West Capital Lending, the fast-growing Irvine, California mortgage brokerage, is at the center of multiple active lawsuits filed by rival lenders, state regulators, and individual borrowers. The cases involve serious allegations: data theft, employee poaching, unlicensed mortgage activity, and consumer lending violations. A brand-new federal lawsuit filed in March 2026 adds yet another layer to the legal picture surrounding one of the nation’s most controversial mortgage brokerages. Honda Battery Drain Lawsuit

This guide covers every active case, what each lawsuit alleges, how these disputes could affect borrowers, and what to do if you believe West Capital Lending harmed you.

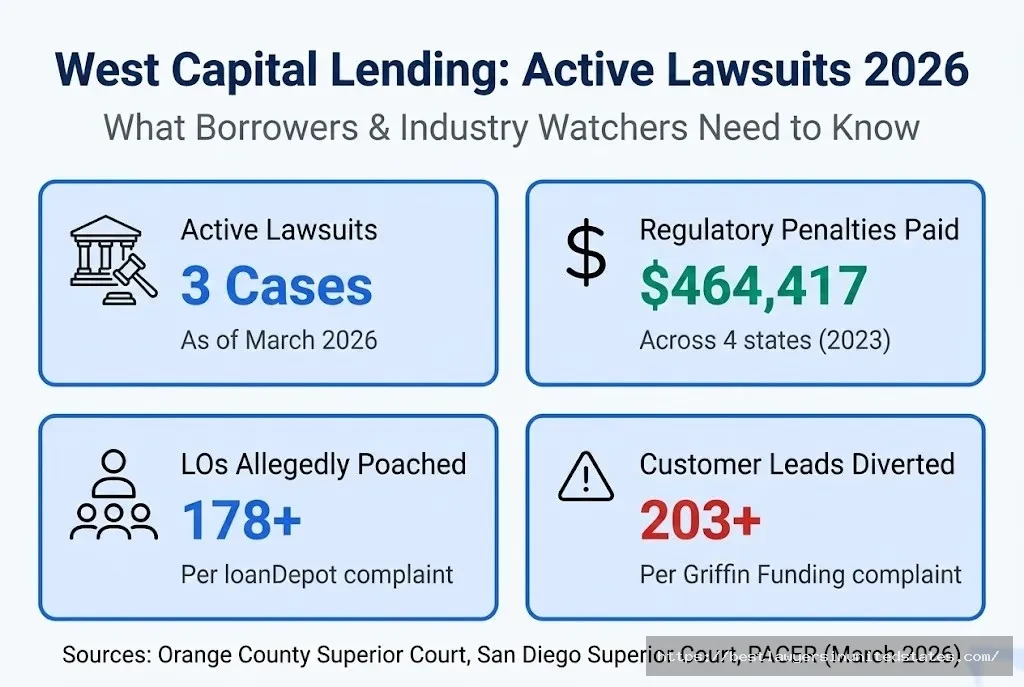

Quick Answer: West Capital Lending faces multiple lawsuits as of March 2026, including a major trade secrets case filed by loanDepot in October 2025 (alleging data theft and poaching of 178 loan officers), a lead diversion lawsuit by Griffin Funding, a new federal case filed March 3, 2026 (Cohen v. West Capital Lending), and past regulatory settlements in four states totaling over $464,000 in penalties. These are not consumer class action settlements — there is no open claim filing deadline for customers to receive settlement money at this time. However, if you were harmed as a borrower, you have legal options.

What Is the West Capital Lending Lawsuit About?

Background: Who Is West Capital Lending?

West Capital Lending (WCL) is an Irvine, California-based direct lender and mortgage brokerage founded in 2016 by Daniel Iskander and Eric Hines. It operates in 43 states plus Washington, D.C. and offers conventional, FHA, VA, jumbo, non-QM, and reverse mortgage products.

By almost any measure, WCL grew at a breakneck pace. Through August 2025, West Capital had originated $3.22 billion across 8,848 loans year to date — nearly matching its entire prior year total. The company’s total mortgage loan originator count surged 37% in 2025 alone, from 769 in January to 1,056 by August.

