Quick Answer

- The MOHELA lawsuit is a federal consumer protection case, AFT v. MOHELA, now paused while both sides negotiate a possible settlement.

- Borrowers who experienced billing errors, PSLF or income-driven repayment delays, or credit reporting mistakes tied to MOHELA may have separate grounds for relief.

- No settlement has been finalized and no class has been certified, so there is currently no automatic claim process for individual borrowers.

| Detail | Info |

|---|---|

| Court | U.S. District Court for the District of Columbia |

| Case / Docket Number | 1:24-cv-02460-TSC |

| Presiding Judge | Tanya S. Chutkan |

| Filing Date | Originally filed July 22, 2024; amended January 15, 2026 |

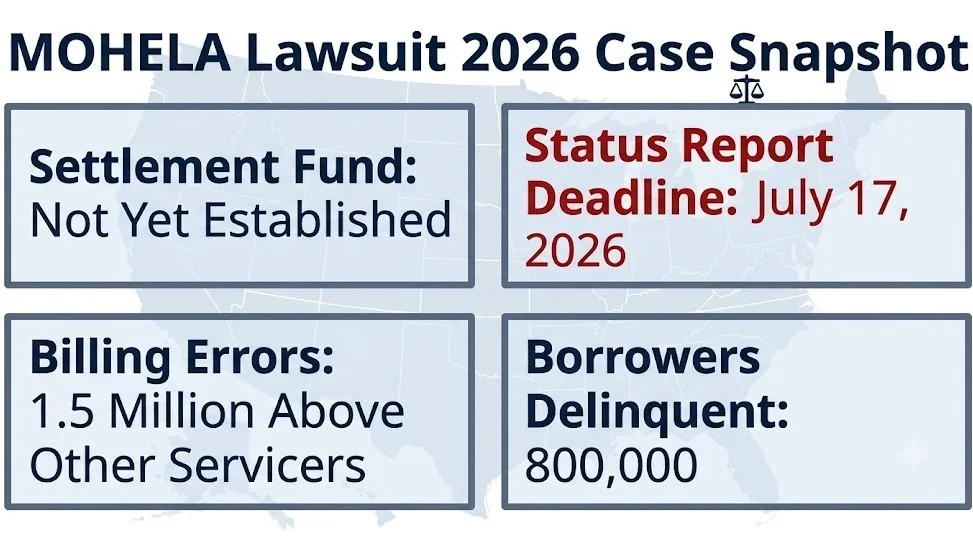

| Status | Paused for settlement negotiations since March 2026; status report due July 17, 2026 |

| Settlement Fund | Not yet established; no settlement has been finalized |

The MOHELA lawsuit picture in 2026 centers on one federal case that just went quiet for a reason. Settlement talks are now underway between the nation’s largest student loan servicer and the teachers’ union that sued it.

That case, filed in the District of Columbia, alleges MOHELA generated more billing errors than every other federal loan servicer combined during the return to repayment. Roughly 800,000 borrowers became delinquent as a result, according to the underlying complaint.

Separate from that case, borrowers are also pursuing credit reporting claims tied to servicer transfers, and Public Service Loan Forgiveness delays remain a distinct source of litigation. This piece separates all three threads and explains where each stands right now.

MOHELA Lawsuit

A MOHELA lawsuit refers to any of several active or recently active legal actions accusing the servicer of mismanaging federal student loan accounts. The most significant is a federal consumer protection case, not a personal injury or product liability claim.

That case, AFT v. MOHELA, was filed by the American Federation of Teachers on behalf of its members and the general public. It proceeds under the D.C. Consumer Protection Procedures Act, which prohibits unfair or deceptive trade practices.

MOHELA is a public instrumentality created by the state of Missouri in 1981, and it services loans on behalf of the U.S. Department of Education under a federal contract worth over $1.1 billion.

Quick Facts

- Lead case: AFT v. MOHELA, D.D.C.

- Legal theory: consumer protection, not tort or product liability

- Defendant: Higher Education Loan Authority of the State of Missouri

Attorneys handling these claims describe the case as one of the largest consumer protection actions ever brought against a federal student loan servicer.

MOHELA Lawsuit 2026

The MOHELA lawsuit in 2026 has moved from a jurisdictional fight into active settlement negotiations. That shift followed a January amendment adding new government data on MOHELA’s performance.

