Dividing property during divorce ranks among the most complex and contentious issues couples face. Courts split marital assets and debts based on state law, which follows either community property or equitable distribution rules. This guide explains how property division works, what assets can be split, and how to protect your financial interests during divorce.

Whether you’re just considering divorce or already in the process, understanding property division helps you make informed decisions. You’ll learn the difference between marital and separate property, how courts value assets, and what to expect in your state. We also cover special situations like business ownership, retirement accounts, and hidden assets.

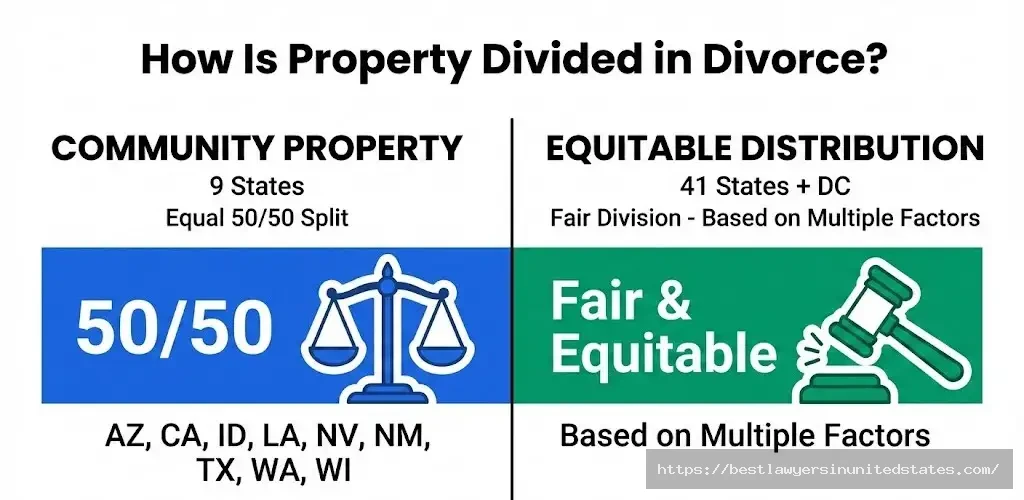

Understanding Property Division Systems in Divorce

Two main systems govern how courts divide property during divorce. Your state follows either community property or equitable distribution rules. The system your state uses determines how courts split assets and debts between spouses.

Community Property States

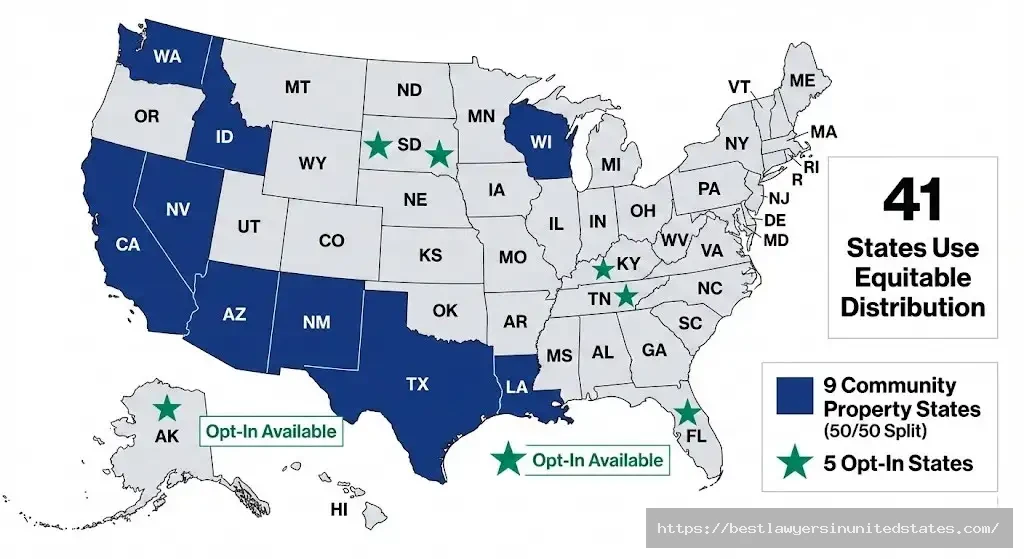

Nine states follow community property rules: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. These states treat most property acquired during marriage as belonging equally to both spouses.

Courts typically split community property 50/50 in these states. Each spouse gets half of everything earned or purchased during the marriage. The law views marriage as an equal partnership where both spouses contribute equally, regardless of who earned more income.

Community property includes:

- Wages and salaries earned during marriage

- Property purchased with marital income

- Business income from marital efforts

- Retirement benefits earned during marriage

- Debts incurred during marriage

Five additional states allow couples to opt into community property rules: Alaska, South Dakota, Tennessee, Kentucky, and Florida. Couples must sign a written agreement to choose community property treatment.

Equitable Distribution States

The remaining 41 states and Washington D.C. use equitable distribution. Courts divide marital property fairly, but not necessarily equally. Judges consider multiple factors to determine what’s fair for each couple.

Equitable means fair, not equal. One spouse might receive 60% while the other gets 40%. Courts look at each spouse’s financial situation, contributions to the marriage, and future earning potential.