That explosive growth is part of why the company now faces legal scrutiny from multiple directions. Competitors and regulators allege WCL’s rise was fueled by tactics that crossed legal lines. WCL denies all wrongdoing.

Overview of All Active Lawsuits

| Case | Filed | Court | Filed By | Status |

|---|---|---|---|---|

| loanDepot v. West Capital Lending | October 10, 2025 | Orange County Superior Court, CA | loanDepot | Active/Ongoing |

| Griffin Funding v. West Capital Lending | June 2025 | San Diego Superior Court, CA | Griffin Funding | Active/Ongoing |

| Cohen v. West Capital Lending | March 3, 2026 | U.S. District Court, Central District of CA | Plaintiff Cohen | Active — just filed |

| Oregon ODFR Regulatory Action | 2022–2023 | State regulatory | Oregon DFR | Settled June 2023 |

| Multi-State Regulatory Settlements | 2022–2023 | State regulatory (HI, OR, ID, TX) | State regulators | Settled 2023 |

Lawsuit #1: loanDepot v. West Capital Lending (The Biggest Case)

What loanDepot Is Alleging

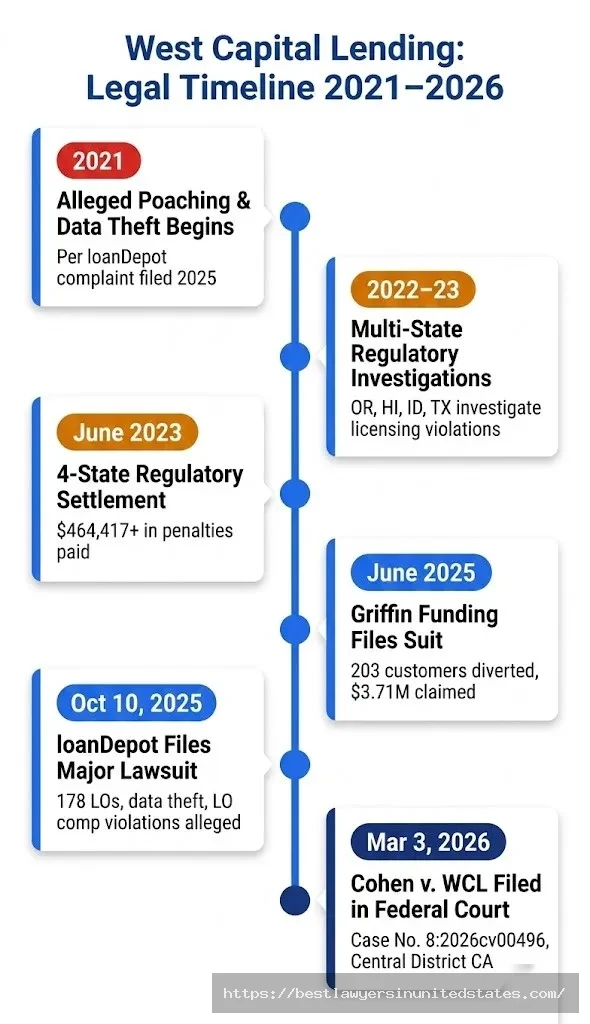

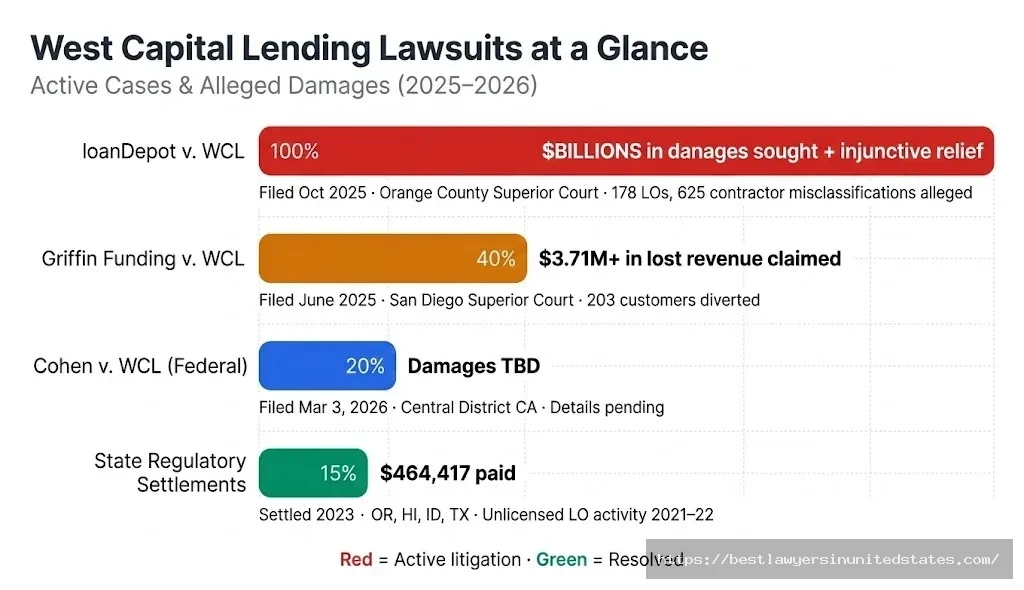

This is the highest-profile and most sweeping case against WCL. The lawsuit, filed on October 10, 2025, in California’s Orange County Superior Court, accuses West Capital of staging a large-scale employee raid and data theft campaign dating back to 2021, and also accuses WCL of improperly hiring loan originators as independent contractors.

The suit’s major claim alleges that WCL misclassified over 600 originators as independent contractors, violating lending laws, skirting taxes, and giving the company a competitive advantage through lower overhead costs.

The lawsuit was filed by the Law Offices of Mary A. Dannelley and names defendants Daniel Iskander, Eric Hines, and others.

The Data Theft Allegation

The data theft claim is one of the most detailed in the complaint. According to loanDepot, a WCL employee contacted the firm around June 2024, indicating that WCL had affiliated with lead generation company “What’s a Mortgage” and obtained customer data taken from loanDepot by two former employees who had joined WCL. Upon loanDepot’s request, WCL agreed to deliver the information on a flash drive in September 2025. LoanDepot said it learned for the first time that the drive included 10 different lists containing not only customer names and contact information but also FICO scores, loan numbers and loan-level details.

