August 12, 2014, is bounded by the date of SeaWorld’s first post-Blackfish earnings call and the date of its first public acknowledgment of Blackfish-related attendance decline.

Blackfish-to-litigation timeline:

| Date | Event |

|---|---|

| July 2013 | Blackfish premieres at Sundance; CNN Films distributes |

| August 29, 2013 | SeaWorld Q2 2013 earnings call; start of securities class period |

| Q3 to Q4 2013 | Corporate partners begin withdrawing; SeaWorld executives dispute Blackfish impact publicly |

| Q1 to Q2 2014 | Attendance declines accelerate; executives continue minimizing Blackfish |

| August 12, 2014 | SeaWorld discloses Blackfish-driven attendance decline; SEAS stock drops sharply |

| September 9, 2014 | Securities class action complaint filed in S.D. Cal. |

Attorney Insight: Attorneys analyzing the case structure note that the breadth of the Blackfish-related corporate partner withdrawals, including Southwest Airlines, Hyundai, and numerous educational institutions, provided corroborating evidence of a known business impact that SeaWorld executives were simultaneously denying in public statements.

SeaWorld $65 Million Settlement: Terms and Structure

The $65 million SeaWorld securities fraud settlement is the largest financial resolution in the company’s litigation history. The settlement received final approval from Judge Michael M. Anello in the U.S. District Court for the Southern District of California.

The $65 million fund was established to compensate investors who purchased SeaWorld Entertainment Inc. (NYSE: SEAS) common stock during the class period of August 29, 2013, to August 12, 2014, and who suffered economic losses as a result of the alleged fraud. SeaWorld denied all liability as part of the settlement agreement, as is standard in securities class action resolutions.

Attorney fees and litigation expenses were paid from the settlement fund, consistent with PSLRA requirements. The lead plaintiffs’ firm, Robbins Geller Rudman and Dowd LLP, and co-counsel received court-approved fees from the fund prior to distribution to class members.

Settlement fund allocation structure:

| Component | Amount / Detail |

|---|---|

| Gross settlement fund | $65,000,000 |

| Attorney fees and expenses | Court-approved percentage from gross fund |

| Claims administration costs | Deducted from gross fund |

| Net fund available for distribution | Gross fund minus fees and expenses |

| Distribution basis | Pro rata, based on recognized loss per share |

| Minimum claim threshold | Set by plan of allocation |

Attorney Insight: Attorneys analyzing securities class action fee structures note that the PSLRA requires judicial approval of all fee applications and mandates that any class member may object to the fee request, a procedural protection that distinguishes securities class actions from many consumer class settlements.

SeaWorld Investor Lawsuit Settlement: The Arkansas Teacher Retirement System

The lead plaintiff in the SeaWorld securities fraud class action was the Arkansas Teacher Retirement System, a public pension fund that held SeaWorld Entertainment shares during the class period and suffered documented investment losses.

The selection of a public pension fund as lead plaintiff was consistent with the PSLRA’s preference for institutional investors with the largest financial stakes in the litigation. The Arkansas Teacher Retirement System’s participation signaled to the court that the case had institutional-grade oversight, which typically strengthens the credibility of the settlement terms presented for judicial approval.

Robbins Geller Rudman and Dowd LLP, one of the leading securities class action firms in the United States, served as lead counsel. The firm has recovered billions of dollars for institutional investor clients in securities fraud cases and has managed some of the largest securities class action settlements in U.S. history.

Lead plaintiff and counsel profile:

| Role | Entity |

|---|---|

| Lead plaintiff | Arkansas Teacher Retirement System |

| Lead plaintiffs’ counsel | Robbins Geller Rudman and Dowd LLP |

| Co-counsel | Additional plaintiffs’ firms (specified in court record) |

| Named defendants | SeaWorld Entertainment Inc., former CEO James Atchison, and other executive officers |

| Defendant’s counsel | Defense-side securities litigation firms (specified in court record) |

Attorney Insight: Attorneys monitoring the PSLRA lead plaintiff process note that the Arkansas Teacher Retirement System’s appointment followed the standard competitive process in which multiple institutions with significant share holdings competed for lead plaintiff status, and that institutional lead plaintiffs consistently produce higher per-share recoveries than individual investor lead plaintiffs in comparable cases.