Common equitable distribution factors:

- Length of the marriage

- Each spouse’s income and earning capacity

- Age and health of each spouse

- Contributions as homemaker or breadwinner

- Standard of living during marriage

- Child custody arrangements

- Tax consequences of property division

- Economic misconduct or waste of assets

Key Differences: Community Property vs Equitable Distribution

| Feature | Community Property | Equitable Distribution |

|---|---|---|

| Division Method | Equal 50/50 split | Fair, not necessarily equal |

| Typical Split | 50/50 presumed | 40/60 to 60/40 common |

| Judge Discretion | Limited (strict rules) | Broad (many factors) |

| Property Scope | Community vs separate | Marital vs non-marital |

| States Using | 9 states | 41 states + DC |

| Fault Consideration | Generally no | Some states yes |

The division system affects your financial outcome significantly. California divorce costs and Texas divorce costs differ partly due to property division complexity. Understanding your state’s approach helps you prepare for settlement negotiations.

Marital Property vs Separate Property: What Can Be Divided?

Courts only divide marital property during divorce. Separate property belongs to one spouse exclusively and stays with that person. Knowing the difference protects your assets and sets realistic expectations.

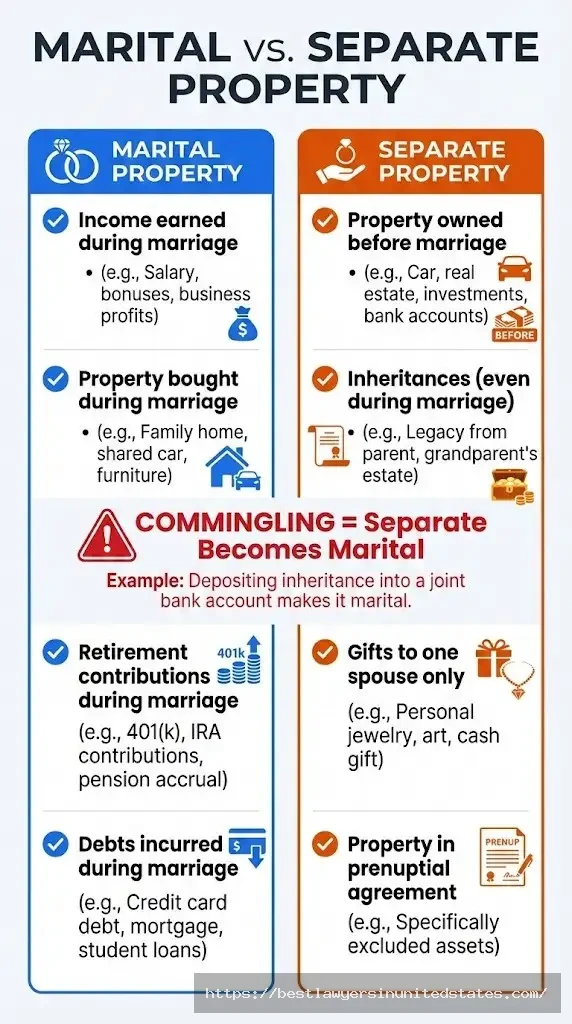

What Is Marital Property?

Marital property includes nearly everything acquired during marriage, regardless of whose name appears on the title. The date you married through your separation date determines what counts as marital property.

Marital property typically includes:

- Income earned by either spouse during marriage

- Houses, cars, and furniture purchased during marriage

- Bank accounts and investments opened during marriage

- Retirement contributions made during marriage

- Business interests acquired or grown during marriage

- Stock options earned during marriage (even if not vested)

- Debts incurred during marriage

A common misconception is that property in one person’s name stays theirs. Wrong. If you bought a car during marriage using your salary, it’s marital property even if only your name is on the title. The same applies to bank accounts, investments, and most other assets.

What Is Separate Property?

Separate property belongs exclusively to one spouse. Courts cannot divide it during divorce. This property stays with the original owner regardless of the divorce outcome.

Separate property includes:

- Property owned before marriage

- Gifts received by one spouse (from anyone except the other spouse)

- Inheritances received by one spouse

- Property designated as separate in a prenuptial agreement

- Personal injury settlements (in most states)

- Property acquired after the date of separation

Keep separate property separate to maintain its protected status. Mixing separate property with marital property can change its classification.

When Separate Property Becomes Marital

Separate property loses its protected status through commingling or transmutation. These processes convert separate property into marital property, making it subject to division.

Commingling happens when you mix separate and marital property together. Depositing a $50,000 inheritance into a joint checking account used for household expenses comingles those funds. After years of deposits and withdrawals, you cannot trace which money came from the inheritance. The account becomes marital property.

Transmutation occurs when you intentionally change separate property to marital. Adding your spouse’s name to your separately-owned house deed transmutes it into marital property. Both spouses now have ownership rights.

| Scenario | Property Type | Reason |

|---|---|---|

| House owned before marriage | Separate | Premarital asset |

| Same house, spouse added to deed | Marital | Transmutation |

| Inheritance deposited in joint account | Marital | Commingling |

| Inheritance kept in separate account | Separate | Maintained separation |

| Retirement earned during marriage | Marital | Earned while married |

| Retirement earned before marriage | Part separate/part marital | Portion formula applies |

Understanding these distinctions helps you avoid accidentally converting separate property. Keep inheritance and gifts in separate accounts. Avoid adding your spouse to titles of premarital property unless you intend to share ownership.