The amended complaint, filed January 15, 2026, cites federal data showing MOHELA borrowers wait roughly seven times longer than ED Financial customers to reach a representative. Among the five major servicers, MOHELA ranked worst on customer service.

By March 2026, both sides asked the court to pause litigation while they negotiate. A joint status report was due back to the court by July 17, 2026, detailing either a settlement or a plan to resume the case.

| 2026 Milestone | Date |

|---|---|

| Amended complaint filed | January 15, 2026 |

| Case paused for settlement talks | March 2026 |

| Status report deadline | July 17, 2026 |

Attorneys handling these claims note that a court-ordered pause for settlement talks typically signals real negotiating movement, not a stalled case.

MOHELA Lawsuit Update

The latest update in the MOHELA case is procedural: the parties remain in negotiations and have not yet announced a settlement or returned to active litigation. As of this writing, no dollar figure or relief structure has been made public.

Before reaching this stage, MOHELA spent over a year contesting the court’s jurisdiction. It argued sovereign immunity as an arm of Missouri and separately claimed federal contractor immunity.

The court rejected the immunity defenses. On September 29, 2025, the court denied efforts to keep the case out of federal court on those grounds, allowing the underlying claims to proceed.

- MOHELA raised sovereign immunity and federal contractor immunity defenses

- The court found MOHELA has only a colorable, not conclusive, immunity claim

- Litigation proceeded to an amended complaint and now settlement talks

Attorneys handling these claims point to the immunity ruling as a significant procedural win that kept the case alive in federal court.

Litigation Watch: The core MOHELA case survived a sovereign immunity challenge, moved to an amended complaint citing new government data, and is now paused for settlement negotiations with a July 17, 2026 status deadline.

Who Qualifies for MOHELA Lawsuit

Qualification depends on which MOHELA-related claim a borrower is considering, since there is no single unified case covering every servicing complaint. The lead AFT case is an organizational lawsuit, not an individual claims program.

Borrowers with documented billing errors, delayed Public Service Loan Forgiveness processing, or income-driven repayment mishandling fall within the conduct described in the AFT complaint, even though that case does not currently offer them a direct claim path.

Separately, borrowers who experienced credit reporting errors after a servicer transfer, particularly from Nelnet to MOHELA, may have individual claims under federal credit reporting law.

| Borrower Situation | Relevant Legal Action |

|---|---|

| Billing errors, delinquency after 2023 repayment restart | AFT v. MOHELA (D.D.C.) |

| PSLF or IDR processing delays | AFT v. MOHELA and related PSLF litigation |

| Credit report showed inflated balance after transfer | Individual FCRA and Privacy Act claims |

Attorneys handling these claims recommend borrowers keep dated records of every billing statement, denial letter, and credit report pull, since documentation drives eligibility more than the servicing complaint alone.

MOHELA Lawsuit Eligibility

Eligibility for any MOHELA-related legal action depends on the specific harm alleged and whether it fits an existing case theory. No blanket eligibility standard currently exists across all the pending matters.

For the AFT case, eligibility as a direct claimant is not yet available, since AFT sued as an organization on behalf of its members and the public, not as a certified borrower class.

For individual credit reporting claims, eligibility generally requires a documented balance discrepancy following a servicer transfer, and evidence the error was disputed with the credit bureau and not corrected.

- Documented billing or processing error tied to MOHELA servicing

- Evidence the issue was reported and not resolved

- For credit claims, a specific, provable balance discrepancy after a transfer

Attorneys handling these claims caution that eligibility today is largely case specific, since no certified class exists yet to define a uniform standard.

MOHELA Student Loan Servicing Lawsuit

The MOHELA student loan servicing lawsuit alleges the company systematically mishandled federal loan accounts during and after the 2023 return to repayment. The complaint describes a pattern, not isolated incidents.

According to court records, MOHELA made 1.5 million more billing-related errors than all other federal servicers combined during the return to repayment period, based on a Senate-commissioned report.

The complaint also describes a company-wide “call deflection” practice, allegedly designed to route borrowers toward self-help tools rather than resolving account errors directly with staff.

Bold callout: MOHELA generated more billing errors than every other federal student loan servicer combined during the return to repayment.