Litigation Watch: The Arkansas Teacher Retirement System’s selection as lead plaintiff and Robbins Geller’s appointment as lead counsel established the institutional credibility that enabled the $65 million settlement to clear judicial scrutiny, including the loss causation and damages analysis required for final approval under PSLRA standards.

SeaWorld Settlement: How Much Per Share Did Investors Receive?

The per-share recovery in the SeaWorld securities fraud settlement varied by purchase price, sale price, and timing within the class period, calculated according to the plan of allocation approved by Judge Anello.

Securities class action plans of allocation are actuarial instruments. They calculate a “recognized loss” for each share purchased during the class period based on the difference between the inflation-adjusted purchase price and the inflation-adjusted sale price or the closing price at the end of the class period, whichever is lower.

Specific per-share recovery figures in the SeaWorld settlement depended on the volume of claims submitted and the total recognized losses presented by all claimants. The actual distribution amount per dollar of recognized loss was determined by dividing the net settlement fund by the total recognized losses across all valid claims.

How recognized loss was calculated:

| Variable | Description |

|---|---|

| Purchase price during class period | Price at which investor bought SEAS shares |

| Artificial inflation per share | Amount stock price was inflated due to alleged fraud |

| Sale price or class period end price | Lower of actual sale price or price at class period end |

| Recognized loss per share | Calculated from inflation schedule in plan of allocation |

| Pro rata distribution | Investor’s recognized loss divided by total recognized losses, multiplied by net fund |

Attorney Insight: Attorneys advising institutional investors in securities settlements consistently emphasize that per-share recovery in class actions is always a fraction of actual losses, because the settlement fund is shared across all claimants proportionally, and that investors with the largest recognized losses receive the largest absolute payments.

SeaWorld Pass Holder Class Action

The SeaWorld pass holder class action is a separate litigation track from the securities fraud case, targeting the company’s alleged deceptive practices in selling and administering annual park passes to consumers.

Multiple consumer class actions were filed against SeaWorld in California, Florida, and Virginia, the states where its parks are located, alleging that the company misrepresented the terms, benefits, and renewal conditions of its annual pass products. The California cases were primarily filed in San Diego Superior Court and the Southern District of California.

Pass holder claims centered on allegations that SeaWorld auto-renewed annual passes without adequate notice, charged renewal fees without authorization, misrepresented the parks and attractions included in pass benefits, and failed to provide promised discounts and access rights.

Annual pass holder claims by category:

- Unauthorized auto-renewal charges to credit and debit cards

- Failure to disclose pass renewal terms at point of sale

- Misrepresentation of park access and attraction availability

- Refusal to refund passes when park conditions changed materially

- Breach of contract in pass benefit administration

Attorney Insight: Attorneys handling consumer class actions against theme parks note that auto-renewal cases are among the most straightforward consumer protection claims in terms of liability, because the authorization failure is typically documented in the merchant’s own payment processing records, leaving little factual dispute about whether the charge was authorized.

SeaWorld Annual Pass Lawsuit: Deceptive Renewal Practices

The SeaWorld annual pass lawsuit focuses on the company’s subscription-style pass products and the specific renewal and billing practices that plaintiffs alleged violated California’s Automatic Renewal Law (Business and Professions Code Section 17601 et seq.) and the Consumer Legal Remedies Act (Civil Code Section 1750 et seq.).

California’s Automatic Renewal Law requires businesses to clearly disclose automatic renewal terms before charging customers, to obtain affirmative consent, and to provide a mechanism for cancellation. SeaWorld’s annual pass enrollment process allegedly failed to meet those statutory requirements in several respects.

The California auto-renewal litigation resulted in settlements requiring SeaWorld to revise its pass enrollment disclosures and, in some cases, provide refunds or park credits to affected pass holders. The precise terms varied by individual settlement agreement.