How Are Assets Valued and Divided?

Courts must determine the value of each asset before dividing property. Professional appraisers and financial experts provide valuations for complex assets. The valuation date and method used can significantly affect your settlement.

Asset Valuation Methods

Different assets require different valuation approaches. Real estate needs professional appraisals while bank accounts show clear statement balances. Accurate valuations ensure fair property division.

Real estate requires a professional appraiser to determine fair market value. Appraisers consider recent comparable sales, property condition, and market trends. Home values fluctuate, so timing matters. Some couples agree to sell and split proceeds, avoiding valuation disputes.

Vehicles can be valued using Kelley Blue Book, NADA Guides, or similar resources. These tools factor in make, model, year, mileage, and condition. Car valuations are straightforward compared to other assets.

Bank accounts and investments use account statements from the valuation date. The balance on that specific date becomes the asset’s value. Market fluctuations between valuation and actual division can create issues.

Business interests require forensic accountants or certified business valuation experts. They analyze financial statements, assets, liabilities, customer base, and future earning potential. Business valuations often spark disputes due to different valuation methods producing different results.

| Asset Type | Valuation Method | Who Values It |

|---|---|---|

| Real Estate | Professional appraisal | Licensed appraiser |

| Vehicles | Market value guides | KBB, NADA |

| Bank Accounts | Statement balance | Account statements |

| Retirement Accounts | Account balance | Plan administrator |

| Businesses | Income/asset/market approach | Business valuator |

| Personal Property | Replacement cost | Appraiser (if valuable) |

| Cryptocurrency | Exchange price | Market data |

Valuation Date Issues

The valuation date determines when asset values are measured. States differ on which date to use. Some use the separation date while others use the trial date or divorce filing date.

Markets rise and fall between separation and divorce finalization. A retirement account worth $200,000 at separation might be worth $250,000 at trial. Which value applies? State law decides.

Common valuation dates:

- Date of separation (when spouses started living apart)

- Date of divorce filing

- Date of trial or final hearing

- Date divorce becomes final

Strategic timing can affect outcomes. Selling assets before the valuation date changes what’s available for division. Courts frown on intentional asset manipulation but legitimate transactions happen. Document all major financial decisions during divorce proceedings.

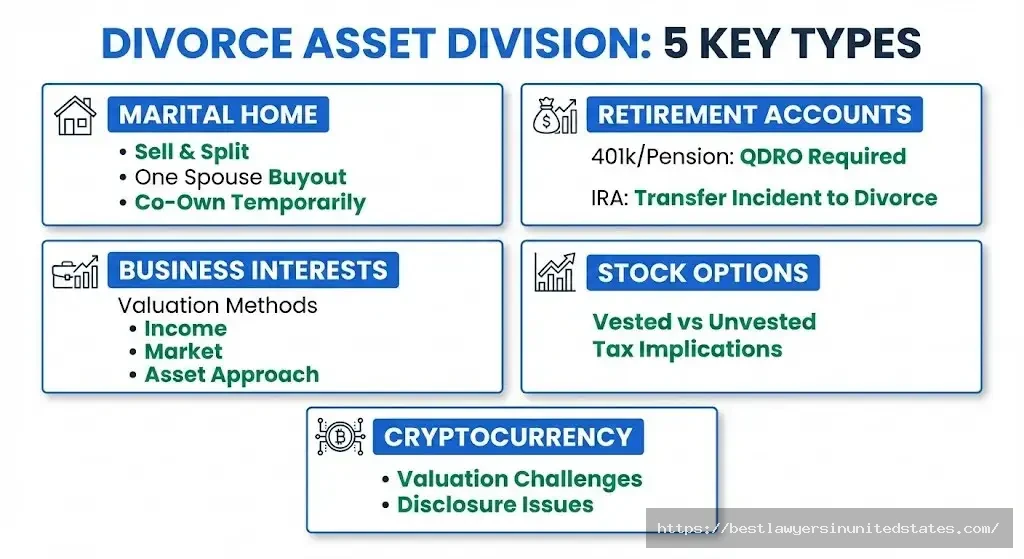

Dividing Complex Assets in Divorce

Some assets require special handling during property division. The marital home, retirement accounts, and business interests present unique challenges. Understanding these complexities helps you negotiate better settlements.

The Marital Home

The house where you lived during marriage often represents your largest asset. Courts offer several options for dividing home equity. Each option carries different financial and tax implications.

Option 1: One spouse keeps the house. The keeping spouse buys out the other’s equity share. This requires refinancing the mortgage to remove the departing spouse from liability. The keeping spouse must qualify for the new loan based on their income alone.

Option 2: Sell the house and split proceeds. Both spouses share proceeds after paying off the mortgage and selling costs. This option works best when neither spouse can afford the house alone or when moving on completely makes sense. Timing the sale affects proceeds based on market conditions.

Option 3: Continue co-owning temporarily. Some couples delay selling until children graduate or market conditions improve. Co-ownership requires clear agreements about mortgage payments, maintenance, and eventual sale terms. This option maintains housing stability but extends financial ties.