Attorneys handling these claims describe the alleged call deflection practice as central to the case, since it goes to intent rather than simple servicing mistakes.

MOHELA Lawsuit Settlement

There is no finalized MOHELA lawsuit settlement as of July 2026, since the parties are still in confidential negotiations under a court-ordered pause. Any settlement terms discussed publicly right now are speculative.

The court paused the case in March 2026 specifically to allow settlement talks to continue, and both sides requested at least one 60-day extension of that pause.

According to the joint status report structure, the parties were required to update the court by July 17, 2026, either announcing a resolution or a plan to resume litigation.

| Settlement Status Fact | Detail |

|---|---|

| Settlement finalized | No |

| Case status | Paused for negotiation |

| Next court deadline | July 17, 2026 |

| Relief structure disclosed | Not yet public |

Attorneys handling these claims note that consumer protection settlements of this type often include injunctive commitments on servicing practices, not only monetary relief.

MOHELA Lawsuit Payout

There is no confirmed payout figure for individual borrowers in the MOHELA lawsuit, because the AFT case is not currently structured as an individual damages claim. The lawsuit primarily seeks to stop ongoing unlawful practices under D.C. consumer protection law.

If a settlement is reached, relief in cases like this typically combines injunctive changes to servicing conduct with some form of restitution, though the exact structure has not been disclosed.

Separately, individual credit reporting claims under the Fair Credit Reporting Act and Privacy Act can carry their own statutory damages, independent of whatever the AFT case eventually resolves.

- AFT case: primarily seeks injunctive relief and public accountability, not confirmed individual payouts

- Credit reporting claims: potential statutory damages under FCRA and the Privacy Act

- No global payout figure exists for either track as of mid-2026

Attorneys handling these claims stress that a consumer protection settlement and an individual credit reporting claim are different legal paths with different payout structures.

MOHELA Class Action

MOHELA is not currently facing a certified class action, despite frequent references to one in online coverage. The lead federal case is an organizational suit brought by a union, and the credit reporting case is an individual claim that could become a class if certified later.

In the credit reporting matter, filed by borrower Adriana Walsh, the court has not certified a class as of this writing. Other borrowers who experienced the same suppressed double-reporting issue after a servicer transfer could potentially be included automatically if certification occurs.

Separately, individual state court lawsuits, including one filed in California, allege thousands of statutory violations tied to MOHELA’s servicing conduct, independent of the D.C. federal case.

| Case | Class Status |

|---|---|

| AFT v. MOHELA (D.D.C.) | Not a class action; organizational suit |

| Walsh v. Dept. of Education | No class certified yet |

| Maldonado v. MOHELA (California) | Individual claim, alleges thousands of violations |

Attorneys handling these claims caution readers against assuming any MOHELA case currently guarantees automatic inclusion, since no certification order has been issued.

Litigation Watch: No MOHELA case has reached class certification as of mid-2026, and eligibility for relief currently depends on which specific legal theory a borrower’s harm fits.

MOHELA Lawsuit Court Case

The MOHELA court case with the most significant procedural history is AFT v. MOHELA, filed originally in D.C. Superior Court and later moved to federal court. Its jurisdictional fight shaped much of 2025.

AFT filed the case on July 22, 2024, as No. 2024-CAB-4576 in D.C. Superior Court. MOHELA removed it to federal court on August 26, 2024, arguing it was immune from the D.C. Consumer Protection Procedures Act.

The federal court, under Judge Tanya S. Chutkan, denied AFT’s motion to remand the case back to D.C. Superior Court on September 29, 2025, keeping the matter in federal court under Case No. 1:24-cv-02460-TSC.

| Procedural Step | Date |

|---|---|

| Original filing, D.C. Superior Court | July 22, 2024 |

| Removal to federal court | August 26, 2024 |

| Remand motion denied | September 29, 2025 |

| Amended complaint filed | January 15, 2026 |

Attorneys handling these claims describe the jurisdictional fight as unusually long for a consumer protection case, largely due to MOHELA’s layered immunity arguments.

MOHELA PSLF Lawsuit

A MOHELA PSLF lawsuit specifically targets delays in processing Public Service Loan Forgiveness applications, a distinct problem from the general billing errors described in the AFT case. PSLF-specific claims have been raised separately since at least February 2024.