LoanDepot further alleged that WCL repeatedly refused to cooperate in confirming the complete return and remediation of that data from its systems and devices.

The Employee Poaching Allegation

LoanDepot estimates 178 of its loan originators were solicited and hired by WCL, with the belief that they would “enjoy higher after-tax earnings as a 1099 independent contractor than as a W2 employee.”

The lawsuit also describes a specific scheme: WCL allegedly poached LoanDepot originators who had active pending loans, quickly closed those loans at WCL, then obscured the diversion by having a different LO sign off on the transactions.

The LO Compensation Violation Allegation

LoanDepot also claims WCL compensates LOs under a plan offering a “lucrative split” of loan revenue — typically 10% to 15% — which violates LO compensation rules and creates “a perverse incentive for LOs not to provide the best terms to a consumer in order to increase their own compensation.”

This allegation, if proven, would be directly relevant to borrowers. LO compensation rules under federal Regulation Z exist specifically to protect borrowers from being steered into higher-cost loans.

Key Allegations: loanDepot v. WCL

| Allegation | Specific Claim | Applicable Law |

|---|---|---|

| Data theft | Stolen customer lists with FICO scores, loan details | Trade secrets laws, GLBA |

| Employee poaching | 178 LOs recruited away with active leads | Contract law, unfair competition |

| LO misclassification | 625+ originators treated as 1099 contractors | California labor law, federal lending law |

| Illegal LO compensation | 10–15% revenue splits to LOs | Regulation Z (LO Comp Rule) |

| Lead diversion | Active loans diverted and closed at WCL | Trade secrets, tortious interference |

What WCL Says

Daniel Iskander, co-founder of West Capital Lending, called the lawsuit baseless. “Anyone can sue anyone for any reason,” Iskander said. “This isn’t the first time a competitor has tried to sue us for losing loan officers to the broker channel. We operate within all state and federal laws and, most importantly, with integrity for our loan officers and our borrowers. There’s absolutely no validity to any type of corporate theft in any way, shape, or form. The only validity to the entire complaint by loanDepot is that West Capital Lending is a top brokerage. Period.”