California Automatic Renewal Law requirements allegedly violated:

| Statutory Requirement | SeaWorld’s Alleged Failure |

|---|---|

| Clear disclosure of renewal terms before enrollment | Renewal terms buried in fine print or post-enrollment emails |

| Affirmative consent to auto-renewal | Pre-checked boxes or implied consent used |

| Easy cancellation mechanism disclosed | Cancellation process not adequately disclosed at enrollment |

| Reminder notice before renewal charge | Inadequate pre-renewal notice provided |

Attorney Insight: Attorneys practicing consumer protection in California note that automatic renewal law violations carry statutory remedies under the CLRA including actual damages, punitive damages, and attorney fees, making pass holder cases economically viable for plaintiffs’ counsel even when individual consumer losses are modest.

Litigation Watch: The SeaWorld annual pass litigation, running concurrently with the securities fraud case in some years, targeted the company’s consumer billing practices under California’s Automatic Renewal Law, a state statute that provides statutory damages independent of actual financial harm, fundamentally changing the economics of consumer class recovery.

SeaWorld COVID Refund Lawsuit

The SeaWorld COVID refund lawsuit is a category of consumer class actions filed beginning in mid-2020 after SeaWorld closed all of its parks in March 2020 in response to pandemic-related government orders.

Customers who had purchased annual passes, single-day tickets, or multi-day tickets before the March 2020 closures and could not use those purchases sought refunds or compensation. SeaWorld’s initial response in most markets was to offer extensions of pass validity periods or park credits rather than cash refunds. That response generated litigation in multiple jurisdictions.

The legal theories in the COVID refund cases varied. Some plaintiffs alleged breach of contract, asserting that SeaWorld’s closure constituted a failure of consideration for which cash refund was the appropriate remedy. Others alleged violations of consumer protection statutes. California, Florida, and Virginia cases proceeded on parallel tracks.

SeaWorld COVID refund case snapshot:

| State | Court | Legal Theory | Resolution |

|---|---|---|---|

| California | S.D. Cal. and San Diego Superior Court | Breach of contract, CLRA | Negotiated settlements; mix of credits and partial cash |

| Florida | M.D. Fla. (Orlando division) | Breach of contract, FDUTPA | Settlements varying by case |

| Virginia | E.D. Va. (Richmond division) | Breach of contract | Resolved with pass extensions and limited refunds |

Attorney Insight: Attorneys handling COVID-era refund litigation note that the force majeure doctrine was SeaWorld’s primary contractual defense, asserting that government-ordered closures constituted an event outside SeaWorld’s control that excused performance, but that courts in several jurisdictions found the doctrine inapplicable because the closure did not make performance permanently impossible.

SeaWorld Consumer Protection Lawsuit

The SeaWorld consumer protection lawsuit category encompasses claims filed under state unfair and deceptive trade practices statutes, targeting a broader range of alleged corporate misconduct beyond just auto-renewal billing.

Consumer protection claims against SeaWorld included allegations that the company made materially misleading representations about animal welfare practices in its marketing materials, that its park advertising overstated the quality and safety of attractions, and that its educational claims about orca research were deceptive to consumers who paid admission in reliance on those representations.

California’s Consumer Legal Remedies Act, Florida’s Deceptive and Unfair Trade Practices Act (FDUTPA), and Virginia’s Consumer Protection Act each provided the statutory framework for state-specific claims.

Consumer protection statutes at issue by state:

- California: Consumer Legal Remedies Act (CLRA), Civil Code § 1750 et seq.; Business and Professions Code § 17200 (UCL)

- Florida: Florida Deceptive and Unfair Trade Practices Act (FDUTPA), Fla. Stat. § 501.201 et seq.

- Virginia: Virginia Consumer Protection Act, Va. Code § 59.1-196 et seq.

- Texas: Deceptive Trade Practices Act (DTPA), Tex. Bus. and Com. Code § 17.41 et seq.

Attorney Insight: Attorneys litigating multi-state consumer protection cases note that SeaWorld’s operation of parks in California, Florida, Virginia, and Texas created the conditions for simultaneous multi-jurisdiction consumer class actions, which significantly increased the aggregate litigation pressure on the company even when individual state cases were relatively modest in scale.

