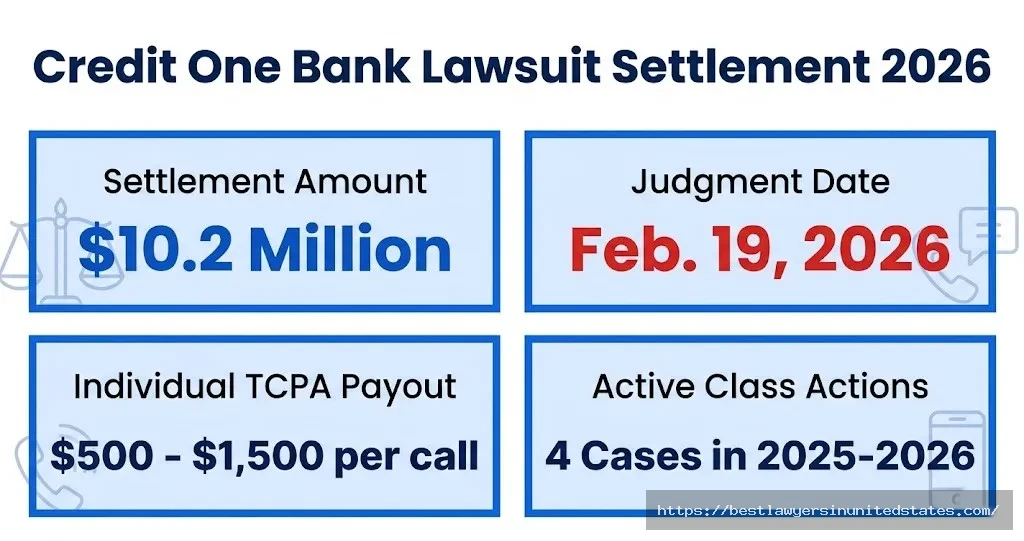

Credit One Bank was ordered to pay $10.2 million in a landmark judgment entered on February 19, 2026, resolving a five-year civil enforcement action over harassing debt collection calls. This is the most significant confirmed credit one bank lawsuit settlement to date, and millions of consumers across California may be directly affected.

There is also a separate active class action lawsuit filed in August 2025, plus ongoing allegations tied to illegal express payment fees and credit reporting errors. This guide covers every confirmed case, separates fact from viral misinformation, and tells you exactly what to do if you think you have a claim.

By the time you finish reading, you will know which lawsuit applies to you, whether you qualify, and what your next steps are in 2026. Lizzo Lawsuit 2026

Credit One Bank Lawsuit Settlement: What You Need to Know Right Now

Credit One Bank will pay $10.2 million to resolve a civil lawsuit filed by the District Attorneys’ Offices of Los Angeles, Riverside, San Diego, and Santa Clara counties, which alleged the company made repeated, intrusive, and harassing debt collection calls to consumers.

This is not a rumor. This is a signed court judgment. The money is real.

The judgment was entered on February 19, 2026, in Riverside County Superior Court and signed by Judge Harold Hopp. The court did not just hand Credit One a fine. It required the bank to overhaul its entire debt collection operation.

There are also multiple other lawsuits involving Credit One: a pending class action over robocalls, a lawsuit over illegal express payment fees, and FCRA-related credit reporting claims. Each one covers different consumers with different eligibility rules.

| Settlement Type | Amount | Status | Who It Affects |

|---|---|---|---|

| California DA Civil Judgment | $10.2 million | Final as of Feb. 19, 2026 | California consumers; no individual claims |

| TCPA Robocall Class Action (Mingura) | Pending | Active, filed Aug. 2025 | Nationwide; claims open eventually |

| Express Payment Fee (TILA) | $5M+ estimated | Resolved late 2025 | Credit One cardholders charged $9.95 fee |

| FCRA Credit Reporting | Varies | Ongoing | Consumers with inaccurate credit data |

Key Takeaway: There is not one Credit One Bank lawsuit settlement. There are at least four distinct legal actions, and you may qualify for more than one.

