Quick Answer: Whether your lawsuit settlement is taxable depends entirely on what it compensates you for, not just the fact that you received a check. Money from physical injury or illness is generally tax-free. Most other settlement money — lost wages, punitive damages, emotional distress from non-physical harm, and interest — is taxable as ordinary income.

If you just got a settlement check (or you’re expecting one), this guide explains exactly what you’ll owe, what you won’t, and how to avoid costly mistakes when you file. Philips CPAP Lawsuit Payout Per Person

What Are the IRS Rules on Lawsuit Settlement Taxes?

The tax treatment of a lawsuit settlement comes down to two federal laws that work together. Under IRC Section 61, the IRS considers all income taxable from whatever source derived — including money you win or settle in a lawsuit. That’s the starting point.

Then IRC Section 104 carves out specific exceptions. The most important one: money you receive for personal physical injuries or physical sickness is excluded from your gross income.

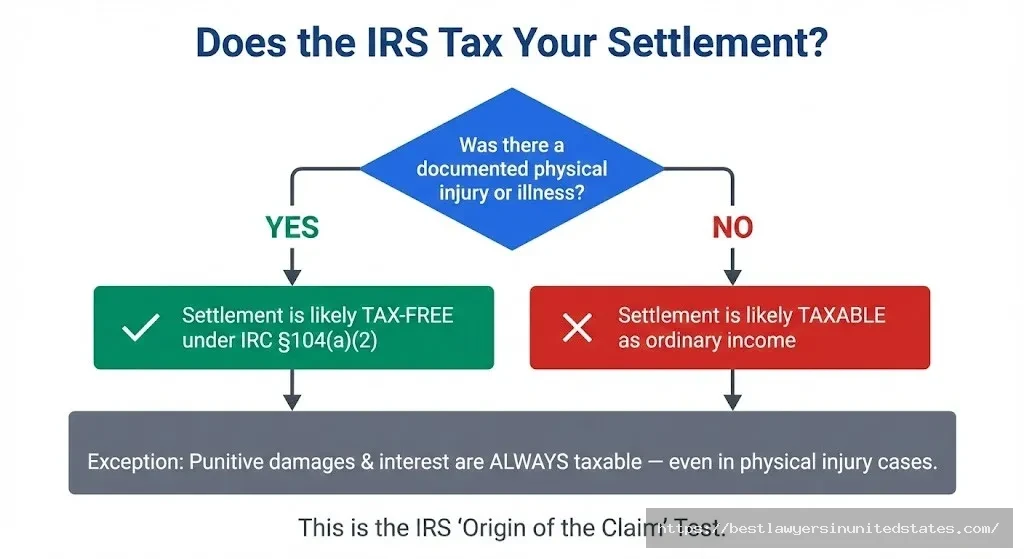

The key question the IRS asks isn’t “Did you win a lawsuit?” It asks: “What was this settlement money intended to replace?” That principle — called the origin of the claim test — determines whether you owe taxes. Facial abuse lawsuit

Here’s the practical upshot: if you were hurt in a car accident and got $50,000 for your injuries, medical bills, and related suffering, that money is almost certainly tax-free. But if you sued your employer for wrongful termination and got $50,000 for lost wages, you owe taxes on it — because lost wages replace taxable income you would have paid taxes on anyway.

Lawsuit Settlement Tax Quick Reference Table

| Settlement Type | Taxable? | IRS Form You May Receive | Where to Report |

|---|---|---|---|

| Physical injury / physical sickness damages | No | None (typically) | Not required |

| Medical expense reimbursement (if previously deducted) | Partial | 1099-MISC | Schedule 1, Line 8z |

| Emotional distress from physical injury | No | None (typically) | Not required |

| Emotional distress without physical injury | Yes | 1099-MISC | Schedule 1, Line 8z |

| Lost wages from a physical injury case | No | None (typically) | Not required |

| Lost wages from an employment case | Yes | W-2 or 1099-MISC | Form 1040, Line 1a |

| Back pay / wrongful termination | Yes | W-2 | Form 1040, Line 1a |

| Punitive damages | Always Yes | 1099-MISC | Schedule 1, Line 8z |

| Interest on a settlement | Always Yes | 1099-INT | Schedule B |

| Workers’ compensation | No | None | Not required |

| Discrimination / harassment (non-physical) | Yes | 1099-MISC | Schedule 1, Line 8z |

| Class action settlement payments | Depends on type | 1099-MISC if taxable | Varies |

