Symple Lending LLC faces multiple active federal lawsuits alleging illegal spam texting, deceptive loan advertising, and bait-and-switch debt settlement practices. Three TCPA class action cases are currently active in federal court in Florida, with potential damages of up to $1,500 per violation per class member. No settlement has been reached as of March 2026 — but if you received unsolicited texts from Symple Lending or were misled about their services, you may already have legal rights worth protecting.

Quick Answer: Symple Lending is named in at least four federal lawsuits filed between 2021 and 2025. The most significant are three TCPA class actions alleging illegal marketing texts sent to people on the Do Not Call Registry. These cases are active and ongoing — no settlement fund is open for claims yet. If you were contacted without consent or deceived about loan products, you should document everything now and consult an attorney.

This guide walks you through every lawsuit against Symple Lending, what the allegations mean for you, how to protect your rights, and what to watch for as these cases move through the courts. The Phoenix ED Device Lawsuit

What Is the Symple Lending Lawsuit About?

Background: Who Is Symple Lending?

Symple Lending LLC is a loan marketplace and lead-generation company registered in Wyoming and operating out of Tampa (and previously Irvine), California. The company markets itself as a personal loan provider offering debt consolidation, home improvement, and personal loans — with advertised rates starting at 6.99%. Its NMLS ID is #2508833.

Despite a slick website and an A+ BBB rating, Symple Lending’s business model is considerably murkier than it appears. Its own Terms of Use describe its role as “connecting consumers with third-party advertisers or lenders” — meaning it does not directly originate loans. Across Trustpilot, BBB, and other review platforms, no verified consumer review describes actually receiving a funded loan from Symple Lending or its lending partners.

Instead, a pattern emerges in consumer complaints: people call or apply expecting a personal loan, and end up being steered toward high-fee debt settlement programs from companies like Beyond Finance or Freedom Debt Relief. That’s not an accident — a 2021 court filing (DMB Financial v. Symple Lending) documents a formal affiliate sales agreement for debt settlement referrals, in which Symple Lending received a $110,000 advance for connecting consumers to a debt settlement company.

The company also has a complicated leadership history. Co-founder Houston Fraley is subject to a 2017 FTC permanent injunction for illegal telemarketing practices — an enforcement action that bars him from certain telemarketing activities. Symple Lending has been sued for telemarketing violations multiple times since.

The Four Active Lawsuits at a Glance

| Case Name | Court | Filed | Type | Status |

|---|---|---|---|---|

| Turizo v. Symple Lending LLC | S.D. Florida (Case 0:2024cv61274) | July 18, 2024 | TCPA Class Action | Active |

| Paniagua v. Symple Lending LLC | S.D. Florida | October 2024 | TCPA Class Action | Active |

| Betts v. Symple Lending LLC | S.D. Florida (Case 0:25-cv-60114) | January 20, 2025 | TCPA Class Action | Active |

| Troutman et al v. Symple Lending LLC | C.D. California (Case 8:25-cv-01181) | May 30, 2025 | Trademark Infringement | Active |

| DMB Financial v. Symple Lending et al | D. Massachusetts (Case 1:2021cv12065) | December 17, 2021 | Contract Dispute | Resolved |

Timeline of Key Legal Events

| Date | Event | Details |

|---|---|---|

| December 2021 | DMB Financial files suit | Contract dispute over $110,000 advance for debt settlement referrals; Beyond Finance named as co-defendant |

| 2017 | FTC injunction against Houston Fraley | Permanent injunction for illegal telemarketing related to prior company |

| July 18, 2024 | Turizo v. Symple Lending filed | First TCPA class action in S.D. Florida; alleges unsolicited texts to Do Not Call numbers |

| October 2024 | Paniagua v. Symple Lending filed | Second TCPA class action; plaintiff reports 6+ unwanted texts while on DNC Registry since 2011 |

| January 20, 2025 | Betts v. Symple Lending filed | Third TCPA class action in S.D. Florida (Case 0:25-cv-60114) |

| May 30, 2025 | Troutman et al v. Symple Lending filed | Trademark infringement over confusingly similar lion logo; federal court issued TRO against Symple Lending |

| 2025–2026 | All TCPA cases active | No settlement reached; litigation ongoing |

The TCPA Lawsuits: What Are the Allegations?

The core allegations in all three TCPA class actions follow a similar pattern. Symple Lending allegedly sent unsolicited marketing texts to people who never gave consent — and who were registered on the National Do Not Call Registry.

