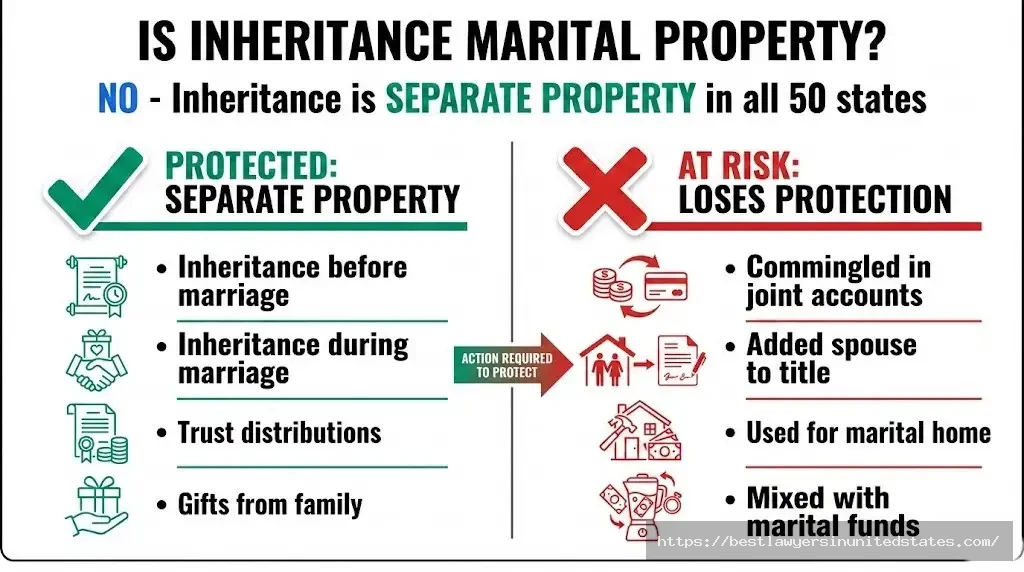

Will your spouse get half of your inheritance if you divorce? In most cases, no. Inheritance is separate property that belongs only to the spouse who received it. However, you can lose this protection if you mix inherited money with marital funds or add your spouse’s name to inherited property.

Protecting an inheritance during divorce requires careful planning and documentation. Many people accidentally convert their separate inheritance into marital property through common mistakes like depositing funds in joint accounts. Understanding how inheritance laws work can save you thousands of dollars and preserve your family’s legacy.

This guide explains when inheritance becomes marital property, how to protect inherited assets, and what happens to inheritance in different divorce scenarios. You’ll learn state-specific rules, common mistakes to avoid, and action steps to take right now.

Is Inheritance Marital Property? Understanding the Basics

No, inheritance is not marital property in the United States. Federal and state laws classify inheritance as separate property that belongs exclusively to the spouse who received it. This applies whether you inherited before marriage or during marriage.

The legal principle comes from the doctrine of “gift, devise, or descent.” When someone leaves you property through a will or trust, that asset is yours alone. Courts cannot divide your separate property in divorce unless you voluntarily converted it to marital property.

The General Rule: Inheritance as Separate Property

Inheritance follows a simple rule across all 50 states. Property you receive as a gift or through a will belongs only to you. Your spouse has no automatic claim to it in divorce.

This protection applies to multiple types of inherited assets:

Protected inheritance assets:

- Cash and bank accounts from estates

- Real estate inherited from family

- Stocks, bonds, and investment accounts

- Family businesses passed down

- Personal property and heirlooms

- Trust distributions naming you as beneficiary

The key is keeping these assets separate from marital property. Once you mix inheritance with shared assets, you risk losing protection.

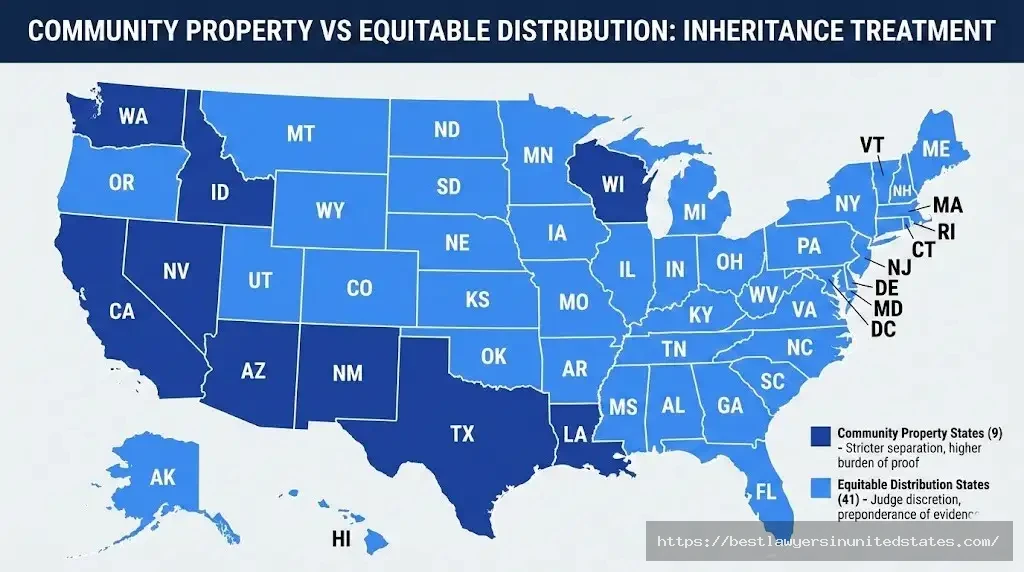

Community Property vs Equitable Distribution States

The United States has two property division systems that affect how courts handle inheritance. Community property states split marital assets 50/50, while equitable distribution states divide property fairly (not necessarily equally).

Community property states (9 total):

- California

- Texas

- Arizona

- Nevada

- New Mexico

- Idaho

- Wisconsin

- Louisiana

- Washington

All other states use equitable distribution. The difference matters because community property states have stricter rules about what counts as separate versus community property. Inheritance remains separate in both systems, but the burden of proof varies.

| Property System | States | Inheritance Treatment | Burden of Proof |

|---|---|---|---|

| Community Property | 9 states | Separate unless commingled | Clear and convincing evidence (TX) |

| Equitable Distribution | 41 states + DC | Separate but subject to tracing | Preponderance of evidence |

In community property states like California and Texas, you must prove your inheritance meets the legal definition of separate property. Courts presume all assets acquired during marriage are community property unless you can show otherwise.