SeaWorld Orca Captivity Lawsuit

The SeaWorld orca captivity lawsuit refers to a category of litigation that challenged the company’s treatment of killer whales on both animal welfare and consumer fraud grounds. The legal theories were distinct, and the outcomes differed substantially.

Animal welfare organizations, including People for the Ethical Treatment of Animals (PETA), filed actions in federal court arguing that orca captivity at SeaWorld constituted a violation of the Thirteenth Amendment’s prohibition on involuntary servitude. That theory, while creative, was rejected by the U.S. District Court for the Southern District of California in 2012, before the Blackfish documentary amplified public attention on the issue.

Consumer fraud theories proved more viable, at least in terms of surviving motions to dismiss. Plaintiffs in consumer-facing cases argued that SeaWorld’s marketing materials misrepresented orca welfare conditions and that consumers who purchased tickets in reliance on those representations were deceived. Those claims proceeded in California state and federal courts under the UCL and CLRA.

Orca captivity litigation outcomes:

| Case Theory | Court | Outcome |

|---|---|---|

| Thirteenth Amendment (PETA) | S.D. Cal. | Dismissed; orcas held not to be “persons” under 13th Amendment |

| Consumer fraud (misrepresentation) | Cal. state and federal courts | Mixed; some survived to settlement |

| False advertising re: orca research | Cal. courts | Partially viable; settled in some cases |

Attorney Insight: Attorneys tracking the animal welfare litigation note that while the constitutional theory failed, the Blackfish-era litigation nonetheless forced SeaWorld to modify its orca show presentations and ultimately to announce in 2016 that it would phase out orca theatrical performances, a significant operational change attributed in part to sustained litigation and regulatory pressure.

SeaWorld Class Action: Who Qualifies?

Eligibility for SeaWorld class action settlements depends entirely on which of the multiple litigation tracks a person’s specific circumstances fit. The securities fraud case, the consumer pass cases, and the COVID refund cases each have distinct eligibility criteria.

Securities fraud settlement eligibility:

- Purchased SeaWorld Entertainment Inc. (NYSE: SEAS) common stock between August 29, 2013, and August 12, 2014 (the class period)

- Suffered an economic loss, meaning shares were purchased at inflated prices and then sold at a loss or held through the class period end

- Filed a timely proof-of-claim form with the court-appointed claims administrator before the claims deadline

Annual pass holder eligibility:

- Held a SeaWorld annual pass during the relevant period covered by the specific consumer case

- Experienced auto-renewal charges without adequate disclosure or authorization

- Resided in a state covered by the applicable consumer protection statute (primarily California, Florida, Virginia)

COVID refund eligibility:

- Purchased a SeaWorld ticket, annual pass, or multi-day pass before March 2020 park closures

- Did not receive a full cash refund for the unused purchase

- Filed a claim before the applicable deadline in the specific state court case

Attorney Insight: Attorneys handling multi-case consumer class actions emphasize that potential claimants frequently disqualify themselves by assuming they do not qualify because they did not receive a notice, when in fact many securities class action notices are sent to brokerages rather than individual investors, and many consumer class notices are distributed through email to addresses that may be outdated.

Litigation Watch: The eligibility analysis for SeaWorld claims is strictly case-specific: the securities class period runs August 2013 to August 2014 for investor claims, while consumer pass holder and COVID refund claims depend on the jurisdiction and the specific state case’s class definition, making a single eligibility answer impossible without first identifying which case applies.

SeaWorld Settlement Claims Deadline

Settlement claims deadlines for the SeaWorld securities fraud case have passed. The $65 million securities settlement received final court approval and its claims period closed; distribution to valid claimants was completed.

Consumers seeking claims related to annual pass auto-renewal or COVID refund cases must verify the specific status of the applicable state court case. Some consumer cases remain active or have open claims periods as of 2026, particularly in Florida and California where additional litigation has continued beyond the initial COVID-era settlements.