What Is the TCPA?

The Telephone Consumer Protection Act (TCPA) is the federal law that protects consumers from unwanted telemarketing calls and texts. It gives consumers the right to:

- Be placed on the Do Not Call Registry to stop marketing calls and texts

- Sue companies that violate those protections

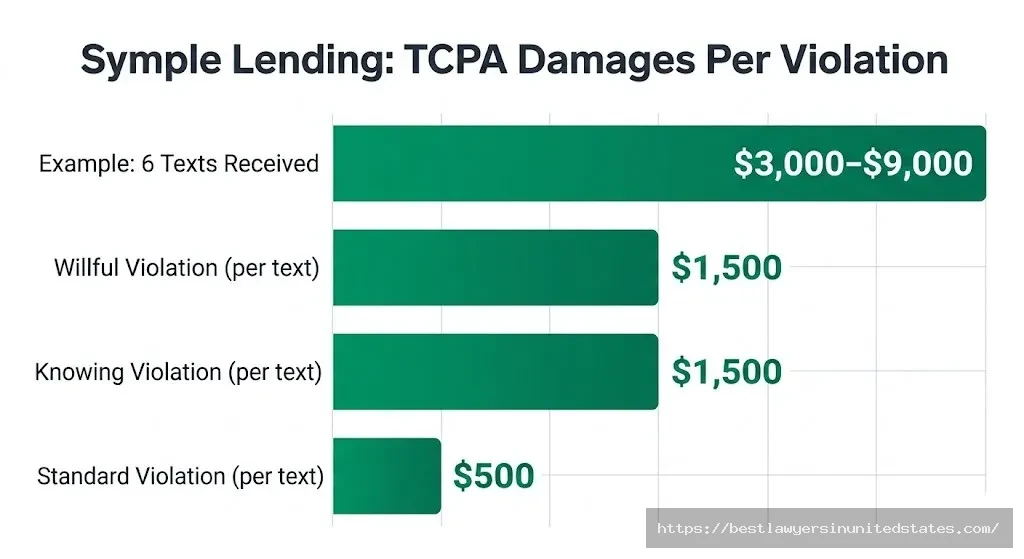

- Recover $500 per violation, or $1,500 per knowing or willful violation

Those numbers add up fast when a company is texting thousands of people without consent.

Key Allegations Against Symple Lending

The three TCPA class actions allege that Symple Lending:

- ✅ Sent unsolicited marketing texts to consumers’ cell phones without prior express written consent

- ✅ Continued texting consumers whose numbers were registered on the National Do Not Call Registry

- ✅ Texted people who had never done business with Symple Lending and never requested information

- ✅ Used text messages “to advertise, promote, and/or market” its financial products in violation of federal law

- ✅ Engaged in a pattern of mass cold-texting as part of a high-volume lead generation operation

In the Paniagua case, the plaintiff reports receiving six or more unsolicited texts — despite being on the Do Not Call Registry since 2011 and having zero prior relationship with the company.

Who Filed the TCPA Lawsuits?

- Turizo v. Symple Lending LLC — Filed July 2024 in the Southern District of Florida

- Paniagua v. Symple Lending LLC — Filed October 2024 in the Southern District of Florida (brought to wider attention through TCPA World)

- Betts v. Symple Lending LLC — Filed January 20, 2025 in the Southern District of Florida; Judge Rodney Smith presiding; Burr & Forman representing Symple Lending

All three cases are class actions, meaning they seek to represent not just the individual plaintiffs but potentially thousands of other consumers who received similar unsolicited texts from Symple Lending.

An Important Legal Wrinkle

TCPA litigation against Symple Lending faces one significant legal uncertainty: federal courts are currently split on whether DNC protections apply to text messages. On the same day in July 2025, one federal court ruled DNC rules do apply to texts, while another ruled they do not. This jurisdictional conflict may affect how the Florida cases proceed or resolve.

That said, separate TCPA provisions — specifically those requiring prior express written consent for marketing texts — may provide an independent basis for liability regardless of how the DNC question is resolved.

The Deceptive Practices Allegations

Beyond the TCPA cases, Symple Lending faces broader consumer protection allegations that, while not yet consolidated into a single class action, have generated significant complaint volume and legal scrutiny.