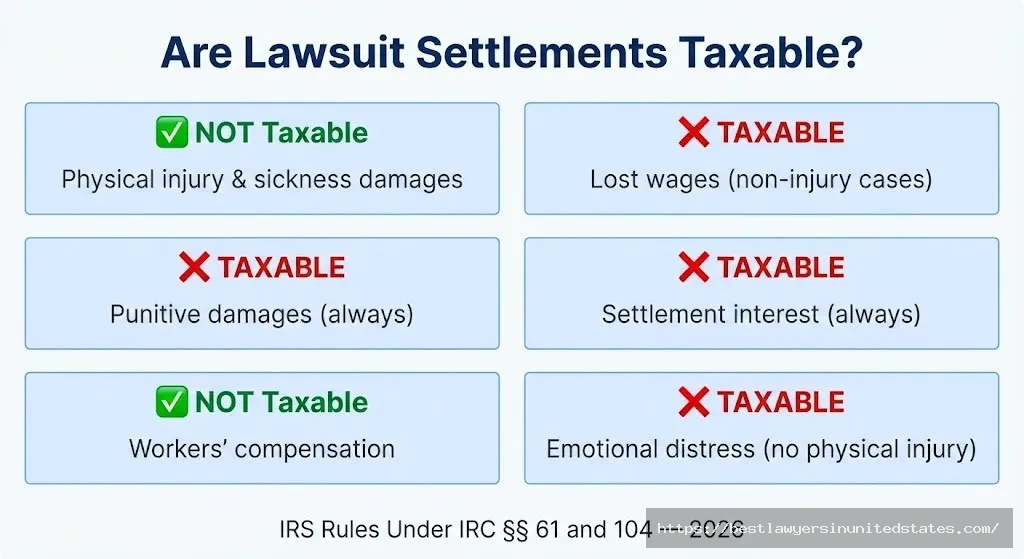

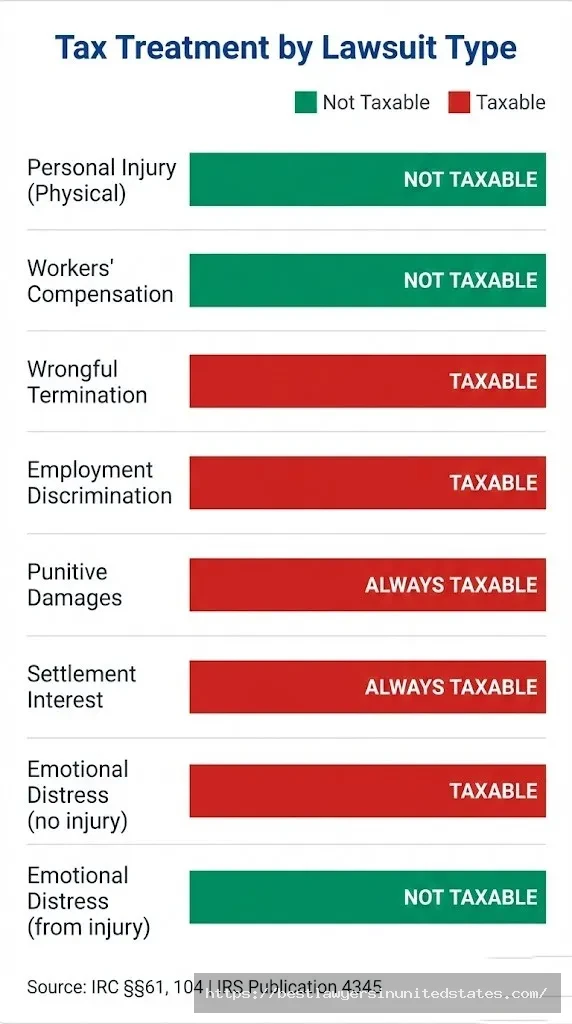

Which Lawsuit Settlements Are NOT Taxable?