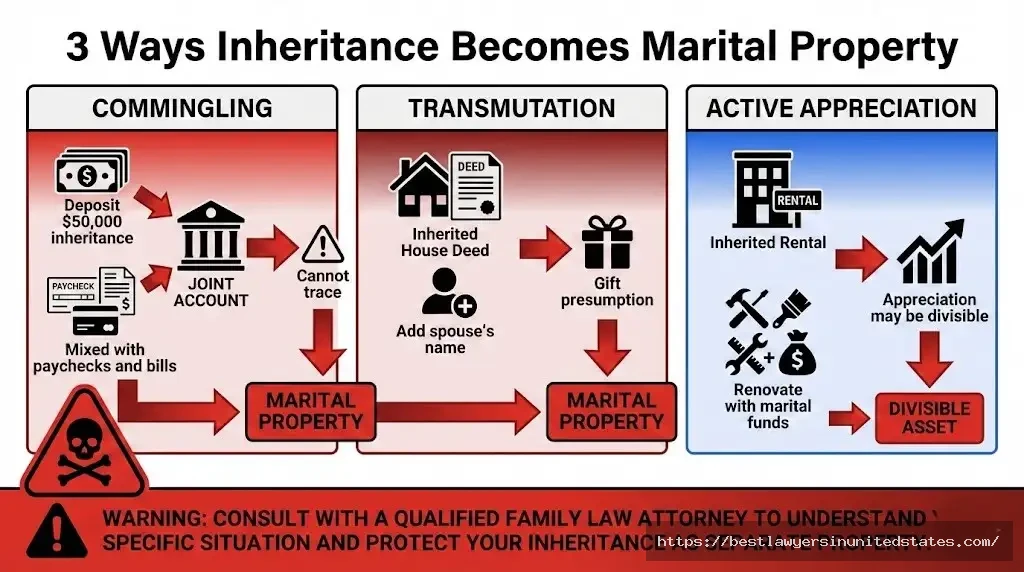

When Does Inheritance Become Marital Property?

Inheritance loses protected status through three main actions: commingling, transmutation, and active appreciation. Each of these can convert your separate inheritance into divisible marital property.

Most people lose inheritance protection accidentally. They deposit inherited money in a joint checking account for “convenience” or use inheritance funds to renovate the marital home. These seemingly innocent actions can cost you half of your inheritance in divorce.

The timing of when you received the inheritance doesn’t change these risks. Whether you inherited property 10 years before marriage or last month, the same rules apply. Protection depends on how you handle the assets after receiving them.

How Inheritance Loses Protected Status (And Becomes Marital Property)

The most common way to lose inheritance protection is through commingling, which happens when you mix inherited money with marital funds. Courts call this “hopeless commingling” when the assets become so mixed that you cannot trace them back to the original inheritance.

You bear the burden of proving your inheritance remained separate. Without clear documentation showing an unbroken chain from the inheritance to your current account, courts will treat the mixed funds as marital property subject to property division.

Commingling: Mixing Inheritance With Marital Assets

Commingling occurs when separate property combines with marital property until they cannot be distinguished. The classic example is depositing a $50,000 inheritance check into your joint checking account with your spouse.

Once that money hits the joint account, it mixes with paychecks, bill payments, and other marital income. After a few months of transactions, you cannot prove which dollars came from your inheritance and which came from marital earnings.

Common commingling mistakes:

- Depositing inheritance in joint bank accounts

- Using joint account for inheritance investments

- Paying marital bills from inheritance account

- Transferring money between separate and joint accounts

- Using inheritance for shared expenses

The solution is simple but requires discipline. Keep inherited money in an account with only your name on it. Never use that account for anything except the inherited funds and their investment growth.

Example scenario: Sarah inherits $100,000 from her grandmother. She deposits it in a joint savings account “just temporarily” while she decides what to do with it. Over the next year, she and her husband use the account to pay for a vacation ($8,000), home repairs ($15,000), and their daughter’s college tuition ($20,000). When Sarah files for divorce two years later, she cannot prove which of the remaining $57,000 came from her inheritance versus marital contributions. The entire account is now marital property.

Transmutation: Converting Separate Property to Marital

Transmutation is the legal process of changing property from separate to marital status through intentional actions or documents. This often happens when you add your spouse’s name to an inherited asset or use inheritance to purchase jointly-titled property.

Courts presume you intended to make a gift to the marriage when you take these actions. Proving otherwise requires strong evidence that you never meant to share the inheritance.

Intentional transmutation examples:

- Adding spouse’s name to inherited house deed

- Buying a car with inheritance titled in both names

- Using inheritance for marital home down payment with joint ownership

- Signing documents stating inheritance is “our property”

Some states require written agreements for transmutation. California law demands a written statement expressing intent to change property character. Other states allow transmutation through actions alone.

Unintentional transmutation risks: You might transmute property without realizing it. Refinancing an inherited house and adding your spouse to the new mortgage can create a transmutation argument. Using marital funds to pay the mortgage on your inherited rental property might give your spouse a partial interest.

| Action | Risk Level | Transmutation Likelihood |

|---|---|---|

| Add spouse to inherited house deed | EXTREME | Very high |

| Use inheritance for joint home down payment | HIGH | High |

| Pay inherited property taxes from joint account | MEDIUM | Moderate |

| Keep inheritance in separate account | NONE | None |

The safest approach is never adding your spouse’s name to any inherited asset. If you want your spouse to inherit the property after your death, use beneficiary designations or your estate plan instead.

Appreciation: When Inherited Assets Grow in Value

Courts distinguish between passive appreciation and active appreciation of inherited property. Passive appreciation stays separate property. Active appreciation using marital effort or funds may become divisible.

Passive appreciation happens when market forces increase an asset’s value. If you inherit $50,000 in stocks that grow to $75,000 through market gains alone, the entire $75,000 remains your separate property.

Active appreciation occurs when marital labor or money improves the asset’s value. The increase in value may be subject to division even if the underlying asset stays separate.

Passive appreciation examples (remains separate):

- Inherited stock portfolio grows through market gains

- Rental property value increases due to neighborhood development

- Art collection appreciates from artist becoming famous

- Land value rises from nearby infrastructure improvements

Active appreciation examples (may be divisible):

- You manage inherited rental properties (marital labor)

- Spouse renovates inherited house (marital effort)

- Marital funds used for inherited business improvements

- Both spouses work in inherited family business

California uses the Pereira and Van Camp formulas to calculate how much appreciation is marital versus separate. These complex formulas consider the rate of return, time involved, and contribution of marital effort.

Using Marital Funds to Maintain or Improve Inherited Property

Paying for inherited property expenses with marital money creates a reimbursement claim or partial ownership interest for your spouse. Even if the property title stays in your name alone, your spouse may get a share based on marital contributions.

This issue arises frequently with inherited houses. You inherit your parents’ home but pay the mortgage, property taxes, insurance, and maintenance from your salary (marital income). Over 10 years, you might spend $100,000 in marital funds on the property.

Marital contributions to separate property:

- Mortgage payments from salary

- Property taxes from joint accounts

- Major renovations using marital savings

- Business capital improvements

- Property insurance premiums

Courts handle this differently by state. California Family Code Section 2640 gives a reimbursement right for separate property contributions to community property (and vice versa). You might get credit for marital funds spent but not actual ownership.

Other states give the contributing spouse an ownership percentage. If marital funds paid half the mortgage over 15 years, your spouse might get a 25% interest in the property.

Protection strategy: If you inherit property with ongoing expenses, pay those expenses from the property’s own income (rental payments, business profits) or from your separate inheritance account. Never pay inherited property costs from joint accounts or marital income.

Titling Inherited Property in Spouse’s Name

Adding your spouse’s name to inherited property creates a strong presumption you intended to make a gift. Courts will likely treat the property as marital even if you claim you only added the name “for convenience” or “estate planning purposes.”

This mistake happens often with inherited real estate. You inherit a house and decide to add your spouse to the deed so they can access it if something happens to you. That action probably just converted your separate inheritance into marital property.