Bait-and-Switch: Loans That Become Debt Settlement

The most common consumer complaint against Symple Lending follows a consistent pattern:

- A consumer sees advertising for low-interest personal loans (rates starting at 6.99%)

- They call or apply online expecting a loan

- Instead of receiving a loan offer, they’re steered — sometimes aggressively — toward a debt settlement program

- The debt settlement program comes with high fees and credit score consequences the consumer was not warned about

According to Finder.com’s 2026 review, Symple Lending’s website makes no mention of debt settlement services — yet consumer complaints about being funneled into debt settlement are widespread and consistent. National Life Group Lawsuit

What Laws May Be Implicated

Legal analysts covering the Symple Lending complaints have identified several consumer protection laws that could be relevant:

| Law | What It Requires | Potential Violation |

|---|---|---|

| Truth in Lending Act (TILA) | Clear disclosure of loan terms, fees, APR | Failure to disclose actual costs |

| Fair Debt Collection Practices Act (FDCPA) | Honest, non-deceptive communication | Misleading advertising practices |

| TCPA | Prior consent for marketing texts | Unsolicited texts to DNC numbers |

| FTC Act Section 5 | No unfair or deceptive business practices | Bait-and-switch marketing |

As of March 2026, Symple Lending has no federal enforcement actions from the FTC or CFPB on record. However, the pattern of litigation and consumer complaints has drawn significant regulatory attention.

The Debt Settlement Referral Business Model

A 2021 court filing (DMB Financial v. Symple Lending) pulls back the curtain on how Symple Lending actually makes money. The lawsuit documents:

- A formal affiliate sales agreement between Symple Lending and DMB Financial, a debt settlement company

- A $110,000 advance paid to Symple Lending for directing consumers toward debt settlement

- Disputed commissions of $6,000 for consumer referrals

- Beyond Finance named as a co-defendant in the contract dispute

This documented relationship between Symple Lending and debt settlement companies is central to consumer deception claims — because it shows the company had a direct financial incentive to steer people away from the loans it advertised and into debt settlement instead.

Who Might Have a Legal Claim Against Symple Lending?

Because no class action settlement has been reached yet, there’s no claim form or deadline to file right now. But you may have legal rights worth pursuing if you fall into one of these categories.

TCPA Claims: Did Symple Lending Text You Without Consent?

| Question | What It Means |

|---|---|

| Did you receive texts from Symple Lending? | You may qualify for a TCPA claim |

| Were you registered on the Do Not Call list? | Strengthens your potential claim |

| Did you ever give Symple Lending your number? | If no, consent was likely absent |

| Did you receive multiple texts? | More violations = more potential damages |

| Did you ask them to stop and they didn’t? | Additional violations may apply |

You might have a TCPA claim if:

- ✅ You received unsolicited text messages from Symple Lending

- ✅ You never gave Symple Lending your phone number or consent to be contacted

- ✅ Your number was (or is) on the National Do Not Call Registry

- ✅ You had no existing business relationship with Symple Lending when the texts arrived

- ✅ You received multiple texts, especially after telling them to stop

Deceptive Practices Claims: Were You Misled About Loans?

You may have consumer protection claims if:

- ✅ You contacted Symple Lending expecting a personal loan and were steered to debt settlement instead

- ✅ You were not clearly told you were being referred to a third-party debt settlement program

- ✅ You signed up for a debt settlement program based on representations that turned out to be false or misleading

- ✅ You paid fees to a debt settlement company you were referred to by Symple Lending without understanding what you were signing

- ✅ You suffered credit damage or financial harm after being enrolled in a program you didn’t fully understand

Who Likely Does NOT Have a Claim

You probably don’t have a current legal claim against Symple Lending if:

- ❌ You gave Symple Lending prior express written consent to send you marketing texts

- ❌ You voluntarily enrolled in a debt settlement program and received the services described

- ❌ Your only complaint is that you don’t like the company’s practices but suffered no actual harm

- ❌ You’re outside the statute of limitations (generally 4 years for TCPA claims)

How Much Could You Recover?

No settlement has been reached in any of the Symple Lending cases, so there are no guaranteed payout amounts. However, TCPA law provides statutory damages — meaning you can recover a set amount per violation without having to prove specific dollar losses.

TCPA Statutory Damages Structure

| Violation Type | Damages per Violation | When It Applies |

|---|---|---|

| Standard TCPA violation | $500 | Each unsolicited text or call |

| Knowing or willful violation | $1,500 | When company knew it was violating the law |

| DNC Registry violation | $500–$1,500 | Texts/calls to registered numbers |

If you received six unsolicited texts (like the Paniagua plaintiff), your potential recovery could range from $3,000 to $9,000 for your individual claim under the TCPA’s statutory damages provisions.