Tax considerations matter significantly. Selling the marital home may trigger capital gains taxes. Each spouse can exclude up to $250,000 in gains ($500,000 for couples filing jointly). Timing and ownership duration affect tax liability.

Need to understand who gets the house in divorce? State laws and individual circumstances determine the answer. Neither spouse has automatic rights to the marital home.

Retirement Accounts and Pensions

Retirement accounts earned during marriage constitute marital property subject to division. Courts divide these accounts without triggering taxes or penalties through special procedures.

Qualified Domestic Relations Orders (QDROs) allow tax-free division of 401(k)s and pension plans. The QDRO directs the plan administrator to create a separate account for the non-employee spouse. Without a QDRO, withdrawing funds to pay your spouse triggers taxes and early withdrawal penalties.

The QDRO process takes several steps:

- Determine the marital portion of the account

- Draft the QDRO document (requires specialized attorney)

- Submit to plan administrator for approval

- Court approves the QDRO

- Plan administrator splits the account

IRA division works differently. IRAs split through a simple “transfer incident to divorce” without needing a QDRO. The divorce decree authorizes the transfer. The receiving spouse rolls funds into their own IRA tax-free.

Military pensions follow special federal rules. The “10/10 rule” requires 10 years of marriage overlapping with 10 years of military service for direct payment from the Defense Finance and Accounting Service. Shorter marriages can still divide military pensions, but payment methods differ.

| Account Type | Division Method | Tax Consequences | Timeline |

|---|---|---|---|

| 401(k) | QDRO required | None if done properly | 3-6 months |

| Pension | QDRO required | None if done properly | 3-6 months |

| IRA | Transfer incident to divorce | None | 2-4 weeks |

| Military Pension | Court order + 10/10 rule | None | Varies |

Business Interests

Dividing a business owned by one or both spouses requires careful valuation and creative solutions. Courts determine whether the business is marital property, value it, then decide how to divide it.

Valuation methods for businesses include:

- Income approach: Values future earning potential

- Market approach: Compares to similar business sales

- Asset approach: Values tangible and intangible assets

Business owners sometimes manipulate valuations to minimize what they owe their spouse. Forensic accountants trace income, expenses, and asset transfers. They identify schemes like paying non-existent employees or deferring income.

Division options include:

- Buyout: One spouse buys the other’s interest over time

- Sale: Sell the business and split proceeds

- Co-ownership: Continue running the business together (rare)

- Trade-off: Non-owner spouse gets other assets equal to business value

Most divorcing couples cannot continue co-owning a business. Buyouts or offsetting the business value with other assets work better. The non-owner spouse might receive the house equity while the owner keeps 100% of the business.

Stock Options and Equity Compensation

Stock options and restricted stock units (RSUs) earned during marriage are marital property. Division becomes complicated when options haven’t vested yet or when exercise dates span separation and divorce.

Vested vs unvested options present different challenges. Vested options have value you can exercise immediately. Unvested options require waiting until the vesting date arrives. Courts still divide unvested options using formulas that account for past and future service.

A common formula calculates the marital portion:

- Marital portion = (months married while earning options) ÷ (total months from grant to vest) × total options

Courts also consider tax implications. Exercising options triggers ordinary income tax. The spouse exercising options bears the tax burden, so settlements account for this.

Cryptocurrency and Digital Assets

Cryptocurrency holdings like Bitcoin, Ethereum, and other digital assets are marital property if acquired during marriage. Disclosure and valuation present unique challenges.

Cryptocurrency values fluctuate wildly. A Bitcoin worth $60,000 at separation might be worth $45,000 at trial or $75,000. Courts must decide which date to use for valuation.

Division challenges include:

- Volatility: Prices change dramatically hour to hour

- Hidden wallets: Spouses can hide digital assets in unknown wallets

- International exchanges: Assets held offshore are harder to trace

- Valuation timing: Determining which date’s price applies

Forensic accountants examine blockchain transactions and exchange records to find hidden cryptocurrency. Computer forensics might reveal wallet addresses. Courts can order spouses to transfer cryptocurrency or assign equivalent value in other assets.