Re-titling scenarios that create gift presumption:

- Adding spouse as co-owner on inherited house deed

- Retitling inherited car in both names

- Making spouse joint owner of inherited bank account

- Adding spouse as co-trustee with withdrawal rights

The better approach is keeping property titled in your name alone and using estate planning tools like beneficiary designations, transfer-on-death deeds, or your will to provide for your spouse after your death.

Placing Inheritance in LLC or Business Entity

Creating a business entity and transferring inherited property into it can accidentally convert separate property to marital. This sophisticated mistake catches even people trying to protect their inheritance.

Here’s how it happens: You inherit a commercial building worth $500,000. Your attorney advises forming an LLC for liability protection. You create “Smith Properties LLC” during your marriage and deed the building to the LLC.

The problem is you no longer own the building. You own an interest in an LLC that was formed during the marriage. That LLC interest is presumed to be community or marital property in most states. You lost the separate property character of the underlying real estate.

LLC and business entity risks:

- LLC formed during marriage presumed marital

- Partnership interests created during marriage

- S-corporation stock issued during marriage

- Trust interests established during marriage

If you need liability protection for inherited property, consult both a family law attorney and a business attorney before creating any entities. Some states allow you to preserve separate property character with proper documentation, but the rules are technical and vary by jurisdiction.

State-Specific Inheritance and Divorce Laws

State law governs how courts treat inheritance in divorce, and the rules vary significantly across the country. Understanding your state’s approach is critical for protecting inherited assets.

The biggest distinction is between community property states and equitable distribution states. But even within each category, states handle inheritance issues differently. Some have strict tracing requirements. Others give judges broad discretion to divide any property.

California Inheritance Laws in Divorce

California treats inheritance as separate property under Family Code Section 770. Property acquired by “gift, bequest, devise, or descent” belongs to the receiving spouse alone. This applies whether you inherited before or during marriage.

However, California has a strong community property presumption for assets acquired during marriage. You must prove your inheritance meets the separate property definition with “clear and convincing evidence” in some cases.

California’s key inheritance rules:

- California Family Code Section 770: defines separate property

- Section 2640: reimbursement rights for separate property contributions

- Pereira/Van Camp formulas: calculate appreciation on separate property

- Transmutation requires written agreement (Section 852)

California courts use complex formulas when separate property appreciates through community effort. The Pereira formula applies when the business or property is inherently separate. The Van Camp formula applies when community labor drove appreciation.

Example: You inherit a rental property in California worth $300,000. During your 10-year marriage, you actively manage it, making improvements with marital funds. The property is now worth $500,000. The $200,000 appreciation might be partially community property under Pereira or Van Camp analysis.

California also requires tracing. You must show an unbroken chain of documentation from the original inheritance to the current asset. Missing bank statements or unclear transfers can doom your claim.

Texas Inheritance and Divorce (Texas Family Code 3.001)

Texas Family Code Section 3.001 defines inheritance as separate property acquired by “gift, devise, or descent.” Texas is a community property state with strong protections for inherited assets.

The burden of proof in Texas is “clear and convincing evidence.” This is a higher standard than in many states. You must provide strong documentation that your asset is inherited and you kept it separate.

Texas inheritance laws:

- Section 3.001: separate property definition

- Section 3.002: community property presumption

- Inception of title rule: character determined when acquired

- Income from separate property is community property

Texas has a unique rule about income. Even though your inherited property is separate, the income it generates during marriage is community property. Rent from an inherited rental house is community property. Dividends from inherited stocks are community property.

Texas also uses the “inception of title” doctrine. Property character is determined when you first acquire it. If you inherit a house before marriage, it’s separate property. If the house appreciates through market forces alone, all appreciation is separate. But if you use community funds or labor to improve it, that creates a community claim.

Commingling in Texas: Texas courts have held that depositing inherited funds in a joint account can commingle them beyond tracing. One case found a $300,000 inheritance became community property after it sat in a joint account for several years with regular deposits and withdrawals.

Florida Inheritance in Equitable Distribution

Florida Statute 61.075 governs property division in divorce using equitable distribution principles. Inheritance is separate property (called “non-marital property” in Florida) and not subject to division in most cases.

Florida courts distinguish between active and passive appreciation of separate property. Passive appreciation stays non-marital. Active appreciation from marital labor or funds may become marital property.

Florida inheritance rules:

- Statute 61.075: equitable distribution factors

- Non-marital property: includes inheritance and gifts

- Active appreciation: may be marital if spouse contributed

- Passive appreciation: remains non-marital

Florida judges have broad discretion in equitable distribution. They consider factors like marriage length, economic circumstances, and contributions to the marriage. A judge might not divide inheritance but could award more marital property to a spouse to balance the separate inheritance.

Florida commingling: Florida courts require clear tracing to prove separate property. If you deposit inheritance in a joint account and cannot trace the specific funds, the entire account becomes marital property. Florida cases have been strict on this requirement.

Active vs passive appreciation example: You inherit a house in Florida worth $200,000. Ten years later it’s worth $350,000. If appreciation came from market forces alone, all $350,000 is non-marital. If your spouse renovated the kitchen and bathrooms using marital funds and the renovations added $75,000 in value, that $75,000 might be marital property.

New York Inheritance and Equitable Distribution

New York Domestic Relations Law Section 236(B) classifies inheritance as separate property not subject to equitable distribution. Property acquired “by bequest, devise, or descent” or as a gift from someone other than the spouse is separate.

New York courts have strict tracing requirements. You must show the inheritance source and prove you kept it separate. Missing documentation can result in losing separate property status.

New York inheritance laws:

- DRL Section 236(B): separate property definition

- Strict tracing requirements

- Appreciation of separate property complex

- Marital waste doctrine applies

New York uses the “source of funds” rule for property purchased with mixed funds. If you buy a house using $50,000 inheritance and $150,000 marital funds, the house is part separate and part marital in proportion to the contributions.

Appreciation in New York: If separate property appreciates due to marital contributions or labor, the appreciation may be marital property. Courts look at whether the spouse’s efforts were “significant and direct.”

Marital waste: New York recognizes the marital waste doctrine. If you dissipate (waste) marital assets, the court can charge that back to you. However, spending your own inheritance is not marital waste since it’s separate property.

Understanding Your State’s Inheritance Laws

The other 46 states each have unique rules about inheritance and divorce. Most follow either community property or equitable distribution principles, but the details vary.

| State | Property System | Key Statute | Special Rules |

|---|---|---|---|

| Arizona | Community Property | A.R.S. § 25-211 | Income from separate property is community |

| Nevada | Community Property | NRS 123.130 | Commingling rules strict |

| Illinois | Equitable Distribution | 750 ILCS 5/503 | Non-marital property definition |

| Pennsylvania | Equitable Distribution | 23 Pa.C.S. § 3501 | Appreciation rules complex |

If you have a significant inheritance, research your specific state’s laws or consult a family law attorney. Some states have easier tracing requirements. Others give judges more discretion to divide assets regardless of source.

Quick reference for inheritance protection:

- Community property states: 9 total (stricter rules, higher burden of proof)

- Equitable distribution states: 41 + DC (judge discretion varies widely)

- All states: inheritance is separate property if kept separate

- All states: commingling risks losing protection

Understanding your state’s approach to divorce and property division is the first step in protecting your inheritance. The second step is taking action to keep inherited assets completely separate from marital property.