Credit One Bank Lawsuit Settlement Details: The Full Story

The confirmed settlement details come directly from official court filings and district attorney announcements. Not from Reddit. Not from anonymous websites.

Case number CVRI2101654 was filed in Riverside Superior Court. The People’s consumer protection action asserts Credit One and its agents engaged in unlawful debt collection activities, including calls made with unreasonable and excessive frequency and calls made even after consumers requested they stop or when Credit One called the wrong number.

Credit One had a policy allowing its vendors to make eight calls per day, plus an additional two calls per day under certain circumstances on overdue credit card accounts, and the calls could be placed on consecutive days.

That is ten calls to one person in a single day. Every day. Repeatedly.

Under the terms of the judgment, Credit One was ordered to pay a total of $10.2 million, including $9 million in civil penalties and $1.2 million in investigative costs. Credit One did not admit wrongdoing.

| Case Detail | Information |

|---|---|

| Case Number | CVRI2101654 |

| Court | Riverside County Superior Court |

| Judge | Harold Hopp |

| Judgment Date | February 19, 2026 |

| Total Settlement | $10.2 million |

| Civil Penalties | $9 million |

| Investigative Costs | $1.2 million |

| Admission of Wrongdoing | None |

Key Takeaway: The $10.2M settlement is fully confirmed, court-signed, and publicly announced by four county district attorneys.

Credit One Class Action Lawsuit Settlement: Confirmed vs. Unconfirmed

This is where consumers need to pay close attention. There is a lot of misinformation circulating online about a separate Credit One Bank class action settlement worth $14 million.

A number of outlets reported Credit One had settled a TCPA class action for $14 million. The problem is that none of these articles cite the court or case number. Legal professionals who checked the dockets found no evidence the settlement exists. The articles appear to be confusing a different settlement and citing back to a Reddit article as their source.

Think of it like a game of telephone. One site published it. Dozens copied it. Now it reads like fact.

The confirmed class action is a separate matter entirely. Plaintiff Rebeca Mingura filed the Credit One Bank class action lawsuit on August 8, 2025, in California federal court, alleging violations of the Telephone Consumer Protection Act (TCPA), the Rosenthal Fair Debt Collection Practices Act, and California’s Unfair Competition Law.

That case, Mingura v. Credit One Bank N.A., Case No. 4:25-cv-06712, is still pending as of March 2026. It has not settled. No payout amounts exist for it yet.

- Confirmed: $10.2M civil judgment by California DAs (February 19, 2026)

- Active, pending: Mingura class action, Case No. 4:25-cv-06712 (filed August 2025)

- Unverified: $14M TCPA class action widely reported online; no court record found

Credit One Bank Settlement 2026: Latest News and Updates

The biggest development of 2026 came on February 20, 2026, when four California county district attorneys jointly announced the $10.2 million judgment.

Credit One Bank agreed to the settlement after almost five years of litigation. The Nevada-based bank stated it agreed to settle “solely to avoid the cost and inconvenience of further litigation.”

This is Credit One’s second loss to California law enforcement. A federal jury had previously found Credit One liable in 2019 for violating the Rosenthal Act. Despite that verdict, Credit One allegedly continued the same practices.

The 2026 settlement is the fourth judgment obtained by the California Debt Collection Task Force, which previously secured judgments against Allied Interstate in 2018, Synchrony Bank in 2021, and Capital One Bank in 2022.

Meanwhile, Credit One faces a new active threat. Mingura alleges she received more than 578 calls from Credit One Bank between April and July 2025, even after she had informed the bank that she was a disabled senior citizen experiencing financial and medical difficulties. She hired legal counsel, who sent a formal cease-and-desist letter in July 2025. The bank allegedly continued to contact her anyway.

Key Takeaway: Credit One has now been found liable for the same type of phone harassment twice. The 2026 settlement did not end the bank’s legal troubles.

Credit One Bank Settlement Eligibility: Do You Qualify?

Eligibility depends entirely on which lawsuit or settlement you are asking about. There is no single eligibility test that covers every Credit One case.