In class actions, total exposure for defendants can run into the tens of millions of dollars. For context:

How Symple Lending Compares to Similar TCPA Cases

| Case | Settlement/Exposure | Violations Alleged | Outcome |

|---|---|---|---|

| Symple Lending (active) | TBD | Mass DNC texting | Pending |

| Major Bank TCPA case (2025) | $3.3 billion exposure | Millions of calls | Certified class |

| Typical TCPA settlement | $10M–$50M | Tens of thousands of contacts | Varies |

| Individual TCPA claim | $500–$1,500/text | Per-message violations | Case-by-case |

Important: Until a settlement is reached and a court approves it, there is no fund to claim from. Anyone telling you there’s a current settlement or a deadline to file a claim in the Symple Lending cases is misinformed. Lawsuit in Spanish

What to Do Right Now If You Were Affected

Even though there’s no settlement claim process yet, what you do now can make a significant difference in your legal options later.

Step 1: Document Everything

Save these immediately:

- Screenshots of every text message you received from Symple Lending (with dates and phone numbers visible)

- Records of when you were added to the Do Not Call Registry (check donotcall.gov)

- Any voicemails, emails, or chat logs from Symple Lending

- Records of any loan applications or accounts you opened

- Documentation of any debt settlement program you were enrolled in

- Any financial losses, credit score changes, or fees paid

Step 2: Check Your Do Not Call Registry Status

Go to donotcall.gov and verify your number is registered. If it wasn’t registered when Symple Lending contacted you, registration alone doesn’t give you retroactive DNC protection — but documenting the timeline matters.

Step 3: File a Complaint

File complaints with:

| Agency | Where to File | Why It Matters |

|---|---|---|

| FTC (Do Not Call violations) | donotcall.gov/report | Creates federal record |

| CFPB (lending practices) | consumerfinance.gov/complaint | Adds to regulatory database |

| BBB | bbb.org | Public complaint record |

| Your state attorney general | State AG website | State consumer protection |

As of February 2026, Symple Lending has zero CFPB complaints on record — which means filing one adds meaningful data to the regulatory picture.

Step 4: Consult a TCPA Attorney

TCPA lawyers typically work on contingency, meaning you pay nothing upfront. They get paid only if they win your case. Given that each text message could mean $500–$1,500 in statutory damages, even individual claims can be worth pursuing.

You can find TCPA attorneys through:

- The National Association of Consumer Advocates (NACA): consumeradvocates.org

- State bar referral services

- Legal aid organizations in your state

Step 5: Monitor These Cases

Check these sources periodically for case updates:

- PACER (federal court records): Turizo (Case 0:2024cv61274), Betts (Case 0:25-cv-60114)

- Justia.com — free federal docket tracking

- TCPA World (tcpaworld.com) — follows TCPA litigation closely

- Court settlement administrator websites (when a settlement is eventually announced)

Current Status of All Symple Lending Lawsuits (March 2026)

TCPA Cases: Active Litigation

All three TCPA class actions — Turizo, Paniagua, and Betts — are in active litigation as of March 2026. None have reached settlement. No claim forms exist. No deadlines for consumer claims have been set. byte aligners current status 2026

| Milestone | Status |

|---|---|

| Complaints filed | ✅ All three cases filed |

| Discovery phase | Ongoing |

| Class certification | Not yet decided |

| Settlement negotiations | No public indication of progress |

| Settlement reached | ❌ Not yet |

| Court approval of settlement | ❌ Not applicable |

| Claims filing period open | ❌ Not yet |

Trademark Case: Court Issued TRO, Then Denied Preliminary Injunction

In the Troutman et al v. Symple Lending case over the lion logo, a federal court initially issued a Temporary Restraining Order (TRO) barring Symple Lending’s use of the logo. However, when the preliminary injunction was litigated, the court found that the plaintiff did not adequately demonstrate likelihood of consumer confusion — particularly because a law firm and a loan marketing company don’t operate in the same market space. The case continues.

What Comes Next

The path forward for the TCPA cases will likely follow this sequence:

| Stage | What Happens |

|---|---|

| Discovery | Both sides exchange evidence, depose witnesses |

| Class certification motion | Plaintiffs ask court to certify a class of affected consumers |

| Ruling on class certification | Judge decides whether case can proceed as a class action |

| Potential settlement negotiations | Often happens around or after class certification |

| If settled: preliminary approval | Court reviews proposed settlement terms |

| If settled: notice to class members | Affected consumers notified with claim instructions |

| If settled: claims deadline | Consumers file claims within a set window |

| If settled: final approval & payment | Judge approves, payments distributed |

The entire process from active litigation to settlement payment typically takes 1–3 years in complex TCPA class actions.