How to Protect Your Inheritance From Divorce: 8 Essential Strategies

The best inheritance protection starts the moment you receive the assets. Waiting even a few weeks can lead to mistakes that cost you thousands of dollars. Follow these eight strategies to safeguard inherited property from divorce claims.

Most inheritance protection failures come from lack of knowledge, not bad intent. People deposit checks in joint accounts because they don’t realize the risk. They add a spouse’s name to property for estate planning without understanding the consequences. These strategies will help you avoid common mistakes.

Strategy 1: Keep Inheritance in Separate Account (ALWAYS)

Open a bank account in your name only within 48 hours of receiving an inheritance. This separate account should never have your spouse as a co-owner or authorized user. Use it exclusively for inherited funds and their investment growth.

This is the single most important protection step. A separate account creates a clear paper trail from the inheritance source to the current balance. Courts can trace the funds without dispute.

Separate account rules:

- Account title: Your name only (never joint)

- Deposits: Only inheritance funds and investment returns

- Withdrawals: Only for separate property purposes

- No marital income: Never deposit paychecks or joint funds

- Statements: Keep every monthly statement forever

- Online access: Spouse should not have login credentials

What to do immediately:

- Call your bank and open a new savings or checking account

- Request account be in your name only

- Deposit the inheritance check directly

- Set up separate online banking access

- Store account information privately

- Never share account access with spouse

If you already deposited inheritance in a joint account, move it to a separate account immediately. The longer it sits in joint accounts, the harder tracing becomes. Document the transfer with a memo explaining you’re segregating your inheritance.

Strategy 2: Maintain Meticulous Documentation

Keep every document related to your inheritance in both digital and physical form. Years from now during a contested divorce, you’ll need to prove the source and separation of these funds.

Courts require you to trace inheritance from its source to the current asset. Missing even one bank statement can break the chain and cost you the entire inheritance protection.

Required inheritance documentation:

At inheritance:

- Copy of will or trust naming you as beneficiary

- Death certificate of deceased family member

- Estate distribution documents

- Letter from executor or trustee

- IRS Form 1099 for estate distributions

- Initial deposit receipt

Ongoing:

- Monthly bank statements (every single one)

- Investment account statements

- Property deeds and titles

- Appraisal documents

- Tax returns showing separate property

- Photos of inherited personal property

Organization system:

- Create folder: “Inheritance from [Name] – [Year]”

- Scan all documents to cloud storage

- Keep physical copies in fireproof safe

- Organize chronologically

- Update folder quarterly

- Share location with trusted family member (not spouse)

Digital backup strategy: Upload scanned documents to a secure cloud service like Google Drive or Dropbox. Create a folder structure that makes sense: “Inheritance > Estate Documents,” “Inheritance > Bank Statements > 2026,” “Inheritance > Property Documents.” Set reminders to scan and upload new statements monthly.

Strategy 3: Prenuptial Agreement With Inheritance Clause

A prenuptial agreement is the strongest legal protection for inheritance, but it only works before marriage. The agreement must explicitly protect current and future inheritances with clear language that both parties understand.

Prenups override state default property division rules. A well-written agreement can protect inheritance received during marriage and ensure it stays separate regardless of how you handle it.

Effective inheritance clause language:

- “All property received by either party by gift, bequest, devise, or descent shall remain the separate property of the recipient spouse”

- “Inheritance shall retain its separate character regardless of commingling or transmutation”

- “Each party waives all claims to the other party’s inherited property”

- “Inheritance includes principal and all appreciation, income, and proceeds”

Prenup requirements for enforceability:

- Written agreement signed by both parties

- Full financial disclosure by both parties

- Independent attorney for each spouse

- Signed well before wedding (30+ days minimum)

- No coercion or duress

- Fair and reasonable terms

- Consideration (each party gets something)

Timing matters: Don’t present a prenup one week before the wedding. Courts can invalidate agreements signed under pressure. Start prenup discussions at least three months before marriage. Give your future spouse time to review it with their own attorney.

Cost: Prenuptial agreements typically cost $1,500 to $5,000 per person depending on complexity. This seems expensive but is cheap compared to losing half a $500,000 inheritance.

Strategy 4: Postnuptial Agreement (If Already Married)

A postnuptial agreement provides similar inheritance protection after marriage. Most states enforce postnups if they meet the same fairness and disclosure requirements as prenups.

Postnups are perfect for protecting inheritance received during marriage. You can execute the agreement shortly after receiving the inheritance to lock in its separate status.

Postnup advantages:

- Can be created any time during marriage

- Protects recently received inheritance

- Updates outdated prenup terms

- Reflects current financial situation

- Resolves inheritance disputes before divorce

Postnup requirements:

- Written and signed by both spouses

- Full financial disclosure

- Independent legal counsel for each spouse

- Consideration (something of value exchanged)

- Fair and reasonable terms

- No coercion

When to consider a postnup:

- Received large inheritance during marriage

- Spouse pressuring you to commingle inheritance

- Marriage having difficulties

- Updating old prenup

- Received unexpected inheritance

Consideration requirement: Some states require “consideration” for postnups to be valid. You must give your spouse something in exchange for signing. This could be release of other claims, promise to update your estate plan in their favor, or payment of money.

Postnups are less common than prenups but equally enforceable in most jurisdictions. If you missed getting a prenup, a postnup is your second chance to protect inheritance.

Strategy 5: Use Trusts for Advanced Protection

Trusts provide the strongest inheritance protection because the property never becomes yours individually. When a trust owns the inheritance, it’s not part of your marital estate. Your spouse cannot claim trust assets in divorce.

Three types of trusts offer the best divorce protection: discretionary trusts, spendthrift trusts, and dynasty trusts.

Discretionary trust:

- Trustee has full control over distributions

- You cannot demand distributions

- Not your property for divorce purposes

- Creditor protection included

- Can be set up before or during marriage

Spendthrift trust:

- Prevents creditors from reaching trust assets

- Includes divorcing spouse as creditor

- “Spendthrift clause” prohibits assignment

- Cannot be divided in divorce

- Must be irrevocable to work

Dynasty trust:

- Protects wealth for multiple generations

- Your children’s inheritances protected from their divorces

- Can last 100+ years in some states

- Estate tax benefits

- Creditor protection for all beneficiaries

Trust considerations:

- Cost: $3,000 to $15,000 to establish

- Ongoing trustee fees: 0.5% to 1.5% of assets annually

- Loss of direct control over assets

- Tax reporting requirements

- Cannot use trust assets for personal benefit without triggering inclusion

If your parent or family member is creating an estate plan, ask them to leave your inheritance in trust rather than outright. A properly drafted trust can protect assets from your divorce, creditors, and poor financial decisions.

Strategy 6: Never Commingle—Even Accidentally

The most common inheritance protection failure is accidental commingling. People don’t intend to mix their inheritance with marital funds. They make innocent mistakes that have expensive consequences.

Once commingling occurs, the burden is on you to trace every dollar back to the original inheritance. If you cannot trace the funds with bank statements and clear documentation, courts will treat everything as marital property.