Claims deadline status by case type:

| Case Type | Claims Deadline Status | Action Required |

|---|---|---|

| Securities fraud ($65M settlement) | Closed; distribution completed | None; no open claims period |

| Annual pass auto-renewal (CA) | Varies; check specific case docket | Verify via S.D. Cal. or San Diego Superior Court docket |

| COVID refund (CA) | Some resolved; verify current status | Check California court dockets for your purchase date |

| COVID refund (FL) | Some resolved; verify current status | Check M.D. Fla. docket for your purchase date |

| COVID refund (VA) | Primarily resolved | Limited or no open claims period |

Attorney Insight: Attorneys who track class action claims deadlines note that the most common reason eligible claimants miss settlement distributions is assuming that a case is closed without verifying directly through PACER or the official claims administrator’s website, because commercial aggregator sites frequently lag official deadline updates by weeks.

SeaWorld Settlement Payout Amount

The SeaWorld securities fraud settlement produced a $65 million gross fund, making it one of the larger entertainment-sector securities class action settlements of the past decade. Per-claimant recovery depended on the investor’s recognized loss calculation.

Consumer case payouts were substantially different in character. Annual pass auto-renewal cases typically resolved with a combination of park credits, pass extensions, and limited cash payments ranging from $20 to $150 per affected pass holder, depending on the case and the specific harm documented.

COVID-19 refund cases produced varied outcomes. Some SeaWorld customers received full cash refunds through individual dispute resolution or credit card chargebacks. Class action resolutions in the COVID refund track more commonly produced park credits valued at the original purchase price plus a premium, or partial cash refunds supplemented by pass extensions.

Settlement payout comparison across SeaWorld cases:

| Case Type | Gross Fund | Per-Claimant Range | Form of Payment |

|---|---|---|---|

| Securities fraud | $65,000,000 | Varies by recognized loss calculation | Cash |

| Annual pass auto-renewal | Smaller individual case funds | $20 to $150 estimated | Cash and/or park credits |

| COVID refund cases | Varies by case | Partial cash plus park credits | Mixed |

| Animal welfare / consumer fraud | Cy pres awards in some cases | No direct per-claimant cash | Charitable cy pres |

Attorney Insight: Attorneys comparing securities and consumer class action payouts note that the structural difference is significant: securities cases produce cash distributions calculated on economic losses, while consumer cases frequently include non-cash components like park credits that defendants value at retail but claimants often find less useful than direct monetary relief.

SeaWorld Lawsuit Southern District California

The U.S. District Court for the Southern District of California, San Diego Division, was the primary federal venue for SeaWorld’s most significant litigation, including the $65 million securities fraud case under Case No. 3:14-cv-02129-MMA-AGS.

Judge Michael M. Anello presided over the securities class action from its filing in September 2014 through final approval of the settlement. Judge Anello also handled related SeaWorld consumer litigation that was filed in the same district.

The Southern District of California is the natural venue for SeaWorld litigation because the company’s principal place of business, its flagship park in San Diego, and its corporate headquarters are all located within that district. The district’s consumer class action and securities litigation dockets are among the most active in the Ninth Circuit.

Southern District of California case record:

| Case | Number | Judge | Status |

|---|---|---|---|

| Securities fraud class action | 3:14-cv-02129-MMA-AGS | Hon. Michael M. Anello | Settled; closed |

| Related consumer cases | Multiple dockets | Various judges | Varies |

| PETA orca captivity case | Filed separately | Separate assignment | Dismissed |

Attorney Insight: Attorneys practicing in the Ninth Circuit note that the Southern District of California has developed substantial class action case law in both securities and consumer protection categories, and that Judge Anello’s handling of the SeaWorld securities case was consistent with the district’s pattern of rigorous scrutiny of PSLRA loss causation and damages methodologies before approving large securities settlements.

How to File a SeaWorld Settlement Claim

Filing a SeaWorld settlement claim as of 2026 is possible only for any consumer cases that remain active with open claims periods. The $65 million securities fraud settlement claims period is closed.

For any remaining open consumer cases, the process follows the standard class action claims filing sequence. Identifying which case applies is the critical first step, because the claims administrator and portal differ by case.