Lawsuit #2: Griffin Funding v. West Capital Lending

Overview

A second major industry lawsuit came just months before the loanDepot filing. In June 2025, consumer-direct lender Griffin Funding filed a complaint in the Superior Court of California, County of San Diego, against former employees who left the company in 2024 and 2025 to join WCL. The suit alleges that these former employees diverted leads and customers belonging to Griffin Funding.

How the Alleged Scheme Worked

According to the complaint, Griffin invests millions of dollars annually to generate exclusive leads through its website. To protect that investment, the company’s employment agreements prohibit LOs from copying or soliciting these leads for up to 36 months after leaving the company. Griffin believes former employees “have stolen lists of leads provided to them while employed with plaintiff” because they “intend to continue to solicit and are actively soliciting business from those leads.”

In total, the defendants have diverted at least 203 customers, causing damages in excess of $3.71 million in lost revenue, the lawsuit states. Griffin’s lawsuit alleges breach of contract, conversion, misappropriation of trade secrets and unfair competition.

WCL’s Response to Griffin

WCL founder Daniel Iskander used nearly identical language in response to Griffin’s suit as he did with loanDepot: “Anyone can sue anyone for any reason. This isn’t the first time a competitor has tried to sue us for losing loan officers to the broker channel.”

What Industry Attorneys Say

Industry attorneys note the lawsuits highlight persistent tension between corporate ownership of client data and the personal connections loan officers build with borrowers. Troy Garris, co-managing partner at Garris Horn LLP, explained: “If the LO has nonpublic personal information about a customer the company did business with, it belongs to the company.” But Garris also acknowledged that LOs control much of the business because of their personal relationships with borrowers, and “every mortgage company out there, every day they’re hiring, they’re running the risk that somebody is bringing somebody else’s information into them.”

Lawsuit #3: Cohen v. West Capital Lending (New Federal Case, 2026)

What We Know

A new federal case, Cohen v. West Capital Lending, Inc. (Case No. 8:26-cv-00496), was filed on March 3, 2026 in the U.S. District Court for the Central District of California. The docket was last retrieved on March 3, 2026, and full case details require PACER access.

The nature of this lawsuit — whether it’s a consumer complaint, a former employee dispute, or another type of claim — has not yet been publicly reported in detail. Given the pattern of litigation WCL faces, this case bears monitoring closely.

| Detail | Information |

|---|---|

| Case Name | Cohen v. West Capital Lending, Inc. |

| Case Number | 8:2026cv00496 |

| Court | U.S. District Court, Central District of California |

| Filed | March 3, 2026 |

| Status | Active — early stage |

Regulatory Settlements: State Actions Against WCL

The Four-State Settlement (2023)

Before the current wave of private lawsuits, WCL already faced regulatory enforcement. In 2023, WCL entered into settlement agreements and consent orders with the states of Hawaii, Oregon, Idaho, and Texas related to unlicensed activity in 2021 and 2022. The company agreed to pay more than $464,000 in administrative penalties.

Under the terms of the Oregon settlement, West Capital Lending agreed to pay $464,417.50 in administrative penalties and to implement a number of reforms to its lending practices.

| State | Issue | Settlement Year | Penalty |

|---|---|---|---|

| Oregon | Unlicensed mortgage activity | June 2023 | $464,417.50 (combined) |

| Hawaii | Unlicensed mortgage activity | 2023 | Part of combined settlement |

| Idaho | Unlicensed mortgage activity | 2023 | Part of combined settlement |

| Texas | Unlicensed mortgage activity | 2023 | Part of combined settlement |

These settlements required WCL to admit no wrongdoing but to pay penalties and reform its practices — a standard outcome in state regulatory enforcement actions.

Consumer Complaints: What Borrowers Are Reporting

BBB and Consumer Affairs Complaints

Beyond the corporate lawsuits, WCL faces a pattern of consumer-level complaints worth knowing about before you work with this lender.