Do You Need a Lawyer?

Quick Answer: For TCPA claims, consulting a lawyer costs you nothing upfront — and TCPA statutory damages make many claims economically worthwhile even without a big settlement fund.

When You Can Handle It Yourself

If your goal is simply to:

- File a complaint with the FTC, CFPB, or BBB

- Document your experience for the public record

- Join a class action that eventually gets certified (no lawyer needed — you’ll automatically be included)

…then you don’t need an attorney right now.

When Legal Help Makes Sense

Talk to a TCPA or consumer protection attorney if:

- You received multiple unsolicited texts from Symple Lending

- You were enrolled in a debt settlement program you didn’t understand or consent to

- You suffered measurable financial harm (fees paid, credit damage, etc.)

- You want to pursue an individual claim rather than wait for a class settlement

- You have documentation and want to understand your options

Finding Free Legal Help

Several resources offer free consultations for TCPA and consumer protection matters:

- National Association of Consumer Advocates (NACA): consumeradvocates.org — find a consumer law attorney in your state

- Consumer Financial Protection Bureau: consumerfinance.gov — can point you to legal resources

- Legal aid organizations: Search “[your state] legal aid” for free or low-cost help

- State bar referral services: Most state bars offer a free or low-cost initial referral

TCPA attorneys work on contingency — your case’s potential value comes from statutory damages, not out-of-pocket losses, so you don’t need to have lost money to have a viable claim.

Symple Lending’s Business Practices: A Closer Look

Understanding how Symple Lending operates helps you evaluate your own situation and legal options.

The Loan Marketplace Model

Symple Lending is not a direct lender. Its Terms of Use explicitly describe the company as connecting consumers with “third-party advertisers or lenders.” This means:

- When you apply, your information is shared with third parties

- The loan terms you receive (APR, fees, repayment) are set by those third parties, not Symple Lending

- Symple Lending’s website claims rates starting at 6.99%, but rates could reach up to 35% APR based on the Terms of Use

- Symple Lending makes money from referral fees and lead sales

The Arbitration Clause Problem

Symple Lending’s Terms of Use include a mandatory arbitration agreement and class action waiver. This means:

- By using their website or submitting your information, you may have agreed to resolve disputes through arbitration rather than in court

- Arbitration hearings are held in Hillsborough County, Florida

- The class action waiver attempts to prevent you from joining or bringing a class action

However, this clause has important limits. TCPA class actions brought by plaintiffs who received texts without ever visiting Symple Lending’s website may not be bound by this arbitration agreement. If you were texted cold — without ever interacting with the company — your TCPA rights may be fully intact.

The Founder’s Background

One of Symple Lending’s founders, Houston Fraley, is subject to a 2017 FTC permanent injunction for illegal telemarketing practices related to a prior company (Allorey, Inc.). This means the company’s leadership has direct personal experience with federal telemarketing enforcement — making the pattern of TCPA lawsuits that followed particularly significant.

Frequently Asked Questions

What is the Symple Lending lawsuit?

There are actually multiple lawsuits. The most significant are three TCPA class action cases filed in the Southern District of Florida between July 2024 and January 2025, alleging Symple Lending sent unsolicited marketing texts to consumers on the Do Not Call Registry. There is also a trademark suit and a resolved contract dispute.

Is there a Symple Lending class action settlement I can claim from?

No. As of March 2026, none of the Symple Lending TCPA lawsuits have settled. There is no claim form, no settlement fund, and no deadline for consumers to submit claims. Anyone telling you otherwise is providing inaccurate information.

What is the TCPA and why does it matter here?

The Telephone Consumer Protection Act is the federal law that protects consumers from unwanted marketing calls and texts. It allows affected consumers to sue for $500–$1,500 per violation — even without proving financial damages. Symple Lending is accused of violating the TCPA by texting people on the Do Not Call Registry without their consent.

How do I know if I was affected?

You were likely affected if you received text messages from Symple Lending that you didn’t ask for, especially if you had no prior relationship with the company and/or your number was on the Do Not Call Registry.

How much money could I get from a Symple Lending TCPA lawsuit?