Commingling mistakes to avoid:

Never do this:

- Deposit inheritance check in joint account (even temporarily)

- Transfer money from inheritance account to joint account

- Pay marital bills from inheritance account

- Use joint account to pay expenses for inherited property

- Mix inheritance with salary in same account

- Use inheritance for joint purchases

- Add inheritance to joint investment account

If accidental commingling happens:

- Stop immediately

- Document what happened in writing

- Separate the funds as soon as possible

- Consult family law attorney

- Get forensic accountant if necessary

- Never admit it was intentional

Real-world example: Mark inherited $75,000 from his uncle. He deposited it in his personal savings account (good start). Three months later, his transmission failed. He transferred $3,500 from his inheritance account to his joint checking account to pay the mechanic (big mistake). Later, he “paid himself back” by transferring $3,500 from the joint account to his inheritance account. During divorce, his wife’s attorney argued the entire inheritance account was now commingled because it received marital funds. Mark had to hire a forensic accountant for $8,000 to trace the circular transfers and prove segregation.

Protection tip: If you need to use inheritance for an expense, withdraw cash or write a check directly from the inheritance account. Never transfer money between accounts back and forth. Each transfer creates tracing issues.

Strategy 7: Avoid Titling Property in Both Names

Adding your spouse’s name to inherited property almost always converts it to marital property. Courts presume you intended to make a gift when you voluntarily put your spouse on the title or deed.

This mistake happens frequently with real estate. You inherit your parents’ house and think, “I should add my wife to the deed for estate planning purposes.” That decision probably just cost you half the house in divorce.

Titling mistakes:

- Adding spouse to inherited house deed

- Buying new car with inheritance titled jointly

- Opening joint bank account for inherited money

- Making spouse co-owner of inherited business

- Adding spouse as joint tenant on investment accounts

Estate planning alternatives:

- Transfer on death (TOD) deed: gives property to spouse only after your death

- Beneficiary designation: names spouse as account beneficiary

- Your will or trust: leaves property to spouse at death

- Life estate: you keep ownership during life, spouse gets it after

Refinancing risks: If you refinance a mortgage on inherited property, the lender might require your spouse to be on the new loan. This doesn’t automatically make the property marital, but it creates complications. Consult an attorney before refinancing any inherited real estate.

Quitclaim deed dangers: Never sign a quitclaim deed giving your spouse any interest in inherited property. Even if they promise it’s “just for the bank” or “estate planning,” you just made a gift.

Strategy 8: Professional Guidance from Attorney and Financial Planner

Large inheritances require professional guidance from both a family law attorney and a financial planner. The cost of consultation is tiny compared to the risk of losing hundreds of thousands of dollars through avoidable mistakes.

Consult professionals before you receive the inheritance if possible. They can guide you on setting up accounts, creating trusts, and documenting everything correctly from day one.

When to hire a family law attorney:

- Inheritance over $100,000

- Marriage already has problems

- Considering divorce in near future

- Received inheritance during marriage

- Spouse demanding access to inheritance

- Already made commingling mistakes

- Need prenup or postnup

When to hire estate planning attorney:

- Setting up inheritance trust

- Parent planning estate and you want protection

- Creating dynasty trust for children

- Received trust distributions

- Complex family business inheritance

When to hire forensic accountant:

- Need to trace commingled funds

- Cannot locate all bank statements

- Multiple transfers between accounts

- Business appreciation issues

- Spouse claims contribution to appreciation

Typical costs:

- Family law consultation: $250 to $500

- Estate planning attorney: $300 to $600 per hour

- Forensic accountant: $5,000 to $25,000 for tracing

- Financial planner: $200 to $400 per hour

For high-net-worth divorces involving significant inheritances, these professional fees are worth the investment. They can save you from mistakes that cost 10 to 100 times more than the consultation fees.

What Happens to Inheritance in Different Divorce Scenarios

The timing of when you received an inheritance affects how courts handle it in divorce. Inheritance before marriage gets different treatment than inheritance during marriage or after separation. Understanding these scenarios helps you plan protection strategies.

Each scenario has unique risks and documentation requirements. What matters most is whether you kept the inheritance completely separate from marital property regardless of timing.

Inheritance Received Before Marriage

Property you inherited before marriage is separate in all 50 states. This is the easiest inheritance to protect because it predates the marriage entirely. However, you can still lose protection through commingling during the marriage.

The biggest risk with premarital inheritance is the length of time you’ve been married. The longer the marriage, the more opportunities to accidentally mix the inheritance with marital property.

Example: You inherited $200,000 from your grandmother in 2015. You married in 2020. During your six-year marriage, you kept the inheritance in a separate account and never commingled it. In 2026, you file for divorce. The inheritance plus all appreciation is your separate property as long as you can document it.

Long marriage risks: Courts may scrutinize premarital inheritance more closely in marriages over 15 to 20 years. In some equitable distribution states, judges have discretion to divide any property if failing to do so would cause significant hardship. This is rare but possible.

Protection steps for premarital inheritance:

- Maintain separate account from before marriage

- Never mix with marital funds during marriage

- Keep original inheritance documentation

- Get prenup acknowledging premarital separate property

- Update documentation quarterly

Inheritance Received During Marriage

Inheritance received during marriage is still separate property, but it faces higher scrutiny in divorce. Courts presume property acquired during marriage is marital, so you must overcome that presumption with clear evidence.

The key is taking immediate action when you receive the inheritance. Open a separate account that same day. Deposit the inheritance check directly. Never let it touch a joint account even for one day.

Higher risk factors:

- Stronger marital property presumption

- More opportunities for commingling

- Spouse may claim contribution to appreciation

- May be used for marital purposes

- Burden of proof is on you

Example: Your father passes away in 2024, leaving you $300,000. You’re already married with two children. You immediately open a separate bank account, deposit the inheritance, and never commingle it. You keep detailed statements. In 2026 when you divorce, the inheritance is separate property because you protected it properly.

Spouse claims: Your spouse might argue they contributed to the inheritance’s appreciation even if the principal is separate. If you inherited a rental property and your spouse managed it, they might claim a share of appreciation. Property division rules vary by state on this issue.

Inheritance Received After Separation (But Before Divorce Finalized)

Inheritance received after separation but before the final divorce decree might be separate property depending on state law. The critical date is your state’s “cutoff date” for determining what counts as marital property.

Some states use the separation date as the cutoff. Property acquired after separation is separate. Other states use the date of filing for divorce. A few states use the date of the final divorce decree.

State cutoff dates:

- Separation date states: Property after separation is separate

- Filing date states: Property after filing is separate

- Decree date states: Property until final decree is marital

- Varies by state: Check your state’s specific rule

Example: You separate from your spouse in January 2025. You file for divorce in June 2025. Your mother passes away in August 2025, leaving you $500,000. Your divorce finalizes in March 2026. Whether this inheritance is marital property depends on your state’s cutoff date.

Protection strategies:

- Research your state’s cutoff date

- File for divorce quickly if expecting inheritance

- Keep inheritance separate regardless

- Document separation date clearly

- Disclose inheritance to court if required

Disclosure issues: Even if inheritance after separation is separate property, you might still need to disclose it in your financial affidavits. Hiding assets can result in sanctions or penalties. Consult an attorney about disclosure requirements versus divisibility.

Inheritance From One Spouse’s Parents to Both Spouses

When a parent leaves inheritance to both spouses jointly, it becomes marital property. The testator’s intent matters. If the will or trust explicitly gives property to “John and Mary Smith together,” courts will treat it as a marital asset.