The Consumer Financial Protection Bureau (CFPB) received a mortgage-related complaint about West Capital Lending in 2024 involving closing on a VA mortgage. WCL provided a response and the complaint was closed.

On the Better Business Bureau and ConsumerAffairs platforms, borrower complaints describe several recurring issues:

- Bait-and-switch on loan terms — Loan terms changing significantly at or near closing

- Escrow omissions — Borrowers reporting agreed escrow arrangements dropped without clear notification

- Unsolicited marketing calls — Aggressive outreach to consumers who hadn’t contacted WCL

- Failure to deliver on rate promises — Rates or terms verbally promised but not honored in final loan documents

One ConsumerAffairs reviewer described the experience: “I was using a different broker to begin with but West Capital called me and offered me a better deal. All the things that they did say were a lie and they changed them all right at the last minute at closing.”

WCL has responded to many BBB complaints by placing complainants on do-not-call lists and noting they “take compliance very seriously.”

How the LO Compensation Allegations Affect Borrowers

This section matters specifically if you got a mortgage through WCL.

Under federal Regulation Z’s LO Compensation Rule, loan officers cannot be paid based on the interest rate or terms of a loan — the whole point is to prevent LOs from steering borrowers into higher-cost products to earn a bigger commission.

LoanDepot’s lawsuit alleges WCL paid LOs 10–15% revenue splits on loan proceeds — a structure loanDepot claims violates this rule. If that’s true, some WCL borrowers may have been steered into loans with higher rates or fees than they should have received.

This is still an allegation that hasn’t been proven in court. But if you financed through WCL and felt your rate seemed higher than quotes you received elsewhere, it’s worth getting a second opinion. What Proof Do You Need for a Roundup Lawsuit

Timeline of Key Legal Events

| Date | Event | Details |

|---|---|---|

| 2016 | WCL founded | Co-founded by Daniel Iskander and Eric Hines in Irvine, CA |

| 2021 | Alleged unlicensed activity begins | Per state regulators in OR, HI, ID, TX |

| 2021 | Alleged data/employee poaching begins | Per loanDepot lawsuit |

| 2022 | State regulatory investigations open | Multiple states investigating licensing violations |

| June 2023 | Multi-state regulatory settlement | WCL pays $464,417.50+ in penalties across 4 states |

| June 2024 | loanDepot discovers data theft | WCL employee tips off loanDepot about stolen data |

| 2024–2025 | Griffin Funding LOs depart to WCL | At least 3 LOs allegedly take leads |

| September 2025 | Flash drive returned | WCL returns thumb drive of data to loanDepot |

| October 10, 2025 | loanDepot files lawsuit | Orange County Superior Court; trade secrets, data theft, LO poaching |

| June 2025 | Griffin Funding files lawsuit | San Diego Superior Court; lead diversion, $3.71M+ claimed damages |

| March 3, 2026 | Cohen v. WCL filed | Federal court, Central District of California |

| 2026 (ongoing) | All three cases in active litigation | No settlements announced as of March 2026 |

What This Means for Current and Former WCL Borrowers

There is no open consumer class action settlement against West Capital Lending as of March 2026. No claim filing deadline exists, and no settlement fund has been established for borrowers.

However, if you believe you were harmed by WCL’s lending practices, here are your actual options:

Option 1: File a CFPB Complaint

The Consumer Financial Protection Bureau handles complaints against mortgage lenders. You can file at consumerfinance.gov/complaint. The CFPB forwards complaints to the company and monitors patterns across many borrowers.

Option 2: Contact Your State Regulator

Each state has a Division of Financial Regulation or equivalent agency that licenses mortgage companies and investigates violations. Because WCL already settled with four states, regulators in those states and others are familiar with the company.

Option 3: Consult a Consumer Protection Attorney

If you believe you were steered into a higher-rate loan, experienced a bait-and-switch at closing, or suffered damages from WCL’s lending practices, a consumer protection or mortgage fraud attorney can evaluate whether you have a private claim. Many offer free initial consultations.

Option 4: BBB Complaint

While the BBB cannot force resolution, a formal complaint creates a public record and sometimes prompts companies to resolve legitimate grievances.

Do You Need an Attorney?