Personal Physical Injury and Sickness Settlements

This is the biggest and most important exception. In most situations, personal injury settlements — such as those related to car accidents, slip and fall cases, or medical malpractice — are not considered taxable by the IRS.

The critical word here is physical. Congress added that word to the tax code in 1996, and it changed everything. Before that change, damages for emotional distress alone could be excluded from income. Today, settlements for emotional or mental injuries without a physical injury are taxable as ordinary income.

To qualify for the physical injury exclusion, the harm needs to be real and documented. To qualify for the physical injury/sickness exception, the plaintiff must show that the settlement payment was received as a result of their observable or documented bodily harm, such as bruising, cuts, swelling, or bleeding. Tepezza Lawsuit

Workers’ Compensation Benefits

In general, the IRS doesn’t consider workers’ compensation as taxable income. Workers’ compensation covers medical expenses, illness, loss of income, and disability benefits after a workplace accident.

There is one exception: if your workers’ compensation settlement includes punitive damages, those specific damages are still taxable.

Emotional Distress That Flows From a Physical Injury

If you broke your leg in an accident and also developed anxiety and depression as a result, that emotional distress compensation is tax-free — because it stems directly from a documented physical injury. Any settlement money received for emotional distress is nontaxable if the distress or anguish originated from the physical injury or sickness caused by the accident.

Which Lawsuit Settlements ARE Taxable?

Lost Wages (When No Physical Injury Is Involved)

Loss of earnings recovered in a personal injury settlement or other legal claim are not taxable when a victim sustained a physical injury. However, lost wages are taxable when there is no documented physical injury.

So if you sue your employer for wrongful termination and get back pay, every dollar gets taxed as ordinary income — plus Social Security and Medicare taxes on top of that.

Employment Discrimination and Harassment Claims

Punitive damages and awards for unlawful discrimination or harassment are taxable. If you receive compensation for back pay or unpaid wages, the IRS treats it just like income you earn on the job. It’s subject to both income and employment taxes.

This applies across the board — age, race, gender, religion, disability discrimination, and sexual harassment cases where there’s no physical injury all produce taxable income.

Punitive Damages — Always Taxable

Punitive damages are taxable as ordinary income regardless of the underlying claim. These damages do not compensate the victim for losses, even though the victim receives the payment. Instead, punitive damages “punish” the at-fault party for particularly egregious conduct.

Even if you won a personal injury case that is otherwise completely tax-free, any punitive damages in that settlement are carved out and taxed separately. You report them as “Other Income” on Schedule 1, Line 8z of your Form 1040.

Interest on Settlements — Always Taxable

Interest on settlement amounts is always taxable as interest income. Pre-judgment interest accrues while your case is pending. Post-judgment interest accumulates after a verdict until the judgment is paid. Even if your underlying damages are tax-free, any interest remains taxable.

The IRS reasons that interest compensates you for the time value of money — not for your injury — so it follows ordinary interest income rules.

Emotional Distress Without a Physical Injury

Defamation, invasion of privacy, wrongful arrest without physical force, workplace harassment that caused no physical injury — settlement money from these cases is taxable. The emotional pain was real, but the IRS draws a hard line at “physical.”

Business and Contract Disputes

Contract breach damages are taxed based on what they replace. Damages for lost profits are ordinary income. Damages for breach of a contract to sell property may produce capital gain if the underlying asset was a capital asset.