For the confirmed $10.2M California civil judgment, this was a state enforcement action. It is not a traditional class action lawsuit allowing direct consumer claims. Instead, it imposes penalties and requires compliance reforms. The funds go to the state, not to individual consumers.

For the TCPA claims tied to robocalls, individual consumers can pursue their own claims independently. Under federal law, TCPA statutory damages are $500 per violation, and up to $1,500 per violation if the violation was willful.

For the Mingura class action (Case No. 4:25-cv-06712), the case is still in early stages. If it certifies as a class action and reaches settlement, affected consumers will be notified.

| Lawsuit | Can You File an Individual Claim Now? | Who Is Covered |

|---|---|---|

| $10.2M CA Civil Judgment | No, funds go to state | CA residents; compliance-focused |

| Mingura Class Action | Not yet; case is pending | Those who received harassing calls |

| TCPA Individual Claims | Yes, through your own attorney | Anyone called without consent |

| Express Fee Lawsuit | Class resolution in late 2025 | Cardholders charged the $9.95 fee |

Credit One Bank Settlement: Who Qualifies and Who Does Not

The key to qualifying is matching your experience to the specific lawsuit type. Here is a practical breakdown.

You likely qualify for individual TCPA action if:

- You received automated or prerecorded calls from Credit One Bank

- You did not give written consent to be called via automated systems

- Calls continued after you told them to stop

- You were called at a number that was not associated with any Credit One account

You may qualify for the Mingura class action if:

- You are a Credit One cardholder or former cardholder

- You received multiple calls per day from the bank or its vendors

- Calls persisted after a formal cease-and-desist

- You are in California or received calls targeting a California phone number

You do not qualify if:

- You gave written express consent to automated calls and never revoked it

- You have no record of any contact from Credit One Bank

- You already filed an individual TCPA lawsuit against Credit One

For the express payment fee class action, plaintiffs Anthony Waldon and Jason Goldstein alleged they were both charged fees by Credit One for making “express payments” online, despite the payments being processed by an automated system rather than a live representative. That settlement reached final approval in late 2025. Eligible cardholders may have already received automatic account credits or checks.

Credit One Bank Settlement Amount: How Much Money Is Involved?

The total confirmed financial exposure across all Credit One legal actions is substantial.

The California DA settlement totals $10.2 million: $9 million in civil penalties and $1.2 million in investigative costs. That money goes to the state, not directly to consumers.

Under the TILA express fee settlement, internal records revealed the bank earned over $5 million annually through automated express payment fees. Final approval was granted in late 2025, with eligible class members beginning to receive automatic account credits or checks in January and February 2026.

For individual TCPA claims, the law sets fixed damage amounts. No settlement fund is required. An individual claimant proving even 10 unauthorized automated calls at $1,500 per willful violation could recover $15,000 independently.

| Case | Total Amount | Goes To |

|---|---|---|

| California DA judgment | $10.2 million | State penalties and investigative costs |

| Express fee class action | Approx. $5M+ fund | Cardholders charged $9.95 fee |

| Individual TCPA claims | $500 to $1,500 per call | Individual consumer |

| Mingura class action | TBD | Nationwide class members (pending) |

Key Takeaway: The largest confirmed dollar amount is the $10.2M state judgment. Individual TCPA claims can pay $500 to $1,500 per unauthorized call and are available to pursue right now.

Credit One Bank Settlement: How Much Will You Get?

This depends on which legal path you take and which settlement applies to you.

From the California DA judgment: nothing directly. Funds went to the state of California as civil penalties.

From the express payment fee settlement: if you were a Credit One cardholder charged the $9.95 express payment fee, you may have already received an automatic credit or check. In January and February 2026, eligible class members began receiving automatic account credits or checks.

From individual TCPA claims: up to $500 per unauthorized call, or $1,500 per call if you can show the violation was willful. A consumer who received 578 calls the way Mingura allegedly did could theoretically recover hundreds of thousands of dollars individually.

From the Mingura class action, if it settles: historical TCPA class settlements typically pay between $50 and $500 per person depending on class size. Smaller class participation means higher individual payouts.