The Project on Predatory Student Lending has pursued litigation alleging MOHELA failed to process and decide PSLF applications in a timely manner, leaving borrowers in prolonged limbo over forgiveness they had already earned.

The AFT complaint also references PSLF processing failures as part of its broader pattern allegations, showing overlap between the two litigation tracks even though they proceed as separate matters.

- PSLF-specific claims focus narrowly on forgiveness application delays

- The broader AFT case cites PSLF failures as one example among many servicing problems

- Both tracks rely on documented processing timelines as core evidence

Attorneys handling these claims recommend PSLF applicants keep a dated record of every submission and status inquiry, since processing timelines are the central evidence in these cases.

MOHELA Credit Reporting Lawsuit

A MOHELA credit reporting lawsuit alleges the servicer, in coordination with the Department of Education, allowed inaccurate balances to appear on borrower credit reports after account transfers. This is a legally distinct claim from the AFT servicing case.

Borrower Adriana Walsh filed suit against the U.S. Department of Education on February 18, 2026, after her $150,000 loan balance appeared as $300,000 on her credit report following a transfer from Nelnet to MOHELA.

The complaint asserts violations of the Fair Credit Reporting Act and the Privacy Act of 1974, made possible by a 2024 Supreme Court ruling allowing borrowers to sue federal agencies over credit reporting errors.

Bold callout: A borrower’s loan balance doubled from $150,000 to $300,000 on her credit report after a servicer transfer to MOHELA.

Attorneys handling these claims note that the underlying complaint references roughly 500 similar credit reporting complaints received by the Department since December 2023.

Join MOHELA Lawsuit

There is currently no formal process to join the AFT case, since it proceeds as an organizational lawsuit rather than an opt-in claim. Borrowers cannot sign up for a claim number the way they might in a certified class action.

Union members affected by MOHELA’s conduct are represented indirectly through AFT’s organizational standing in the case, without needing to file individually.

Borrowers outside that structure, particularly those with individual credit reporting harm, generally need to pursue their own claim with an attorney rather than join an existing filing.

- AFT case: no individual opt-in process currently exists

- Credit reporting harm: individual claim required, no certified class yet

- PSLF delays: may support an individual claim depending on documentation

Attorneys handling these claims advise against paying any service that claims to register borrowers into the AFT lawsuit, since no such enrollment mechanism exists.

How to File a MOHELA Complaint

Filing a complaint against MOHELA starts with documenting the specific servicing failure, then choosing the correct venue based on the type of harm involved. A billing dispute and a credit reporting error follow different paths.

For servicing errors, borrowers typically start with a formal written complaint to MOHELA and the Department of Education’s ombudsman, creating a paper trail before pursuing legal action.

For credit reporting errors specifically, disputing the information directly with the credit bureau is a necessary first step before an FCRA claim can proceed, since the law generally requires that dispute to occur first.

| Step | Applies To |

|---|---|

| File written complaint with MOHELA and FSA ombudsman | General servicing errors |

| Dispute directly with credit bureau | Credit reporting errors |

| Consult an attorney if unresolved | Any documented, unresolved harm |

Attorneys handling these claims stress that a documented dispute history is often what separates a viable individual claim from an unresolved customer service complaint.

MOHELA Lawsuit Attorney

A MOHELA lawsuit attorney is typically a consumer protection or student loan attorney, not a general personal injury lawyer. The relevant law here involves the D.C. Consumer Protection Procedures Act, the Fair Credit Reporting Act, and federal servicing regulations.

Attorneys at organizations including the Student Borrower Protection Center and the National Consumer Law Center have led the litigation against MOHELA, working alongside private firms such as Selendy Gay PLLC.

Borrowers considering an individual claim, particularly a credit reporting case, should look for attorneys experienced specifically in FCRA litigation against federal agencies and their contractors.

- Ask whether the attorney has handled FCRA claims against federal loan servicers specifically

- Ask how documentation requirements differ for billing versus credit reporting claims

- Ask whether the firm is tracking the AFT settlement talks and what that means for a new claim

Attorneys handling these claims generally recommend counsel with direct FCRA and student loan servicing experience, since general consumer complaint attorneys may not handle the federal contractor angle.