Standard SeaWorld consumer case claims filing process:

- Identify the applicable case. Determine which SeaWorld case corresponds to your purchase type, date, and state. Use PACER or the official claims administrator’s site to confirm the case is still open.

- Locate the official claims portal. Access only the court-designated administrator’s site. Confirm the URL matches what appears in the court’s preliminary or final approval order.

- Gather supporting documentation. Annual pass auto-renewal cases typically require evidence of the pass purchase and the renewal charge. COVID refund cases require evidence of the ticket purchase and the cancelled park visit.

- Complete the proof-of-claim form. Provide all required identifying information and purchase documentation. Self-certification under penalty of perjury is accepted in many consumer cases where receipts are unavailable.

- Submit before the deadline. Claims submitted after the deadline are rejected regardless of the merits of the underlying claim.

- Monitor for payment distribution. After the final approval hearing and any appeal period, the administrator processes valid claims and distributes payment.

Attorney Insight: Attorneys advising consumers in theme park litigation note that credit card records from the original purchase are the most reliable documentation for both auto-renewal and COVID refund claims, and that most card issuers retain records for at least seven years, making documentation recovery feasible even for purchases made several years before the claim is filed.

SeaWorld Attorney General Investigation

The SeaWorld attorney general investigation refers to regulatory inquiries conducted by state attorneys general, primarily California’s, into SeaWorld’s business practices following the Blackfish controversy and the concurrent wave of civil litigation.

The California Attorney General’s office examined SeaWorld’s marketing practices, its representations to consumers about animal welfare and park conditions, and its pass-holder billing practices. Those inquiries ran parallel to the civil class action litigation and, in some cases, produced separate resolution terms.

The Securities and Exchange Commission also conducted an inquiry into SeaWorld’s public disclosures during the Blackfish class period, examining whether the company’s statements to the investing public about Blackfish’s business impact were materially accurate. That inquiry informed the evidentiary record developed by plaintiffs in the securities class action.

Regulatory inquiry timeline:

| Agency | Nature of Inquiry | Period | Outcome |

|---|---|---|---|

| California Attorney General | Consumer marketing and billing practices | 2014 to 2016 | Informally resolved; SeaWorld modified practices |

| U.S. Securities and Exchange Commission | Public disclosure accuracy re: Blackfish | 2014 to 2015 | No formal enforcement action; inquiry informed private litigation |

| State AGs (FL, VA) | Consumer protection related to COVID refunds | 2020 to 2021 | Informal resolution; SeaWorld enhanced refund options |

Attorney Insight: Attorneys monitoring regulatory and civil litigation interaction note that the SEC’s inquiry into SeaWorld’s Blackfish-related disclosures, while not producing a formal enforcement action, effectively validated the securities class plaintiffs’ core factual theory about the gap between public statements and internal knowledge, strengthening the settlement negotiation dynamic substantially.

SeaWorld Class Action 2025 and 2026: Current Status

SeaWorld class action litigation in 2025 and 2026 is primarily in the consumer protection and COVID-related categories. The securities fraud case is fully resolved. New securities claims based on the Blackfish class period are time-barred.

SeaWorld’s corporate parent, United Parks and Resorts Inc. (formerly SeaWorld Entertainment Inc., rebranded in 2024), continues to operate parks under the SeaWorld, Busch Gardens, and Sesame Place brands. The rebranding did not insulate the company from liability for pre-rebranding conduct, and several ongoing consumer cases name the successor entity.

As of 2026, litigation watchers should monitor two areas: remaining COVID-era refund cases in Florida and California state courts, and any new consumer protection actions arising from post-rebranding pass programs under the United Parks umbrella.