Taxability by Case Type: A Detailed Breakdown

| Case Type | Taxable? | Key Exception | Tax Treatment |

|---|---|---|---|

| Car accident / personal injury | Generally No | Must involve physical injury | Excluded under IRC 104(a)(2) |

| Slip and fall | Generally No | Must involve physical injury | Excluded under IRC 104(a)(2) |

| Medical malpractice | Generally No | Must involve physical injury | Excluded under IRC 104(a)(2) |

| Workers’ compensation | No | Watch for punitive damages | Excluded by statute |

| Wrongful termination | Yes | N/A | Ordinary income + payroll taxes |

| Employment discrimination | Yes | Physical injury exception possible | Ordinary income + payroll taxes |

| Sexual harassment (non-physical) | Yes | N/A | Ordinary income |

| Breach of contract | Yes | Capital asset exception possible | Ordinary income or capital gain |

| Property damage only | Yes | Basis recovery first | Report over asset basis |

| Defamation / libel | Yes | N/A | Ordinary income |

| Class action — consumer fraud | Yes (usually) | N/A | Ordinary income |

| Class action — product liability | Depends | Physical injury component | Mixed treatment |

The Origin of the Claim Test: How the IRS Actually Decides

You can’t just write “physical injury damages” in your settlement agreement and expect the IRS to take it at face value. The origin of the claim test determines tax treatment. The IRS looks at what the settlement was intended to replace, not simply how the payment was labeled. A settlement cannot be made tax-free simply by using specific labels.

The IRS examines the underlying lawsuit — the actual complaint, the allegations, what harm you claimed, and what the money was designed to make you whole for. This is called the “origin of the claim.”

Here’s a real-world example: You sued your employer for workplace violence — a coworker attacked you and broke your arm. You have a physical injury. Even though it’s an employment case, the physical injury exception can apply to the portion of your settlement covering that injury. However, lost wages from the same case might still be taxable.

The takeaway: How damages are described and allocated in your actual written settlement agreement matters enormously. A good attorney can work with the parties to allocate damages in ways that minimize your tax bill — legally.

When Part of Your Settlement Is Taxable and Part Isn’t

Mixed settlements are common, and they require careful allocation. Say you settled a personal injury case for $150,000, broken down as:

- $80,000 for physical injuries and medical expenses → Tax-free

- $30,000 for lost wages during recovery from physical injury → Tax-free (lost wages from physical injury are excluded)

- $25,000 for punitive damages → Taxable

- $15,000 for pre-judgment interest → Taxable

Your total taxable amount is $40,000, not $150,000.

If you have two claims against a defendant and settle for both, indicate the amount for each. For example, if one claim is personal injury-related and the other is a non-personal injury claim, one settlement is excluded from taxation while the other is not.

Allocation Table: How Mixed Settlements Are Split

| Settlement Component | Tax Treatment | Reported On |

|---|---|---|

| Physical injury compensation | Non-taxable | Nothing to report |

| Medical expense reimbursement (no prior deduction) | Non-taxable | Nothing to report |

| Medical expense reimbursement (prior deduction taken) | Taxable to extent of tax benefit | Schedule 1, Line 8z |

| Lost wages from physical injury | Non-taxable | Nothing to report |

| Lost wages from non-physical claim | Fully taxable | W-2 or Schedule 1 |

| Emotional distress from physical injury | Non-taxable | Nothing to report |

| Emotional distress from non-physical claim | Fully taxable | Schedule 1, Line 8z |

| Punitive damages | Always taxable | Schedule 1, Line 8z |

| Interest earned on settlement | Always taxable | Schedule B (Form 1040) |

The Medical Expense Deduction Rule: A Trap Most People Miss

Here’s a subtlety that trips up a lot of people. If you previously claimed medical expenses as itemized deductions on your taxes and then received a settlement that reimbursed those same medical costs, you may owe taxes on the reimbursement.

Medical visits for emotional distress or physical injury are nontaxable if you did not take an itemized deduction for these expenses in prior years. However, if you settle and are reimbursed for medical expenses after taking a deduction in previous years, you will be required to pay a tax that year; this is a specific IRS rule called the “tax benefit rule.”

You report that amount as “Other Income” on Schedule 1, Line 8z of your Form 1040. The logic is that you already got a tax benefit from deducting those costs — you can’t get a double benefit by excluding the reimbursement too.

Attorney Fees: What Happens to the Part That Goes to Your Lawyer?

This is one of the most misunderstood aspects of settlement taxation, and getting it wrong can cost you significantly.