MOHELA Lawsuit Timeline

The MOHELA lawsuit timeline stretches back to July 2024 and remains open, with the most important current marker being the July 17, 2026 status deadline. Understanding this sequence helps explain why no settlement has been announced yet.

The case moved through more than a year of jurisdictional disputes before reaching substantive litigation, then shifted to settlement negotiations in early 2026.

| Phase | Date |

|---|---|

| Original filing | July 22, 2024 |

| Case removed to federal court | August 26, 2024 |

| Remand motion denied | September 29, 2025 |

| Amended complaint | January 15, 2026 |

| Settlement talks pause litigation | March 2026 |

| Status report due | July 17, 2026 |

Attorneys handling these claims note that a case moving from a year of jurisdictional fights directly into settlement talks often reflects real pressure on both sides to resolve rather than retry the immunity issue.

MOHELA Lawsuit Deadline

There is no single national filing deadline for MOHELA-related claims, since deadlines depend on the specific legal theory and applicable statute of limitations. The AFT case deadline questions are different from an individual borrower’s own filing window.

For individual claims, including credit reporting disputes, the relevant statute of limitations under federal credit reporting law generally runs from when the error was discovered, not when it first occurred.

Borrowers considering their own claim should not assume they have unlimited time, particularly given how quickly credit reporting and servicing evidence can become harder to obtain.

- No universal deadline applies across all MOHELA-related legal actions

- Individual FCRA claims generally run from discovery of the error

- Confirming a personal deadline requires attorney review of the specific claim type

Attorneys handling these claims recommend acting promptly to preserve records, even where the exact deadline is not yet clear.

MOHELA Lawsuit by State

MOHELA lawsuits are being pursued in multiple jurisdictions, including the District of Columbia and California, with venue often depending on where the plaintiff filed or where the specific consumer protection law applies. This is not a single nationwide case.

The lead AFT case relies specifically on D.C.’s Consumer Protection Procedures Act, which shaped why that lawsuit was filed there rather than in another state.

Separately, an individual case, Maldonado v. MOHELA, was filed in California Superior Court in September 2024, alleging thousands of statutory violations under different state law theories.

| State or Jurisdiction | Case | Legal Basis |

|---|---|---|

| District of Columbia | AFT v. MOHELA | D.C. Consumer Protection Procedures Act |

| California | Maldonado v. MOHELA | State statutory violations |

| Federal (nationwide) | Walsh v. Dept. of Education | FCRA and Privacy Act |

Attorneys handling these claims note that state consumer protection law can differ significantly, which is why similar MOHELA conduct has produced separate cases in different courts.

Frequently Asked Questions

Is there an active MOHELA lawsuit in 2026?

Yes, the lead case, AFT v. MOHELA, remains active but is currently paused for settlement negotiations.

A status report was due to the federal court by July 17, 2026, addressing whether a settlement was reached.

Who qualifies to join a MOHELA lawsuit?

There is no formal opt-in process for the AFT case, since it proceeds as an organizational lawsuit.

Borrowers with individual credit reporting or PSLF processing harm may instead have grounds for a separate individual claim.

Has MOHELA reached a settlement with borrowers?

No settlement has been finalized as of July 2026, based on the most recent public court filings.

The parties requested a pause in litigation specifically to continue negotiating a resolution.

Is there a MOHELA class action lawsuit?

No MOHELA case has reached class certification as of this writing.

The credit reporting case against the Department of Education could potentially become a class action if a court certifies it later.

How long will the MOHELA lawsuit take to resolve?

The case has already run more than a year through jurisdictional disputes before reaching settlement talks in 2026.

A final resolution timeline depends on whether the current negotiations succeed or the case returns to active litigation.

Is there a deadline to file a complaint against MOHELA?

There is no single national deadline, since different MOHELA-related claims follow different statutes of limitations.

Individual claims, particularly credit reporting disputes, generally run from when the error was discovered.

The MOHELA case has moved from a jurisdictional fight to real settlement talks, with a court deadline now set for July 17, 2026. No payout structure exists yet for individual borrowers.

Anyone with documented billing, PSLF, or credit reporting harm tied to MOHELA should preserve that paperwork now and consult a consumer protection or student loan attorney about an individual claim.