For most standard complaints (unwanted calls, minor disclosures issues), you don’t need an attorney — a CFPB or state complaint may be sufficient.

You should consider consulting an attorney if:

- Your loan terms changed significantly at closing compared to what was verbally promised

- You believe your LO steered you into a higher-rate product

- You suffered measurable financial harm (e.g., higher rate costing you thousands annually)

- You signed documents under time pressure or without adequate disclosure

How West Capital Lending Compares in Industry Litigation

The type of lawsuit WCL faces — competitor suing over employee poaching and data theft — is not unusual in the mortgage industry. However, the scale and number of simultaneous active cases is notable.

| Company | Lawsuit Filed Against | Allegation | Status |

|---|---|---|---|

| West Capital Lending | By loanDepot | Data theft, 178 LO poaching, LO comp violations | Active (Oct 2025) |

| West Capital Lending | By Griffin Funding | 203 customer lead diversion, $3.71M damages | Active (June 2025) |

| CrossCountry Mortgage | By loanDepot | LO recruitment coordination | Preliminary ruling vs CCM |

| Movement Mortgage | By loanDepot | Mass employee defection/poaching | Dismissed by loanDepot |

| West Capital Lending | By state regulators (OR, HI, ID, TX) | Unlicensed activity | Settled 2023, $464K+ |

LoanDepot has previously been involved in similar litigation. The lender filed a lawsuit against Movement Mortgage alleging the rival firm had “poached” employees — a dispute later dropped when loanDepot dismissed the case after months of legal maneuvering. LoanDepot also secured a preliminary ruling in a separate lawsuit against CrossCountry Mortgage, where a judge found sufficient evidence of potential coordination in employee recruitment efforts.

What makes the WCL case different is the combination of alleged data theft (actual customer records with FICO scores and loan details), LO compensation rule violations that directly affected borrowers, and prior state regulatory settlements establishing a pattern of compliance issues.

Frequently Asked Questions

Is there a West Capital Lending class action lawsuit I can join?

As of March 2026, there is no open consumer class action settlement for West Capital Lending borrowers to join or file claims in. The active lawsuits are competitor-versus-WCL business disputes (loanDepot, Griffin Funding) and the newly filed Cohen federal case. If a consumer class action develops, this article will be updated.

What was the West Capital Lending settlement?

In 2023, WCL settled regulatory actions with four states — Oregon, Hawaii, Idaho, and Texas — over unlicensed mortgage originator activity in 2021–2022. The total penalty was over $464,000. This was a regulatory enforcement settlement, not a consumer compensation fund.

Did loanDepot win its lawsuit against West Capital Lending?

No. The loanDepot lawsuit was filed in October 2025 and is in active litigation as of March 2026. No verdict, judgment, or settlement has been announced. Court cases of this complexity typically take 1–3 years to resolve.

What did West Capital Lending allegedly do wrong?

According to the lawsuits, WCL is accused of: stealing customer data lists from rival lenders, poaching over 175 loan officers from competitors, misclassifying 625+ LOs as independent contractors, paying LO compensation structures that violated federal rules, and diverting borrower leads from former employers.

Can West Capital Lending still originate loans?

Yes. WCL continues to operate as an active mortgage broker and direct lender in 43 states. The lawsuits are civil disputes, and no regulatory order has suspended its license as of March 2026.

What is Cohen v. West Capital Lending?

This is a new federal lawsuit filed March 3, 2026 in the U.S. District Court for the Central District of California (Case No. 8:2026cv00496). Full details about the plaintiff’s claims are not yet publicly available.

Were WCL borrowers harmed by the alleged LO compensation violations?

LoanDepot alleges that WCL’s practice of paying LOs 10–15% revenue splits created an incentive for LOs to push borrowers into higher-cost loans. If proven, that would mean some borrowers paid higher rates than they should have. This has not yet been proven in court.

How many loan officers did West Capital Lending allegedly poach?

LoanDepot alleges 178 of its loan originators were recruited to WCL. Griffin Funding alleges multiple former employees took leads and customers after joining WCL.

What states did West Capital Lending settle with regulators?