This happens when parents want to benefit the married couple, not just their child. The inheritance is a gift to the marriage, not to the individual child.

Will language matters:

Separate property: “I leave $100,000 to my daughter, Sarah Martinez” Marital property: “I leave $100,000 to my daughter Sarah Martinez and her husband Robert Martinez”

Marital property: “I leave my house to Sarah and Robert Martinez jointly as tenants in common”

If you expect to receive an inheritance, talk to your parents about their estate planning. Ask them to leave property to you individually, not to you and your spouse jointly. Explain that this protects family assets and gives you more flexibility.

Inherited IRAs and retirement accounts: When one spouse inherits a retirement account and rolls it into their own IRA, that becomes their separate property. But the income and growth might be marital in some states. Consult a financial advisor about inherited retirement accounts.

Common Inheritance Mistakes in Divorce (And How to Fix Them)

Most inheritance protection failures come from five common mistakes. The good news is you can fix some of these mistakes if you act quickly. The bad news is waiting too long makes correction impossible.

If you’ve already made one of these mistakes, don’t panic. Consult a family law attorney immediately. The sooner you act, the better chance you have of salvaging inheritance protection.

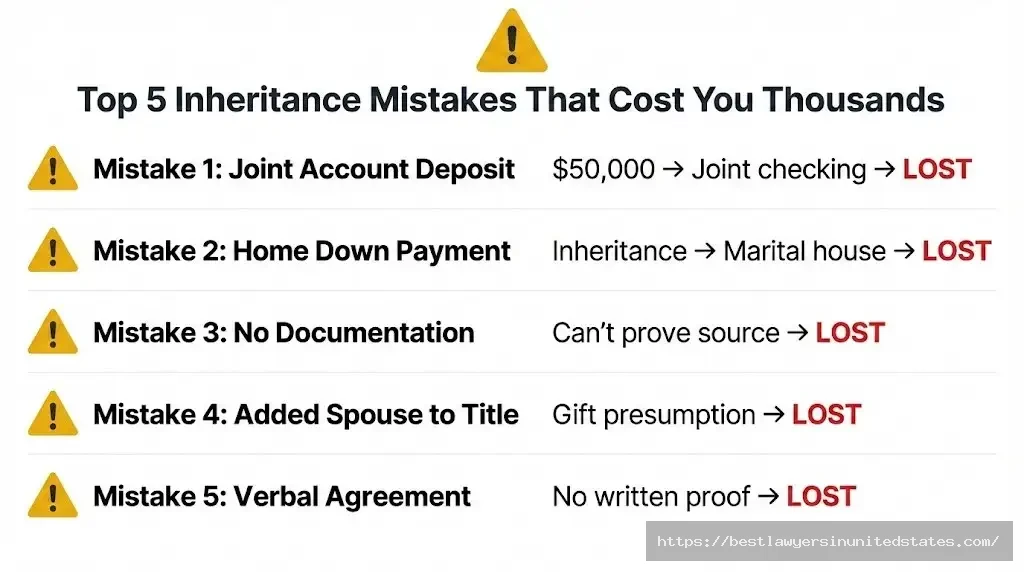

Mistake 1: “It’s Just Easier to Use Our Joint Account”

Depositing inheritance in a joint checking or savings account is the number one protection killer. This seems convenient at the time but creates a nearly impossible tracing problem later.

Courts call this “hopeless commingling” when the mixing is so complete that you cannot distinguish inheritance from marital funds. Once the account has hundreds of transactions over months or years, tracing becomes practically impossible.

Why this fails:

- Joint account has deposits from both spouses’ paychecks

- Bills paid from account mix inheritance with marital income

- Withdrawals use both marital and inheritance funds

- After 6+ months, you cannot trace which dollars are which

- Burden is on you to prove separation (you’ll lose)

How to fix:

- Transfer remaining balance to separate account immediately

- Calculate how much inheritance remains (estimate if needed)

- Document the transfer with written memo

- Close the joint account if possible

- Hire forensic accountant if tracing needed

- Never make this mistake again

Real-world damage: Courts have found six-figure inheritances became entirely marital property after sitting in joint accounts for 12 to 24 months. One case involved a $400,000 inheritance that was commingled with salary deposits and bill payments. After three years, the court ruled the entire account was marital property. The spouse lost $200,000 of inheritance that should have been protected.

Mistake 2: Using Inheritance for Down Payment on Marital Home

Using inherited money for a down payment on a house titled in both names converts that money to marital property. Even if you keep detailed records, you probably just made a gift to the marriage.

This is the second most common mistake after joint account deposits. People inherit money and think, “We need a bigger house for the kids.” They use the inheritance for a down payment and put both names on the deed.

Why this fails:

- House is titled jointly (presumption of gift)

- Inheritance money cannot be separated from the house

- You used separate property to benefit the marriage

- Courts will not “reimburse” you for the down payment in most states

State variations:

- California: Might get reimbursement under Section 2640

- Texas: Inception of title might protect some equity

- Most states: Down payment becomes gift to marriage

Better approach:

- Buy house in your name only with inheritance

- Use marital funds for down payment, keep inheritance separate

- Put inheritance in trust and rent a house

- Keep inheritance liquid and rent

Can you fix this? Maybe, but it’s hard. California and a few other states give reimbursement rights for separate property contributions. You might get the down payment amount back but not appreciation. Most states provide no remedy once you’ve made this mistake.

If you’re considering using inheritance for a home down payment, consult a family law attorney first. There are ways to structure the purchase to protect some inheritance rights, but they must be done before buying.

Mistake 3: Not Documenting the Source

Failing to keep inheritance documentation is like giving away your proof of separate property. Years from now when you divorce, you need to show where the money came from and that you kept it separate.

Without documentation, your spouse’s attorney will argue the money in your “separate” account actually came from marital earnings, bonuses, or gifts from your spouse’s family. You’ll have no way to prove otherwise.

Required documents many people forget:

- Will or trust showing you as beneficiary

- Death certificate

- Estate distribution letter

- Form 1099 from estate

- Initial deposit receipt

- First bank statement showing inheritance deposit

Common documentation gaps:

- Lost the will or trust document

- Never got copy of death certificate

- Threw away old bank statements

- No record of initial deposit amount

- Commingled before documenting

How to fix:

- Contact estate attorney or executor for copies

- Get death certificate from county records

- Request old bank statements from bank (may charge fees)

- Create sworn affidavit describing inheritance

- Get testimony from family members who know about inheritance

- Hire forensic accountant to recreate paper trail

Prevention: Create an inheritance documentation binder today. Put every document related to the inheritance in it. Scan everything to cloud storage. Update the binder every time you receive a bank statement or make a transaction. Store it in a fireproof safe.

Mistake 4: Adding Spouse’s Name “For Estate Planning Purposes”

Adding your spouse to an inherited asset “just for estate planning” creates a gift presumption you may never overcome. This well-intentioned mistake costs people millions of dollars in divorce.

The reasoning seems sound: “If I die, I want my spouse to get the house without probate.” The solution seems simple: “I’ll just add their name to the deed.” But you just converted your separate inheritance into marital property.

Why this fails:

- Voluntary transfer to spouse presumed to be gift

- Difficult to prove you didn’t intend gift

- Courts will not believe “it was just for convenience”

- Spouse now has ownership interest

Better estate planning tools:

- Transfer on death (TOD) deed

- Beneficiary designation

- Your will or trust

- Life estate deed

- Joint tenancy with right of survivorship (only after death)

All of these accomplish the same goal (spouse gets property when you die) without making a gift now.