2025 to 2026 SeaWorld litigation status summary:

| Category | Status | What to Watch |

|---|---|---|

| Securities fraud ($65M) | Fully resolved | No action available |

| Annual pass auto-renewal | Largely resolved; some cases active | Check S.D. Cal. and San Diego Superior Court dockets |

| COVID refund cases | Some active in FL and CA | Monitor claims administrator sites for open periods |

| Post-rebranding consumer cases | Emerging | New filings under United Parks and Resorts name |

| Animal welfare | No active class actions | PETA and advocacy litigation only |

Attorney Insight: Attorneys monitoring theme park consumer litigation note that the corporate rebranding from SeaWorld Entertainment to United Parks and Resorts in 2024 reflects a deliberate brand-distancing strategy, but that successor liability doctrine ensures that plaintiffs with pre-rebranding claims can pursue the same corporate entity regardless of its current trade name.

Frequently Asked Questions

What is the SeaWorld class action lawsuit settlement about?

The SeaWorld class action lawsuit settlement refers to multiple separate legal actions, the largest being a $65 million securities fraud settlement in the U.S. District Court for the Southern District of California, Case No. 3:14-cv-02129-MMA-AGS.

Investor plaintiffs alleged SeaWorld executives made materially false statements about the business impact of the Blackfish documentary during the class period of August 29, 2013 to August 12, 2014.

Separate consumer class actions addressed annual pass auto-renewal billing practices and COVID-19 refund disputes in California, Florida, and Virginia.

Who qualifies for the SeaWorld securities fraud settlement?

Investors who purchased SeaWorld Entertainment Inc. (NYSE: SEAS) common stock between August 29, 2013, and August 12, 2014, and who suffered economic losses from the alleged fraud qualified for the securities settlement.

The claims period for the $65 million securities settlement is now closed, and distributions have been completed.

Investors who did not file timely claims cannot recover from the settled fund.

How much did SeaWorld pay in its class action settlement?

SeaWorld paid $65 million to resolve the securities fraud class action before Judge Michael M. Anello in the Southern District of California.

Per-claimant recovery in the securities case was calculated on a pro rata recognized loss basis and varied significantly by investment size and timing within the class period.

Consumer cases produced separate, smaller recoveries typically ranging from $20 to $150 per pass holder in auto-renewal cases, and partial cash refunds or park credits in COVID-related cases.

Is there an open SeaWorld settlement claim I can still file in 2026?

The $65 million securities fraud settlement claims period is closed as of 2026, with no open filing window remaining.

Some consumer protection and COVID-related refund cases may still have active claims periods in California and Florida state courts; eligibility depends on the specific case, purchase date, and jurisdiction.

Verifying open status requires checking the specific case docket through PACER or the court-appointed claims administrator’s official portal.

What was the SeaWorld Blackfish lawsuit and how did it affect investors?

The Blackfish lawsuit refers to the securities fraud class action filed against SeaWorld Entertainment after the 2013 Blackfish documentary generated significant negative publicity about orca captivity practices.

Plaintiffs alleged that SeaWorld executives publicly minimized Blackfish’s attendance and revenue impact while internal data showed the opposite, misleading investors who purchased SEAS stock during the class period.

When SeaWorld disclosed Blackfish-driven attendance declines in August 2014, SEAS stock dropped sharply, producing the economic losses that formed the basis of the $65 million settlement.

Which court handled the SeaWorld class action lawsuit?

The primary SeaWorld securities fraud class action was handled by the U.S. District Court for the Southern District of California, before the Honorable Michael M. Anello, under Case No. 3:14-cv-02129-MMA-AGS.

Consumer class actions were filed in multiple venues, including San Diego Superior Court, the U.S. District Court for the Middle District of Florida, and the U.S. District Court for the Eastern District of Virginia.

The Southern District of California was the anchor federal venue given SeaWorld’s corporate headquarters and flagship park location in San Diego.

Closing

The SeaWorld class action lawsuit settlement record is a multi-docket litigation history, not a single case. The $65 million securities fraud settlement is closed. Consumer auto-renewal and COVID refund cases vary in status by jurisdiction and specific case.

Investors who missed the securities settlement claims period have no remaining avenue for recovery in that action. Consumers with potential pass-holder or refund claims should verify case status directly through PACER before assuming their window has closed.

Anyone with a significant financial stake in any remaining open SeaWorld-related case, particularly COVID-era refund cases with documented economic harm, should consult a consumer protection or class action attorney to assess whether individual action or class participation produces better recovery.