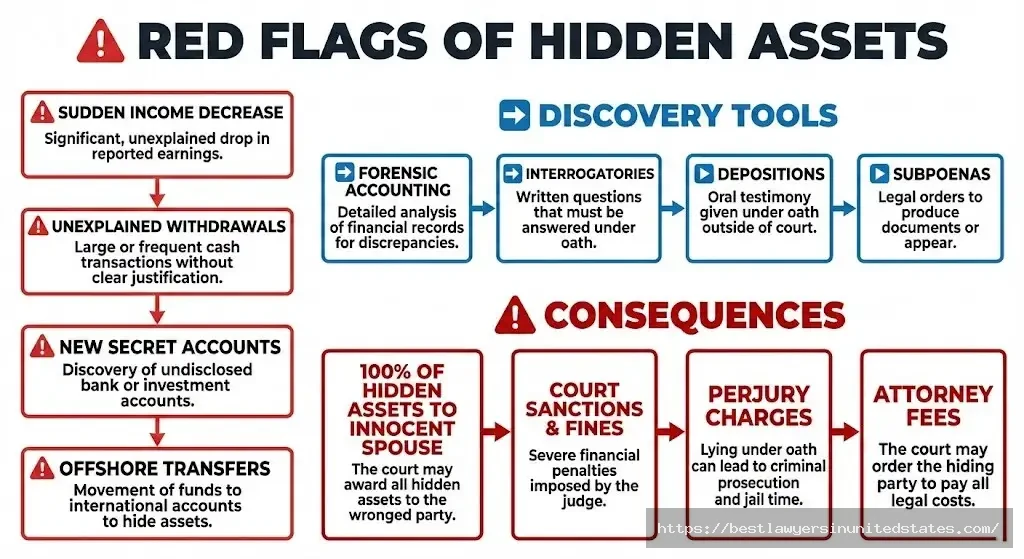

Hidden Assets: Detection and Consequences

Some spouses hide assets to avoid sharing them during divorce. Courts require full financial disclosure from both parties. Hiding assets violates this duty and carries serious penalties.

Common Asset Hiding Tactics

Dishonest spouses use various methods to conceal assets from their partners and the court. Knowing these tactics helps you spot warning signs.

Common hiding strategies:

- Opening accounts at unknown banks or credit unions

- Transferring money to family members or friends for “safekeeping”

- Overpaying taxes to get refunds after divorce

- Delaying bonuses or raises until after divorce finalizes

- Undervaluing business inventory or assets

- Creating fake debts owed to friends or family

- Paying non-existent employees (in family businesses)

- Purchasing expensive items that can be hidden (art, jewelry, collectibles)

- Opening cryptocurrency wallets in untraceable exchanges

- Establishing offshore accounts in tax havens

Red flags that warrant investigation include:

- Sudden income decreases without explanation

- Unexplained account withdrawals

- Mail redirected to new addresses

- New passwords on previously shared accounts

- Defensive behavior about finances

- Reluctance to produce documents

Discovery Process

Legal discovery gives you tools to uncover hidden assets. Both spouses must provide sworn financial disclosures listing all assets and debts. Courts take this duty seriously.

Discovery tools include:

Interrogatories: Written questions your spouse must answer under oath. You can ask about account numbers, asset locations, and transaction details.

Requests for production: Demands for documents like bank statements, tax returns, business records, and account applications. Your spouse must produce these documents or face court sanctions.

Depositions: Oral questioning under oath before a court reporter. Lawyers can follow up on suspicious answers immediately.

Subpoenas: Court orders requiring third parties (banks, employers, accountants) to produce records. These bypass your spouse’s control over information.

Forensic accounting: Certified forensic accountants analyze financial records looking for irregularities. They trace money movement, identify lifestyle inconsistencies, and calculate actual income.

Forensic accountants cost $5,000 to $25,000+ but prove valuable in high-asset cases. They find hidden assets through:

- Analyzing tax returns for unreported income

- Examining credit card statements for unusual purchases

- Reviewing business records for fake expenses

- Tracing bank transfers to unknown accounts

- Comparing lifestyle to reported income

Legal Penalties for Concealing Assets

Courts impose harsh penalties on spouses who hide assets. Judges view asset concealment as fraud on the court and the other spouse. Consequences extend beyond just turning over the hidden assets.

Penalties include:

- Awarding 100% of hidden assets to innocent spouse: The hiding spouse loses their share entirely

- Sanctions and fines: Courts impose monetary penalties payable to the other spouse

- Attorney fee awards: Hiding spouse pays the other spouse’s attorney fees for discovering the concealment

- Perjury charges: Criminal charges for lying under oath about assets

- Reopening settled cases: Discovered assets can reopen finalized divorces

- Contempt of court: Jail time for willfully violating court orders

Beyond legal penalties, hiding assets destroys credibility with the judge. Courts view everything that spouse says with suspicion. This skepticism extends to other divorce issues like child custody and alimony.

Debt Division in Divorce

Courts divide marital debts just like they divide assets. Understanding how debt division works protects you from your spouse’s unpaid bills after divorce.

How Marital Debts Are Divided

Marital debts include any money owed that was incurred during the marriage for marital purposes. Courts allocate these debts between spouses using the same community property or equitable distribution rules that apply to assets.

Common marital debts:

- Mortgage on marital home

- Car loans for vehicles purchased during marriage

- Credit card balances (even if card is in one name)

- Home equity lines of credit

- Personal loans taken during marriage

- Medical bills incurred during marriage

- Tax debt from joint returns

Debt in only one spouse’s name still counts as marital debt if incurred during the marriage. Your spouse’s credit card with only their name becomes your responsibility if charges were for household expenses or marital purposes.

Student loan debt receives special treatment in many states. Loans taken before marriage typically remain that spouse’s separate debt. Loans for education during marriage might be considered marital debt depending on state law and whether marital income paid for living expenses while in school.