TCPA law allows $500 per violation and $1,500 per knowing violation. If you received six texts, your potential individual recovery could be $3,000–$9,000. Class action settlements typically distribute smaller per-person amounts across a large class.

Do I need a lawyer to pursue a TCPA claim?

Not necessarily, but it helps. TCPA attorneys work on contingency — no upfront cost to you. Given the statutory damages available, many TCPA claims are worth pursuing with legal help.

What should I do if I received unsolicited texts from Symple Lending?

Screenshot every text immediately. Note the sending phone number and dates. Check your Do Not Call Registry status. File a complaint at donotcall.gov and with the CFPB. Then consult a TCPA attorney for your individual options.

Is Symple Lending a scam?

It’s a registered company with an NMLS license and A+ BBB rating. But it faces credible legal allegations including three active federal class actions. Its business model — marketing loans while referring people to debt settlement — has generated consistent consumer complaints about deceptive practices. Whether conduct rises to the level of fraud is for courts to determine.

What is the TCPA statute of limitations?

Generally, you have four years to bring a federal TCPA claim from the date of the violation. Don’t wait — document your evidence now and consult an attorney.

What happened with the trademark lawsuit against Symple Lending?

Law firm Troutman Amin, LLP sued Symple Lending for using a confusingly similar lion logo. A federal court initially issued a Temporary Restraining Order but later declined to grant a preliminary injunction, finding it unlikely that consumers would confuse a law firm with a loan company. The case continues. money metals exchange lawsuit

Did Symple Lending’s founder really get an FTC injunction?

Yes. Public FTC records confirm that co-founder Houston Fraley was subject to a 2017 permanent injunction from an enforcement action against a prior telemarketing company (Allorey, Inc.).

Does Symple Lending actually give out loans?

Its Terms of Use describe it as a connector to third-party lenders, not a direct lender. Across major review platforms, no verified consumer review confirms actually receiving a funded loan from Symple or its lending partners, as of early 2026.

What is Symple Lending’s arbitration clause?

Symple Lending’s Terms of Use include a mandatory arbitration clause and class action waiver. Users who submit information through the website may be bound by this clause. However, it may not apply to people who were cold-texted without ever visiting the site.

How do I file a complaint against Symple Lending?

File at donotcall.gov for DNC violations, at consumerfinance.gov/complaint for lending practices, and at your state attorney general’s office for state consumer protection violations. All three create public records that support future regulatory action.

When will the Symple Lending cases settle?

There’s no way to predict this. Complex TCPA class actions can take anywhere from one to several years to resolve. Monitor PACER (federal court records) and Justia.com for updates on the three Florida cases.

What if I signed a debt settlement contract after being referred by Symple Lending?

Review the contract carefully, especially for fee disclosures. If you believe you were misled about what you were signing up for, consult a consumer protection attorney. You may have claims separate from the TCPA lawsuits.

Will I be automatically included in a class action if one settles?

If you are a member of the defined class (typically anyone who received unsolicited texts from Symple Lending during a certain period), you’ll be automatically included in a class settlement unless you opt out. You’d receive notice by mail or email when a settlement is announced.

How do I stay updated on the Symple Lending lawsuits?

Monitor PACER or Justia.com for the case dockets (Turizo: 0:2024cv61274; Betts: 0:25-cv-60114). TCPA World (tcpaworld.com) also covers TCPA litigation developments closely.

Summary: What You Need to Know

The Symple Lending lawsuit situation is active, complex, and still unfolding. Here’s the bottom line:

| Key Fact | Detail |

|---|---|

| Number of active federal lawsuits | 4 (3 TCPA class actions + 1 trademark) |

| TCPA cases filed | July 2024 – January 2025 |

| Court | S.D. Florida (TCPA cases) |

| Allegations | Illegal spam texting, bait-and-switch lending |

| Settlement status | No settlement reached as of March 2026 |

| Claim filing deadline | None yet — no settlement exists |

| Statutory damages (TCPA) | $500–$1,500 per violation |

| Founder background | Prior FTC telemarketing injunction (2017) |

| What to do now | Document evidence, file complaints, consult attorney |

If you received unwanted texts from Symple Lending or were steered into a debt settlement program you didn’t understand, take action now. Document everything, file complaints with federal and state agencies, and speak with a consumer protection or TCPA attorney — most offer free initial consultations and work on contingency.

The law exists to protect people in exactly these situations. Don’t wait for a settlement to exercise your rights.