Can you fix this? Sometimes. Your spouse can sign a quitclaim deed removing themselves from the title. But they have to agree. Once your spouse is on title, they have ownership rights. If divorce is imminent, they’ll never sign a quitclaim deed.

Prevention: Never add your spouse to any inherited asset. Use estate planning tools instead. If you’ve already added them, consult an attorney about getting a postnuptial agreement or quitclaim deed while the marriage is still good.

Mistake 5: Assuming Verbal Agreements Protect Inheritance

Your spouse saying “that’s your money, I won’t claim it” has zero legal value in divorce. Verbal agreements about property division are not enforceable in any state.

People have false security from these conversations. Their spouse acts understanding when they receive the inheritance. They verbally agree it’s separate property. Years later during divorce settlement negotiations, the spouse claims half of it.

Why verbal agreements fail:

- Not enforceable in court

- No written evidence of agreement

- Spouse can change their mind

- Attorneys will advise spouse to claim inheritance

- You have no proof agreement existed

What you need instead:

- Written postnuptial agreement

- Signed by both parties

- Independent attorneys for both

- Notarized if possible

- Full disclosure of inheritance amount

Real example: Husband inherits $250,000. Wife says, “That’s your family money, I would never ask for it.” Husband keeps it separate but doesn’t get written agreement. Five years later, they divorce. Wife’s attorney demands half the inheritance ($125,000). Husband says, “But you promised!” Wife says, “I don’t remember that conversation.” Court rules inheritance is separate property (husband documented it well), but the point is wife tried to claim it despite verbal promise.

Can you fix this? Yes. Get a postnuptial agreement now while your marriage is stable. Document your verbal understanding in writing. Have it reviewed by attorneys. Sign and notarize it. This protects both parties and prevents future disputes.

Emergency Steps If You’ve Already Made These Mistakes

Discovering you made inheritance protection mistakes requires immediate action. The longer you wait, the harder fixing becomes. Some mistakes cannot be fixed at all if too much time has passed.

Immediate actions (within 7 days):

- Stop making the mistake now

- Separate any commingled funds immediately

- Document everything that happened

- Calculate approximate inheritance remaining

- Consult family law attorney

- Do not tell spouse you’re consulting attorney

Short-term actions (within 30 days):

- Gather all documentation you have

- Request missing documents from estate, banks

- Meet with attorney about damage control

- Consider postnuptial agreement if marriage stable

- Hire forensic accountant if needed for tracing

- Create going-forward separation plan

Forensic accounting option: If you commingled funds but kept records, a forensic accountant might be able to trace the inheritance through bank statements. They use sophisticated methods to track deposits and withdrawals. This costs $5,000 to $25,000 but can save a six-figure inheritance.

When to give up: Some mistakes cannot be fixed. If you deposited inheritance in a joint account five years ago and spent most of it on marital expenses with no clear records, you probably lost it. Consult an attorney, but be realistic about recovery chances.

Prevention going forward: Even if you lost one inheritance to mistakes, don’t repeat them. If you receive another inheritance or expect one in the future, implement proper protection from day one.

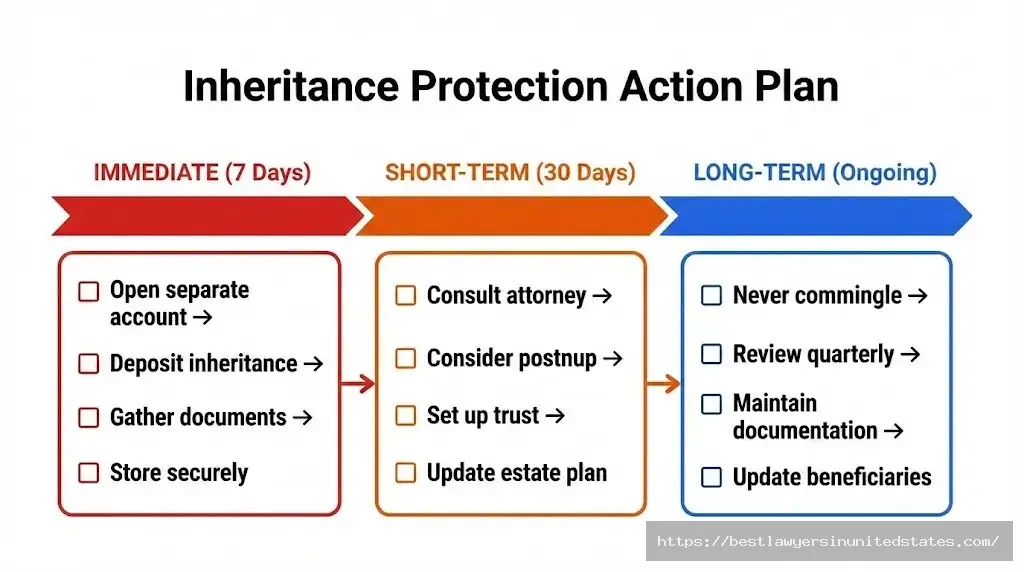

Protecting Your Inheritance: Action Plan and Next Steps

Inheritance protection requires proactive planning, careful documentation, and strict separation from marital property. The rules are clear across all 50 states: inheritance is separate property, but you can lose protection through commingling and other mistakes.

Taking action today protects your family’s legacy. Whether you’ve already received an inheritance or expect one in the future, these steps will help you maintain separate property status.

Immediate Actions (Within 7 Days)

If you recently received an inheritance or have one in a separate account, take these steps this week:

Critical first steps:

- Open new bank account in your name only (if you haven’t already)

- Deposit inheritance or transfer it from joint account immediately

- Request no spousal access or authorization on account

- Set up separate online banking credentials

- Store login information privately

- Make two copies of all inheritance documentation

Do not wait. Every day inheritance sits in a joint account increases commingling risk. Every transaction in a mixed account makes tracing harder. Act now while the paper trail is clear.

Short-Term Actions (Within 30 Days)

After securing the inheritance in a separate account, focus on documentation and legal protection:

Month one priorities:

- Consult family law attorney about your situation

- Discuss postnuptial agreement if you’re married

- Meet with estate planning attorney about trust options

- Gather all inheritance documents in one folder

- Scan everything to secure cloud storage

- Review beneficiary designations on all accounts

- Set up separate investment account if needed (in your name only)

Professional guidance: For inheritances over $100,000, attorney fees of $500 to $2,000 are worth the protection they provide. An attorney can spot issues you might miss and create protection strategies specific to your state.

Long-Term Ongoing Actions

Inheritance protection is not a one-time event. You must maintain separation and documentation throughout your marriage:

Quarterly:

- Review bank statements for any errors

- Update your documentation folder

- Verify no marital deposits in inheritance account

- Check that account access hasn’t changed

Annually:

- Meet with attorney if marriage experiencing problems

- Review estate plan to protect children’s inheritances

- Consider dynasty trust for multi-generational protection

- Update financial records and documentation

Never:

- Add spouse as joint owner to inheritance accounts

- Use inheritance for marital expenses

- Transfer money between inheritance and joint accounts

- Commingle inheritance with marital funds

- Title inherited property in both names

When to Consult an Attorney

Certain situations require immediate legal consultation. Don’t wait until divorce is filed. By then, damage control is much harder.