Courts consider these factors when dividing debt:

- Which spouse incurred the debt

- Whether the debt benefited the marriage or only one spouse

- Each spouse’s ability to pay

- Income and earning capacity of each spouse

- Who receives the asset tied to the debt (like keeping the car with its loan)

| Debt Type | Usually Divided | Considerations |

|---|---|---|

| Mortgage | Yes (with home) | Who keeps the house |

| Car Loan | With vehicle | Who keeps the car |

| Credit Cards | Yes (if marital spending) | Individual charges may vary |

| Student Loans | Maybe | When incurred matters |

| Business Debt | Usually with business | Who operates business |

| Tax Debt | Typically shared | Joint return liability |

Protecting Yourself from Spouse’s Debt

The divorce decree assigns debts to each spouse, but creditors aren’t bound by court orders. If both names are on a credit card, the credit card company can pursue either spouse regardless of who the court assigned the debt to.

Protection strategies:

Pay off joint debts before divorce finalizes when possible. This eliminates the risk of your ex-spouse defaulting on assigned debts. Use proceeds from selling assets or tap separate funds to clear joint obligations.

Refinance joint obligations into separate accounts. If your spouse keeps the house, they should refinance the mortgage into their name only. This removes your liability and protects your credit if they default.

Close joint accounts immediately upon separation. Prevent your spouse from running up charges you’ll be responsible for. Open individual accounts in your name only.

Monitor your credit reports for years after divorce. Your ex-spouse’s unpaid debts on joint accounts damage your credit score. Early detection lets you address problems quickly.

Include indemnification clauses in settlement agreements. These require your spouse to reimburse you if you have to pay debts assigned to them. While not preventing creditor collection, they give you legal recourse.

Consider bankruptcy if debt overwhelms both spouses. Filing before divorce can discharge marital debts. Timing and coordination matter since bankruptcy affects property division.

Understanding debt division helps you negotiate settlements that protect your financial future. Don’t focus only on assets while ignoring debt allocation.

Property Division by State

State law determines how courts divide property. Understanding your state’s approach helps you plan for divorce and negotiate settlements. This section compares the two main systems and highlights state variations.

Community Property States Breakdown

Nine states follow community property rules with some variations. While all split marital property equally in theory, practical application differs.

Arizona: Strictly divides community property 50/50. Judges have limited discretion to deviate from equal division. Separate property stays separate unless commingled.

California: Divides community property equally but allows flexibility for community debts. Judges can assign debts unequally based on ability to pay. California divorce costs reflect high attorney fees for navigating complex property division.

Idaho: Equal division of community property with few exceptions. Courts rarely deviate from 50/50 splits.

Louisiana: Follows French civil law tradition with equal community property division. Complex rules govern separate property classification.

Nevada: Strictly equal division unless spouses agree otherwise. Nevada makes dividing community property straightforward but inflexible.

New Mexico: Equal division presumed but courts consider waste or destruction of community property. Spouse who dissipated assets may receive less.

Texas: Equal and just division of community property. Courts can divide unequally if equal division would be unjust. Texas divorce costs benefit from straightforward community property rules.

Washington: Divides property “justly and equitably” which doesn’t always mean 50/50. Judges consider fairness factors similar to equitable distribution states.

Wisconsin: Equal presumption for community property division. Deviations require specific findings by the court.

Opt-in states: Alaska, South Dakota, Tennessee, Kentucky, and Florida allow couples to elect community property treatment through agreement.

Equitable Distribution Factors by State

Equitable distribution states consider multiple factors when dividing property. While specific factors vary, common themes emerge across states.

Standard factors most states consider:

Marriage length: Longer marriages typically result in more equal division. Short marriages might favor separate property remaining separate.

Income and earning capacity: Courts consider each spouse’s current income and future earning potential. Higher earners might receive less property.

Age and health: Older spouses or those with health problems may need more assets to support themselves.

Contributions to marriage: Both financial contributions and homemaker services count. Raising children and supporting a spouse’s career have value.

Education and training: Courts account for education received during marriage and career sacrifices made.

Standard of living: Courts try to maintain similar living standards for both spouses when possible.

Child custody: The custodial parent might receive more property, especially the marital home.

Tax consequences: Property division should account for different tax treatments of various assets.

Economic misconduct: Wasting marital assets or hiding income affects division.

Future needs: Courts consider each spouse’s financial needs going forward.

| State | Considers Fault | Special Factors | Typical Split |

|---|---|---|---|

| New York | No | Enhanced earning capacity | 50/50 to 60/40 |

| Florida | No | Intentional asset waste | Equal presumption |

| Virginia | Yes | Monetary/non-monetary contributions | Variable |

| Illinois | No | Dissipation of assets | Equitable, not equal |

| Pennsylvania | Yes | Marital fault considered | Variable |

| North Carolina | Yes | Economic misconduct | Equitable |

| Georgia | No | Future earning capacity | Equitable |

Some states consider marital fault (adultery, abuse) when dividing property. Most states separate fault from property division, focusing only on financial factors.

States also differ on waiting periods and grounds for divorce, which affect how quickly property division resolves.

Property Settlement Strategies

Smart negotiation and understanding tax implications can significantly improve your property settlement outcome. Most couples settle property division through negotiation rather than trial.

Negotiating Your Property Settlement

Settlement negotiations let you control the outcome rather than leaving decisions to a judge. You know your situation better than any judge who hears your case for a few hours.

Identify your priorities before negotiating. What assets matter most to you? The house? Retirement accounts? Business? List your top three must-haves and items you’re willing to trade.