- Express fee claimants: Check your mailbox or account credit from January-February 2026

- TCPA individual claimants: $500 to $1,500 per call, via your own attorney

- Mingura class members: No payments yet; case is still active

Credit One Bank Settlement Payout Date: When Will Payments Be Sent?

Payout timing depends entirely on which action you are part of.

For the express payment fee settlement, final approval was granted in late 2025, and in January and February 2026, eligible class members began receiving automatic account credits or checks. If you were eligible for that one, payments may already be in transit.

For the California civil judgment, no individual payout timeline exists for consumers. That money was paid directly to county DA offices and state enforcement funds.

For the Mingura class action (Case No. 4:25-cv-06712), there is no payment timeline yet. The case was filed in August 2025 and is in active litigation as of March 2026. Class certification has not been granted. Settlement could be years away.

| Settlement | Payout Status as of March 2026 |

|---|---|

| Express fee class action | Begun distributing Jan-Feb 2026 |

| California DA judgment | No consumer payouts; state funds only |

| Mingura class action | No timeline; case pending |

| Individual TCPA claims | After your case resolves; varies |

Key Takeaway: The only settlement where consumers may already have money is the express fee class action. Every other track requires more waiting or active legal participation.

Credit One Bank Settlement Claim Form: How to File Step by Step

The right filing steps depend on which settlement applies to your situation.

If you were charged the $9.95 express payment fee: The express fee settlement received final approval in late 2025. Class members should have received notice by mail or email. If you believe you were a class member and did not receive notice, contact Credit One’s settlement administrator directly.

If you received unauthorized automated calls from Credit One: You can file an individual TCPA complaint right now. Here is how:

- Document every call: write down dates, times, phone number, whether the call was automated or prerecorded

- File a complaint with the FCC at fcc.gov and the CFPB at consumerfinance.gov

- Contact a consumer protection attorney who handles TCPA cases. Many work on contingency with no upfront cost.

- If you are in California, the Rosenthal Act offers additional state protections on top of federal TCPA rights.

If you want to join the Mingura class action: The case is pending in the U.S. District Court for the Northern District of California as Case No. 4:25-cv-06712. Follow updates through PACER or sites like Top Class Actions. Once a class is certified, affected consumers will be notified automatically if records show they were called.

Key Takeaway: Filing a claim is not the same for every Credit One lawsuit. Identify which one applies to you first, then take the action that matches it. General Motors V8 Engine Lawsuit

Credit One Bank TCPA Settlement: The Robocall Allegations Explained

The Telephone Consumer Protection Act is the federal law that makes unauthorized robocalls illegal. It is also the law at the center of most Credit One lawsuits.

The TCPA, enacted in 1991, requires businesses to have prior express written consent before using an automated telephone dialing system or prerecorded message to call a consumer’s cell phone. No consent. No call. Simple as that.

The Credit One Bank class action filed in August 2025 alleges violations of the TCPA, the Rosenthal Fair Debt Collection Practices Act, and California’s Unfair Competition Law. The bank allegedly used automated systems to call a consumer’s phone even after consent was revoked.

Under the TCPA:

- $500 per call in statutory damages for violations

- $1,500 per call if the violation is proven willful

- No proof of actual harm needed; the unauthorized call itself is the violation

- Non-customers can qualify if their number was called without consent

The widely reported “$14 million TCPA class action settlement” appears to be unverified. Legal professionals who checked court dockets found no supporting case number or record for this settlement as of early 2026. Do not submit a claim on any website that cannot provide a verified case number for that specific settlement.

Credit One Bank Harassing Phone Calls Lawsuit: The Full History

Credit One’s pattern of phone harassment goes back further than most people realize. This is not a first offense. It is not even a second offense.

Credit One had previously been found liable by a federal jury in 2019 for violating the Rosenthal Act. Despite that verdict, Credit One allegedly continued the same practices.

Then in March 2021, the California Debt Collection Task Force filed its civil enforcement action. That case ran for nearly five years before the February 2026 judgment. Four separate county district attorneys collaborated on the prosecution.