Seek attorney help if:

- Divorce appears imminent and you have inheritance

- You already commingled inheritance with marital funds

- Spouse is demanding share of your inheritance

- You used inheritance for marital home down payment

- Inheritance is in business or LLC formed during marriage

- Large inheritance ($100,000+) received during marriage

- Spouse contests your separate property claim

- You need complex tracing or forensic accounting

- Considering prenup or postnup

What to bring to attorney meeting:

- All inheritance documentation

- Bank statements for inheritance accounts

- Any commingling documentation

- Marriage date and length

- State of residence

- Approximate inheritance value

- List of how funds have been used

- Any existing prenup or postnup

Most family law attorneys offer free consultations or charge $250 to $500 for initial meetings. This consultation can prevent mistakes that cost hundreds of thousands of dollars.

Protecting Future Generations

Your inheritance protection strategy should extend to your children and grandchildren. Estate planning tools can protect family wealth from their future divorces too.

Generational protection strategies:

- Leave inheritances to children in trust (not outright)

- Use dynasty trusts lasting 100+ years

- Include spendthrift provisions

- Appoint independent trustee

- Encourage children to get prenups before marriage

- Educate children about inheritance protection

Dynasty trust benefits:

- Protects assets from children’s divorces

- Protects grandchildren from their divorces

- Creditor protection for all generations

- Estate tax benefits

- Professional management

- Preserves family wealth for 100+ years

If you’re creating an estate plan or updating your will, consult an estate planning attorney about inheritance protection trusts for your children. The relatively small additional cost provides enormous protection.

Frequently Asked Questions About Inheritance and Divorce

Is my spouse entitled to my inheritance when we get divorced?

Quick Answer: No, your spouse is not entitled to your inheritance in most cases. Inheritance is separate property in all 50 states and not subject to division in divorce.

However, you can lose this protection if you commingle the inheritance with marital property, add your spouse’s name to inherited assets, or use marital funds to improve inherited property. The key is keeping inheritance completely separate from marital assets.

Does my spouse automatically get half of my inheritance?

Quick Answer: No, your spouse does not automatically get half of your inheritance. Inherited property belongs exclusively to the spouse who received it.

The only way your spouse can claim half is if you converted the inheritance to marital property through commingling, transmutation, or joint titling. Keep inheritance in your name only and never mix it with marital funds.

When does an inheritance become marital property?

Quick Answer: Inheritance becomes marital property when you commingle it with marital funds, add your spouse’s name to the asset, or use it for marital purposes like buying a jointly-titled house.

The three main conversion events are: depositing inheritance in a joint bank account, titling inherited property in both spouses’ names, and using marital effort or funds to improve inherited assets. All of these can transform separate inheritance into divisible marital property.

How can I protect my inheritance from my spouse?

Quick Answer: Protect inheritance by keeping it in a separate account in your name only, never commingling it with marital funds, maintaining detailed documentation, and considering a prenup or postnup.

The most important step is opening a bank account with only your name on it and using that account exclusively for inherited funds. Never add your spouse as co-owner and never use the account for marital expenses.

What if I already put my inheritance in a joint account?

Quick Answer: Transfer the inheritance to a separate account in your name only immediately. The longer it stays in a joint account, the harder tracing becomes.

Hire a forensic accountant if you need to trace commingled funds. They can sometimes separate inheritance from marital funds using bank records. This costs $5,000 to $25,000 but can save a six-figure inheritance.

Can a prenup protect my future inheritance?

Quick Answer: Yes, a prenuptial agreement can protect both current and future inheritance if it includes explicit language waiving claims to inherited property.

The prenup must be properly executed with full disclosure, independent attorneys, and no coercion. It should specifically state that “all property received by either party by gift, bequest, devise, or descent shall remain separate property.”

Do I have to tell my spouse about my inheritance?

Quick Answer: You may have disclosure requirements depending on your state, but inheritance itself is separate property. Consult an attorney about disclosure obligations.

During divorce, you must disclose inheritance on financial affidavits even if it’s separate property. Hiding assets can result in sanctions. However, you don’t need your spouse’s permission to keep inheritance separate during marriage.

What happens if I used my inheritance to buy our house?

Quick Answer: Using inheritance for a down payment on a jointly-titled house typically converts that money to marital property. You probably made a gift to the marriage.

Some states like California give reimbursement rights under Family Code Section 2640. Most states provide no remedy. If you’re considering this, consult a family law attorney first about protective strategies.

Can my ex-spouse claim my inheritance after we’re divorced?

Quick Answer: Generally no, but if you receive inheritance after separation and before the final decree, it depends on your state’s cutoff date for marital property.

Some states use separation date, others use filing date, and a few use final decree date. Post-divorce inheritance is always separate. However, inheritance could affect alimony modification requests.

Is inheritance considered income for child support or alimony?

Quick Answer: Inheritance principal is not income, but courts may consider post-divorce inheritance when modifying spousal support. Rules vary by state.

If you receive a large inheritance after divorce, your ex-spouse might petition to increase child support or modify alimony based on changed circumstances. The inheritance itself doesn’t count as income, but investment returns from it might.

What’s the difference between commingling and transmutation?

Quick Answer: Commingling is mixing separate property with marital property until they cannot be traced. Transmutation is intentionally converting separate property to marital property through actions or documents.

Commingling usually happens accidentally when you deposit inheritance in a joint account. Transmutation happens when you add your spouse’s name to inherited property or use inheritance to buy jointly-titled assets.

How do I prove my inheritance is separate property?

Quick Answer: Prove inheritance is separate by showing the will or trust, death certificate, estate distribution documents, initial deposit records, and complete bank statements with no commingling.

You must trace an unbroken chain from the inheritance source to the current asset. Missing bank statements or unclear transfers can break the chain and cost you the inheritance.

Can I give my inheritance to my children to protect it?

Quick Answer: No, transferring assets to children to hide them from divorce is fraudulent conveyance and can result in sanctions or criminal charges.

Courts can “claw back” fraudulently transferred assets and penalize you severely. The proper way to protect children’s future inheritances is through trusts established in your estate plan, not transfers made to avoid divorce claims.

What if my inheritance is in a trust—is it still protected?

Quick Answer: Yes, inheritance received through a properly structured discretionary or spendthrift trust is protected from divorce claims. The trust owns the assets, not you individually.

However, if you withdraw funds from the trust and commingle them with marital property, you lose protection. Keep trust distributions in separate accounts and never mix them with marital funds.

Do inheritance laws differ by state?

Quick Answer: Yes, state inheritance divorce laws vary significantly. The biggest difference is between community property states (9 states) and equitable distribution states (all others).

Community property states have stricter separate property definitions and higher burdens of proof. Equitable distribution states give judges more discretion. Some states have easier tracing requirements than others. Research your specific state’s laws or consult a family law attorney.

Questions about protecting your inheritance or need legal help?

Find experienced family law attorneys who handle high-asset divorces and inheritance protection cases.

Email: [email protected]

Last updated: January 2026. This article provides general information only and does not constitute legal advice. Inheritance and divorce laws vary by state. Consult a licensed family law attorney in your jurisdiction for advice specific to your situation.