Consider total net value instead of fighting over specific items. A house worth $400,000 with a $250,000 mortgage provides only $150,000 in equity. Retirement accounts grow tax-deferred but trigger taxes when withdrawn. Compare apples to apples.

Use offsetting assets to avoid actually dividing certain property. Keep your retirement account while your spouse keeps the house equity. This approach works when both assets have similar values.

Trade immediate value for future income. You might accept less property now in exchange for higher alimony payments later. This strategy works when you need cash flow more than lump sum assets.

Divorce mediation helps couples negotiate creative settlements. A neutral mediator facilitates discussions and suggests options both parties might not consider. Mediation costs less than litigation and gives you more control.

Tax Considerations in Property Division

Property division carries significant tax consequences. Understanding these implications helps you negotiate better settlements.

Capital gains taxes apply when selling appreciated assets. Your house bought for $200,000 now worth $500,000 has $300,000 in gains. Each spouse can exclude $250,000 in gains from taxes ($500,000 for joint filers). Timing matters: selling before divorce finalizes might save taxes.

Retirement account divisions avoid taxes when done properly. QDROs for 401(k)s and transfers incident to divorce for IRAs move money tax-free. Taking early withdrawals to pay your spouse triggers income tax plus 10% penalties.

Asset basis matters for future taxes. Stocks with low basis create bigger tax bills when sold. A $50,000 stock portfolio purchased for $20,000 has $30,000 in built-in gains. Compare this to a $50,000 savings account with no tax consequences.

Alimony vs property division has different tax treatment. Alimony is no longer deductible or taxable under current law (divorces after 2018). Property division isn’t taxable. This affects negotiation strategies.

| Asset Transfer | Immediate Tax | Future Tax Impact |

|---|---|---|

| House (under $250k gain/person) | None | None if sold correctly |

| Retirement (QDRO) | None | Taxed when withdrawn |

| Stock Sale | Capital gains | Depends on holding period |

| Cash/Checking | None | None |

| Alimony | None | None (post-2018 divorces) |

Using Property Division Calculators

Online calculators help you estimate how courts might divide your property. These tools provide starting points for negotiations but can’t replace legal advice for complex situations.

Calculate Your Property Division

Understanding how your assets and debts might be divided helps you negotiate better settlements. Our calculator estimates property division based on your state’s laws and your specific situation.

Calculator features:

- State-specific property division rules (community vs equitable)

- Asset and debt inventory

- Marital vs separate property classification

- Estimated division outcomes

- Comparison of keeping vs selling options

Questions about property division or need legal help? Find Divorce Lawyers – Free Consultation Email: [email protected]

Calculators work best for straightforward situations. Complex assets like businesses, stock options, or hidden assets require professional valuation. Use calculator results as conversation starters with your attorney, not final answers.

Consider using our alimony calculator alongside property division estimates. Alimony and property division interact in settlement negotiations. Higher property awards might mean lower alimony, and vice versa.

Frequently Asked Questions About Property Division

Does a Wife Always Get Half the House?

No. Neither spouse automatically gets any specific percentage of the house. Community property states presume equal division of marital property including home equity. Equitable distribution states divide property fairly, which might mean the wife receives more, less, or equal to half depending on various factors.

The wife might receive the house (or more than half its value) when she’s the primary custodial parent and keeping children in the marital home serves their best interests. Alternatively, the husband might keep the house if he can afford it and the wife receives offsetting assets.

How Is Property Divided in a 70/30 Split?

A 70/30 split means one spouse receives 70% of the marital property’s total value while the other gets 30%. Courts calculate total marital assets, subtract marital debts, then divide the net value accordingly.

Equitable distribution states commonly produce unequal splits based on factors like marriage length, income disparity, fault (in some states), and future needs. Community property states rarely deviate from 50/50 unless both spouses agree.

What Assets Cannot Be Split in a Divorce?

Separate property cannot be divided in divorce. This includes property owned before marriage, inheritances received by one spouse, gifts given to only one spouse, and property designated as separate in a prenuptial agreement.

However, separate property can become marital property through commingling or transmutation. Depositing an inheritance in a joint account or adding your spouse’s name to your premarital property deed converts it to marital property subject to division.

Can You Divorce Without Splitting Assets?

Yes, but only if both spouses agree to skip property division or have no marital assets to divide. A valid prenuptial agreement might waive property division rights. Some couples complete uncontested divorces by agreeing who keeps what without court involvement.

Courts generally won’t approve settlements that leave one spouse destitute while the other keeps everything. Settlements must be fundamentally fair, even if not equal. Heavily one-sided agreements raise red flags about coercion or lack of understanding.

How Do You Calculate Property Division in Divorce?

Calculation depends on whether you’re in a community property or equitable distribution state. Community property states divide marital property equally (50/50). Equitable distribution states weigh multiple factors to determine fair percentages.

The basic process: (1) Classify each asset as marital or separate, (2) Determine fair market value of all marital assets, (3) Add up marital debts, (4) Calculate net marital estate (assets minus debts), (5) Apply state law to divide the net estate. Professional appraisers, accountants, and attorneys help with complex property.

What Is the 10/10/10 Rule for Divorce?