By 2025, a new plaintiff, Rebeca Mingura, alleged she received more than 578 calls between April and July 2025. Even after her attorney sent a formal cease-and-desist letter in July 2025, the calls continued.

This is a pattern that spans more than six years:

| Year | Event |

|---|---|

| 2019 | Federal jury finds Credit One liable under Rosenthal Act |

| March 2021 | California DAs file civil enforcement (CVRI2101654) |

| April-July 2025 | Mingura receives 578+ calls; cease-and-desist ignored |

| August 2025 | Mingura class action filed (Case No. 4:25-cv-06712) |

| February 19, 2026 | $10.2M judgment entered; compliance reforms ordered |

Key Takeaway: Credit One Bank has been flagged, found liable, and sued multiple times for the same conduct. The 2026 judgment is the fourth victory against a debt collector by the California task force.

Credit One Bank Express Payment Fee Lawsuit: What Cardholders Claimed

The express payment fee lawsuit targeted a different type of consumer harm: a deceptive $9.95 fee charged for paying your credit card bill.

Plaintiffs Anthony Waldon of New York and Jason Goldstein of Florida both claimed they were charged fees by Credit One for making “express payments” online, even though the payments were seemingly processed by the company’s automated system. The fee was $9.95 per express payment. Plaintiffs estimated that Credit One earned more than $5 million through these fees.

The legal issue ties to the Truth in Lending Act. TILA prohibits creditors from charging a fee for expedited service unless an actual live representative handles the payment. Credit One’s “express” option allegedly used an automated chatbot, not a live person. Yet the bank charged the premium fee anyway.

The settlement received final approval in late 2025. Beginning in January and February 2026, eligible class members began receiving automatic account credits or checks.

- Case Number: 7:20-cv-10003

- Court: U.S. District Court, Southern District of New York

- Fee Amount: $9.95 per express payment

- Total Earned by Credit One: $5M+ estimated

- Settlement Status: Final; payouts began January-February 2026

If you paid this fee between 2018 and 2020 and never received a settlement notice, contact the case administrator through the Southern District of New York’s official court filing system.

Credit One Bank FCRA Settlement: Credit Reporting Violations Explained

The Fair Credit Reporting Act requires lenders to report accurate information to Experian, Equifax, and TransUnion. When they do not, consumers suffer. Credit scores drop. Loans get denied. Interest rates go up.

Credit One has faced multiple FCRA-related claims over the years, typically in three categories:

- Duplicate reporting: Both Credit One and a debt buyer reporting the same debt simultaneously after the account was sold

- Inaccurate status reporting: Showing accounts as “charged off” or “past due” when payments were made or the debt was settled

- Identity theft failures: Failing to investigate or correct disputed accounts opened fraudulently

In the Suluki v. Credit One Bank case in the Southern District of New York, a plaintiff alleged Credit One either willfully or negligently failed to conduct a reasonable investigation into her claims of identity theft, where her mother had opened accounts in her name without permission.

FCRA violations can allow you to recover:

- Actual damages such as denied credit, higher interest rates, and financial losses

- Statutory damages between $100 and $1,000 per violation

- Punitive damages for willful violations

- Attorney fees paid by the defendant

If you see inaccurate Credit One tradelines on your credit reports, file a dispute with the bureau first. If Credit One fails to investigate properly within 30 days, that is a potential FCRA violation.

Credit One Debt Collection Violation: Your Rights Under Federal Law

You have powerful rights under three separate federal laws when dealing with Credit One’s debt collection practices. Most people do not know any of them.

Under the TCPA: Automated calls to your cell phone without written consent are illegal. Period. Even debt collectors must follow this rule.

Under the Fair Debt Collection Practices Act (FDCPA): Debt collectors cannot call you before 8 a.m. or after 9 p.m. They cannot call your workplace if you tell them your employer disapproves. They must stop calling if you send a written cease-and-desist. They cannot use abusive, obscene, or harassing language.