The General Rule

In most taxable cases, the IRS treats your entire gross settlement as your income — even the portion your lawyer takes as their contingency fee. That means if you settled an employment discrimination case for $100,000 and your attorney took $40,000, the IRS generally counts $100,000 as your income.

The Good News for Physical Injury Cases

For physical injury cases, the entire amount including attorney’s fees is tax-free. So you don’t have to worry about being taxed on money that went straight to your attorney in a personal injury case.

The Above-the-Line Deduction Exception

For employment discrimination and certain other civil rights claims, IRC Section 62(a)(20) allows an above-the-line deduction preventing the fees from being trapped as unusable itemized deductions. This is a huge benefit for plaintiffs in discrimination cases specifically.

The 1099 Situation With Attorney Fees

Defendants or their insurance companies must issue a Form 1099-MISC for taxable settlement payments exceeding the IRS reporting threshold. This form reports the payment to both you and the IRS, creating a record that you received the funds.

Forms 1099-MISC and Forms W-2, as appropriate, must be filed and furnished with the plaintiff and the attorney as payee when attorney’s fees are paid pursuant to a settlement agreement that provides for payments includable in the claimant’s income, even though only one check may be issued for the attorney’s fees. That means both you and your attorney may receive a 1099 for the full settlement amount — not just your portion.

Form 1099-MISC vs. W-2: How Your Settlement Gets Reported to the IRS

How the defendant reports your settlement payment to the IRS depends on the nature of the underlying claim.

| Settlement Type | IRS Form Used | Who Issues It | Withholding? |

|---|---|---|---|

| Lost wages / back pay / front pay | W-2 | Defendant employer | Yes — income tax, Social Security, Medicare |

| Punitive damages | 1099-MISC | Defendant or insurer | Generally no |

| Non-physical emotional distress | 1099-MISC | Defendant or insurer | Generally no |

| Interest on settlement | 1099-INT | Defendant or insurer | Generally no |

| Physical injury (non-taxable) | None typically | N/A | No |

| Attorney gross proceeds | 1099-MISC Box 10 | Defendant or insurer | No |

Important for 2026: The IRS reporting threshold for Form 1099-MISC and 1099-NEC has been raised from $600 to $2,000 for payments made starting in the 2026 tax year. This affects lower-value settlement payments but does not change the underlying tax rules.

Payments expressly designated for non-taxable physical injury damages are excluded from 1099 reporting requirements. If your entire settlement qualifies for the physical injury exclusion, you may not receive a 1099 at all. However, this does not change your obligation to accurately report income on your tax return. Zicam Lawsuit

How to Reduce Your Tax Bill on a Settlement: Legal Strategies

1. Negotiate the Allocation Language in Your Settlement Agreement

How damages are described in the settlement can have an impact on your tax bill. It’s helpful to specify which portion of a split settlement is for physical injuries versus emotional distress or lost wages. In negotiating a settlement, it may be possible to stipulate that an award is for physical injuries, rather than emotional, and thus is nontaxable.

Work with your attorney early to get this language right. Once you sign, it’s very hard to change how the IRS views the allocation.

2. Consider a Structured Settlement

Instead of a lump sum, structured settlements spread your payments over time. For taxable settlements, this can lower your annual tax burden and potentially push some payments into lower-income years when your tax rate is smaller.

3. Check Whether the Above-the-Line Attorney Fee Deduction Applies

If your case involved employment discrimination or specific civil rights claims, your attorney fees may be fully deductible above the line, which reduces your adjusted gross income even if you take the standard deduction.

4. Use a Plaintiff Recovery Trust (for Larger Settlements)

For significant taxable settlements, certain legal structures like qualified settlement funds or plaintiff recovery trusts can delay the tax event and provide flexibility in how proceeds are invested and distributed. This is worth exploring with a financial planner or tax attorney for settlements above $100,000.

5. Plan for Estimated Tax Payments

Some settlement recipients may need to make estimated tax payments if they expect their tax to be $1,000 or more after subtracting credits and withholding. If no withholding was taken from your settlement (which is common with 1099-MISC payments), you could owe a penalty if you wait until April to pay. File Form 1040-ES quarterly.