Oregon, Hawaii, Idaho, and Texas — all related to unlicensed mortgage originator activity occurring in 2021 and 2022. The settlements were reached in 2023.

How do I file a complaint against West Capital Lending?

You can file a complaint with the CFPB at consumerfinance.gov/complaint, with your state’s financial regulator, or with the Better Business Bureau. For significant financial harm, consult a consumer protection attorney.

What is West Capital Lending’s BBB rating?

West Capital Lending has a “B-” rating with the Better Business Bureau. Consumer reviews are mixed — some borrowers report excellent service while others describe term changes at closing and communication issues. Affordable Dentures Lawsuit

Is my personal data safe if I applied with WCL?

LoanDepot’s lawsuit alleges WCL possessed stolen customer data including FICO scores, loan numbers, and personal contact information from loanDepot’s systems. If you were a loanDepot customer whose former LO moved to WCL, there’s a possibility your data was among the information on the flash drive at the center of the lawsuit. The lawsuit does not allege WCL misused borrower data against the borrowers themselves.

What should I do if my loan terms changed at closing with WCL?

Document everything — save all communications, rate lock agreements, loan estimates, and closing disclosures. Compare your initial Loan Estimate with your final Closing Disclosure. If there are material differences that weren’t properly disclosed, file a CFPB complaint and consider consulting a consumer protection attorney.

Did West Capital Lending admit wrongdoing in the state settlements?

No. As with most regulatory settlements, WCL denied the allegations while agreeing to pay penalties and implement reforms. This is standard practice in regulatory enforcement outcomes.

How fast is West Capital Lending growing despite the lawsuits?

Rapidly. Through August 2025, WCL had originated $3.22 billion across 8,848 loans year to date, and its total LO count surged 37% year to date — from 769 in January to 1,056 by August 2025. The company also signed a new lease for 44,241 square feet in Irvine — nearly four times its previous office space.

Where is the WCL vs. loanDepot case being heard?

The loanDepot lawsuit is filed in California Superior Court for Orange County. LoanDepot is seeking injunctive relief and monetary damages, alleging violations of federal labor, LO compensation, and consumer privacy laws.

What is “LO misclassification” and why does it matter?

Misclassification means treating workers as independent contractors (1099) when they should legally be employees (W-2). For mortgage LOs, misclassification matters because: employees are protected by federal LO compensation rules, independent contractors are not. LoanDepot alleges WCL misclassified 625+ LOs specifically to avoid these federal protections and lower overhead costs, which it claims created an illegal competitive advantage.

Will there ever be a consumer settlement?

Possibly. If loanDepot’s case results in a large judgment, WCL could face financial pressure that leads to settlement activity. If the Cohen federal case turns out to be a consumer complaint, it could potentially become a class action. Neither outcome is certain or imminent. Check back for updates as these cases develop.

Latest Updates: March 2026

- Cohen v. West Capital Lending filed March 3, 2026 — A new federal case has been added to WCL’s growing legal docket. Details are limited but the case is active in the Central District of California.

- LoanDepot and Griffin Funding cases ongoing — Both cases filed in 2025 are in active litigation. No settlement negotiations have been publicly reported.

- WCL continues to expand — Despite the lawsuits, WCL is growing its LO count and office space, suggesting no operational slowdown.

- No consumer settlement fund — As of this writing, no settlement has been reached in any case that would entitle borrowers to file claims for compensation.

Summary: What You Need to Know About the West Capital Lending Lawsuit

The West Capital Lending legal situation in 2026 is complex — multiple cases, multiple accusers, and no consumer settlement to speak of. Here’s the bottom line:

If you’re a current or prospective WCL borrower, the lawsuits signal that you should read your loan documents carefully, keep records of every verbal promise made, and compare your Loan Estimate to your Closing Disclosure line by line.

If you’re a former WCL borrower who believes you were harmed, your best path is a CFPB complaint, a state regulator complaint, or a free consultation with a consumer protection attorney. There is no class action claims process open right now.

If you’re following these cases as a mortgage industry observer, the loanDepot lawsuit is the most consequential — its allegations about LO compensation structures and data theft, if proven, could reshape how regulators scrutinize high-growth brokerages going forward.