Under California’s Rosenthal Act: California extends FDCPA protections to original creditors like Credit One itself, not just third-party collectors. That is why the state enforcement action hit Credit One directly. Making repetitive and unreasonable numbers of phone calls to people who owe debts is against the law in California because it is harassment. Capitol Plaque Lawsuit

Your action steps right now:

- Keep records of every call: date, time, caller ID, what was said

- Send a formal cease-and-desist letter via certified mail

- File a complaint at cfpb.gov and fcc.gov

- Contact a TCPA or FDCPA attorney; most offer free consultations

Key Takeaway: Federal and California state laws give consumers real tools to fight back. Documentation is the key to any successful claim.

Credit One Bank Settlement California: State-Specific Protections

California consumers have extra legal muscle that consumers in other states do not have. It matters. The $10.2M judgment proves it.

Credit One’s settlement came in a case involving the Rosenthal Fair Debt Collection Practices Act, a 1977 California law. The California Debt Collection Task Force has now won four settlements in cases involving debt-collection practices.

The Rosenthal Act is stronger than federal law in one critical way: it applies to original creditors. The federal FDCPA covers third-party collectors. California law covers any entity collecting a consumer debt, including the bank itself.

California consumers can also benefit from:

- UCL (Unfair Competition Law): Allows attorneys general and private plaintiffs to sue for unfair business practices

- Enhanced damages for seniors and disabled persons: Courts can award additional compensation when predatory behavior targets vulnerable consumers

- RFDCPA treble damages: Up to three times actual damages for willful violations

The court ordered Credit One and its agents to implement policies and procedures to prevent unreasonable and harassing debt collection calls to California consumers, including compliance with state and federal law concerning consumer debt collection calls.

This is not just about the money. It forces a policy change. Credit One must now maintain documented compliance procedures or face immediate court contempt.

Frequently Asked Questions

Is the Credit One Bank $14 million TCPA settlement real?

The $14 million TCPA settlement widely reported online appears to have no verified court record or case number. Legal professionals who searched federal court dockets found no supporting filing as of early 2026. The confirmed settlement is the $10.2M California civil judgment entered February 19, 2026.

How much will I get from the Credit One Bank lawsuit settlement?

From the California DA judgment, individual consumers receive nothing directly. Funds went to state penalties. From the express payment fee settlement, eligible cardholders may receive an automatic account credit or check, with distributions starting January-February 2026. For individual TCPA claims, the law allows $500 to $1,500 per unauthorized call, pursued through your own attorney.

Do I need to be a Credit One customer to qualify for the settlement?

No. TCPA protections apply to anyone whose phone number was called without consent. Credit One Bank continued to contact people who requested it stop and even called wrong numbers. Non-customers who received automated calls from Credit One or its vendors may have valid TCPA claims.

How do I file a Credit One Bank settlement claim?

For the express fee settlement, check for a class notice by mail or email; contact the Southern District of New York case administrator for Case No. 7:20-cv-10003. For individual TCPA claims, document your calls and contact a consumer protection attorney; many work with no upfront cost. For the Mingura class action (Case No. 4:25-cv-06712), monitor the case through PACER; class notice will be sent automatically if the case settles.

What happens to my Credit One account after the settlement?

Your active Credit One account is not automatically affected by any of these settlements. The court required Credit One and its agents to implement new policies and procedures to prevent unreasonable and harassing debt collection calls going forward. If you have an active dispute or FCRA complaint, pursue it separately through the credit bureaus or your own attorney.

What to Do Right Now

The confirmed Credit One Bank lawsuit settlement is real, court-signed, and dated February 19, 2026. It proves a pattern of phone harassment that California courts took nearly five years to address.

If you were charged a $9.95 express payment fee, check your accounts and mail now. Payments started going out in January 2026. If you received repeated automated calls from Credit One without your consent, you have live legal options under the TCPA today.

Do not wait for a “$14 million settlement” that legal professionals cannot find in any court record. Pursue the confirmed paths: file your CFPB complaint, document your calls, and reach out to a consumer protection attorney.