Tax Strategies Comparison Table

| Strategy | Best For | Potential Tax Savings | Complexity |

|---|---|---|---|

| Negotiate physical injury allocation | Mixed-damage cases | High — can make large portions tax-free | Low — requires good attorney |

| Structured settlement annuity | Large taxable settlements | Moderate — spreads tax over years | Medium |

| Above-the-line attorney fee deduction | Discrimination / civil rights cases | Medium — offsets gross income | Low |

| Plaintiff Recovery Trust | Settlements over $100K | High — tax deferral and flexibility | High — requires specialist |

| Estimated quarterly tax payments | Any taxable settlement | Avoids 5% underpayment penalty | Low |

Employment Lawsuits: A Closer Look at the Tax Rules

Employment cases deserve special attention because they’re so common and the tax rules are specific.

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable from gross income unless a personal physical injury caused such loss.

Back pay and front pay are treated as wages. That means your former employer must process them through payroll with withholding for income tax, Social Security, and Medicare — just like a regular paycheck. You’ll get a W-2, not a 1099.

Punitive damages in employment cases get a separate 1099-MISC and are taxed as ordinary income.

One exception worth knowing: if a workplace incident caused actual physical harm — a supervisor assaulted you, you developed a stress-induced physical illness, a workplace accident injured you — those physical injury damages may qualify for the exclusion even in an employment lawsuit context.

Class Action Settlements: Special Rules

Class action settlements often involve small individual payouts, and many people assume that makes them tax-free. That’s not how it works.

The tax treatment of a class action settlement follows the same origin of the claim rules. A few common scenarios:

Consumer fraud / deceptive practices class actions — Usually taxable, because the money replaces economic losses or reimburses overcharges, not physical injury. If you receive a $25 check from a data breach settlement, that’s technically taxable income, though many people don’t report small amounts.

Product liability class actions involving physical injury — The portion for physical injuries and medical expenses is generally tax-free. Any punitive damages are taxable.

Securities class actions — These are typically taxable because they compensate for investment losses, which follow capital gains rules. Consult a CPA for these.

Data breach settlements — Generally taxable as ordinary income to the extent they exceed documented losses. Pure emotional distress damages in data breach cases (without physical injury) are taxable.

State Taxes on Lawsuit Settlements

Federal rules get most of the attention, but your state may have different rules — or no income tax at all.

| State Tax Situation | What It Means for You |

|---|---|

| No state income tax (TX, FL, WA, NV, WY, SD, AK, TN, NH) | Only federal rules apply to your settlement |

| State follows federal exclusions (most states) | Physical injury settlements are state-tax-free too |

| State has its own rules (a few states) | You may owe state tax even on federally-excluded amounts |

| High-tax states (CA, NY, NJ, OR) | Taxable settlements face high combined rates — plan accordingly |

California and New York residents face particularly high state income tax rates on taxable settlements — up to 13.3% in California on top of federal rates. If you’re in one of those states, tax planning before you sign a settlement agreement is especially valuable.

Frequently Asked Questions

Are personal injury settlements taxable?

Quick Answer: No — physical injury settlements are generally tax-free under IRC Section 104(a)(2).

The money you receive for physical injuries, medical bills, pain and suffering, and even emotional distress connected to those physical injuries is excluded from your gross income. The key is that the harm must be physical and documented. You don’t need to report this money on your tax return, and you typically won’t receive a Form 1099 for it.

Do I have to pay taxes on a settlement for emotional distress?

Quick Answer: It depends on whether your emotional distress stems from a physical injury or not.

If your anxiety, depression, or emotional suffering was caused by documented physical injuries — a car accident, workplace assault, etc. — that portion of your settlement is tax-free. If the emotional distress comes from non-physical harm like harassment, defamation, or wrongful termination, it’s taxable as ordinary income.

Are punitive damages taxable?

Quick Answer: Yes, always — punitive damages are taxable under federal law regardless of the type of case.

Even if your entire personal injury settlement is tax-free, punitive damages within that same settlement are carved out and taxed. Report them as “Other Income” on Schedule 1, Line 8z of your Form 1040.

Is interest on a lawsuit settlement taxable?

Quick Answer: Yes — interest is always taxable, even when the underlying settlement is not.

Pre-judgment and post-judgment interest are both treated as ordinary interest income and reported on Schedule B. There are no exceptions to this rule.

Are wrongful termination settlements taxable?

Quick Answer: Yes — wrongful termination and back pay settlements are fully taxable as wages.

You’ll receive a W-2 from your former employer for these payments (or, if they didn’t withhold, a 1099 and a potentially large surprise tax bill). The money replaces wages you would have paid taxes on anyway, so the IRS taxes it the same way.

Will I receive a Form 1099 for my settlement?

Quick Answer: You’ll get a 1099 for taxable settlement payments above the reporting threshold, but not for non-taxable physical injury settlements.

For 2025 tax year payments: the 1099 reporting threshold is $600. For 2026 tax year payments, the threshold has been raised to $2,000 under the One Big Beautiful Bill Act. If you receive a 1099 and believe your settlement is non-taxable, you still need to report it on your return and explain the exclusion — don’t just ignore it.

What if I didn’t receive a 1099 — do I still owe taxes?

Quick Answer: Yes. Not receiving a 1099 doesn’t mean your settlement is tax-free or that you don’t need to report it.

The IRS may still have records of the payment from the defendant’s reporting. And even if they don’t, you’re legally required to report all taxable income regardless of whether paperwork was issued. Failing to report taxable settlement income can trigger penalties, interest, and potentially audit scrutiny.

Are workers’ compensation settlements taxable?

Quick Answer: No — workers’ compensation benefits and settlements are not taxable at the federal level.

This applies to payments for medical expenses, disability, and lost wages from work injuries. One exception: if your workers’ comp settlement includes punitive damages, those specific damages are taxable. Workers’ comp that reduces Social Security disability benefits may also be partially taxable under different rules.

What about class action settlement checks — do I pay taxes?

Quick Answer: Usually yes, though it depends on the nature of the underlying claim.

Small consumer settlement checks (like a $25 refund from a product recall) are technically taxable income. Most people don’t report these small amounts, but strictly speaking you’re required to. Larger class action settlements, particularly those involving investment losses or consumer fraud, should be reported. Physical injury class actions are treated the same as individual injury cases.

Can I deduct my attorney fees from a taxable settlement?

Quick Answer: It depends on the type of case, and post-2018 rules make this harder.

For physical injury cases, the entire settlement including attorney fees is tax-free, so this question doesn’t apply. For employment discrimination and civil rights cases, attorney fees may be deductible above the line under IRC Section 62(a)(20), which is valuable. For most other taxable settlements, attorney fees are generally no longer deductible as itemized deductions for individual taxpayers. A tax professional can help you determine what applies to your specific situation.

How do I report a taxable settlement on my taxes?

Quick Answer: Taxable settlements are reported in different places depending on the type.

Employment-related payments (wages, back pay) go on Line 1a of Form 1040, typically reflected on a W-2. Other taxable settlements (punitive damages, non-physical emotional distress, interest) go on Schedule 1 as “Other Income” on Line 8z. Interest specifically goes on Schedule B. Your settlement administrator or the defendant’s insurer should send you the appropriate forms, but don’t wait for paperwork to confirm what you owe.

What happens if I don’t report my settlement income?

Quick Answer: You risk IRS penalties, interest on unpaid taxes, and potentially an audit.

The IRS receives copies of all 1099s and W-2s issued. If you received a 1099 for settlement income and don’t report it, there will be a mismatch in IRS records that can trigger a notice automatically. Penalties can include 20-25% of the unpaid tax plus interest from the due date. In cases of willful non-reporting, more serious consequences are possible.

Does the One Big Beautiful Bill Act (2025) change how settlements are taxed?

Quick Answer: The core settlement tax rules haven’t changed, but the reporting thresholds and tax brackets have.

The One Big Beautiful Bill, which became law in 2025, raised the 1099 reporting threshold from $600 to $2,000 for many payments starting in the 2026 tax year. It also updated income tax brackets. The fundamental rules under IRC Section 104 — which govern what settlements are tax-free — remain in place. If you have a large pending settlement, updated tax projections using 2026 OBBBA brackets may show different after-tax results than older estimates.

Should I talk to a tax professional about my settlement?

Quick Answer: Yes, particularly for any settlement over $10,000 or involving mixed types of damages.

Without professional guidance, you could miss opportunities to minimize your tax liability or, worse, end up underreporting income. A CPA or tax attorney can review your settlement agreement, identify which portions are taxable and non-taxable, advise on attorney fee treatment, and help you avoid estimated tax penalties. The cost of an hour with a tax professional is usually a small fraction of the potential tax savings in a meaningful settlement.

Can I negotiate my settlement to reduce taxes?

Quick Answer: Yes — the allocation language in your settlement agreement can make a real difference.

In negotiating a settlement, it may be possible to stipulate that an award is for physical injuries, rather than emotional, and thus is nontaxable. Both parties need to agree to the allocation, and the IRS won’t honor allocations that don’t reflect the actual claims, but working with your attorney to appropriately document the true nature of each payment component is entirely legitimate and often valuable.

Are settlements from property damage lawsuits taxable?

Quick Answer: Property damage settlements are generally taxable to the extent they exceed your adjusted basis in the property.

If your $20,000 car was totaled and you received $20,000, there’s no taxable gain. But if you received more than the property’s basis (its value for tax purposes), the excess could be taxable. Consult a tax advisor if you received a settlement substantially above the property’s market value.

What if I receive a settlement from a wrongful death lawsuit?

Quick Answer: Wrongful death settlements are generally tax-free for the beneficiaries under IRC Section 104.

Compensation received on account of the wrongful death of a family member, including damages for loss of support and companionship, is generally excluded from income. Punitive damages are the exception — those remain taxable even in wrongful death cases, except in states where wrongful death statutes allow only punitive damages, which may receive special treatment under IRC Section 104(c).

Documentation Checklist: What to Keep for Tax Purposes

Keeping good records now saves significant headaches later — especially if the IRS has questions.

| Document | Why You Need It | Where to Get It |

|---|---|---|

| Settlement agreement | Shows how damages were allocated | Your attorney |

| Original complaint / petition | Shows the nature of the underlying claim | Court records / your attorney |

| Form 1099-MISC or W-2 | Official income reporting document | Defendant or insurer (by Feb 17, 2026 for 2025 payments) |

| Medical records related to your injury | Proves physical injury for tax exclusion | Your healthcare providers |

| Prior year tax returns (if medical deductions claimed) | Needed for tax benefit rule analysis | IRS account / your records |

| Attorney fee agreement | Documents amount paid in fees | Your attorney |

| Proof of payment / deposit | Confirms when you received the money | Bank records |

| Correspondence with settlement administrator | Documents any non-taxable designations | Email / mail records |

Bottom Line: The 4 Questions That Determine Your Tax Bill

When you’re trying to figure out whether your settlement is taxable, run through these four questions in order:

1. Was there a documented physical injury or physical illness? If yes, the money compensating for that physical harm is very likely tax-free.

2. What was each component of the settlement designed to replace? Lost wages replace taxable income → taxable. Medical bills for physical injury → not taxable. Punitive damages → always taxable.

3. How is the settlement agreement written? Allocation language matters. Vague agreements give the IRS more room to interpret things against you.

4. Were any prior medical expenses deducted on past returns? If yes, reimbursement for those specific expenses may be taxable under the tax benefit rule.

If you’re working through a complex settlement — especially one with multiple types of damages, large amounts, or a mix of taxable and non-taxable components — getting a qualified tax advisor involved before you sign the agreement is the single best investment you can make.

This article is for informational purposes only and does not constitute tax or legal advice. Tax laws can vary by state and individual circumstance. Please consult a qualified CPA or tax attorney regarding your specific settlement situation.

Sources: IRS Publication 4345 (Settlements – Taxability); IRC Sections 61 and 104; IRS Tax Implications of Settlements and Judgments guidance; IRS Form 1099-MISC Instructions (2025/2026).

Comments