The 10/10/10 rule applies specifically to military pension division. It requires: (1) 10 years of marriage, (2) overlapping with 10 years of military service, (3) for the Defense Finance and Accounting Service to make direct payments to the ex-spouse.

Without meeting this rule, military pensions can still be divided, but the service member must make payments directly to the ex-spouse rather than through automatic military payroll deduction.

Who Loses More Financially in a Divorce?

Women typically experience greater financial decline after divorce than men, according to research. Women’s household income drops an average of 41% while men’s drops 23%. This disparity stems from career gaps while raising children, lower lifetime earnings, and receiving primary custody requiring child-related expenses.

However, individual outcomes vary significantly based on income levels, asset types, state laws, and settlement terms. High-earning women might fare better than lower-earning husbands. Age, health, and earning capacity matter more than gender in many cases.

How Does Moving Out Affect Property Division?

Moving out doesn’t forfeit your property rights. You maintain equal ownership of marital property regardless of who stays in the house. This common misconception prevents some spouses from leaving abusive situations.

However, moving out can affect temporary support and custody arrangements. The spouse remaining in the house might argue they should keep it permanently for children’s stability. Document your reasons for leaving and maintain financial contributions to the mortgage and household expenses.

Moving out establishes a separation date in some states, which determines when new property acquisitions become separate instead of marital. Consult an attorney before moving to understand implications in your state.

Can Hidden Assets Be Discovered After Divorce is Final?

Yes. Discovering hidden assets after divorce finalizes can reopen your case. Most states allow reopening a divorce judgment when fraud is proven. The innocent spouse must file a motion showing the other spouse concealed assets and this concealment affected the property division.

Time limits vary by state. Some states impose strict deadlines (like 1-2 years) while others allow reopening indefinitely if fraud is proven. Hidden assets discovered years later still provide grounds for modification in many jurisdictions.

What Happens to Property Acquired During Separation?

Property and income acquired after separation typically becomes separate property. The separation date marks when marital property accumulation stops. However, states define “separation” differently.

Some states require physical separation (living apart). Others recognize legal separation while still living together if one spouse expressed intent to end the marriage. The separation date affects which property is marital and which is separate, making proper documentation critical.

Do Prenuptial Agreements Always Hold Up in Court?

Prenuptial agreements usually hold up if properly drafted and executed. Courts enforce prenups when both parties: (1) fully disclosed their assets and debts, (2) had independent legal counsel or opportunity to consult counsel, (3) signed voluntarily without coercion, and (4) included fair terms.

Courts may invalidate prenups with unconscionable terms, those signed under duress, or agreements where one party hid significant assets. Having separate attorneys review the agreement before signing strengthens its enforceability.

How Are Debts Divided if Only One Spouse’s Name Is on the Account?

Debts incurred during marriage for marital purposes are typically marital debts regardless of whose name appears on the account. Courts divide these debts using the same community property or equitable distribution rules that apply to assets.

Your spouse’s credit card with only their name still becomes your responsibility if charges benefited the marriage (groceries, utilities, home repairs). However, debts for affairs, gambling, or other non-marital purposes might stay with the spouse who incurred them.

Can I Keep My Spouse from Selling Assets During Divorce?

Yes. Courts issue temporary restraining orders preventing asset dissipation during divorce proceedings. These automatic orders typically activate when divorce papers are filed, prohibiting both spouses from selling, transferring, or wasting marital assets without court approval or written agreement.

Violations of these orders result in contempt charges and penalties. Document any suspicious transfers or sales and report them to your attorney immediately. Courts can void improper transfers and award additional property to the harmed spouse.

What If My Spouse Refuses to Sell the House?

If you cannot agree on whether to sell the house, courts decide for you. Contested divorce proceedings let judges order house sales when spouses disagree. The court considers factors like children’s needs, each spouse’s ability to afford the house, and whether selling makes financial sense.

Some judges order buyouts where one spouse purchases the other’s equity share. Others force sales with proceeds divided according to each spouse’s property division percentage. Mediation often resolves house disputes without trial.

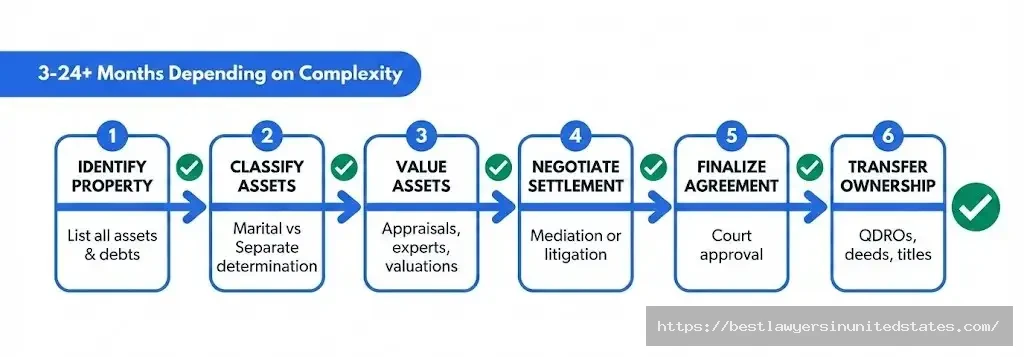

How Long Does Property Division Take in Divorce?

Property division timeline varies from 3 months to 2+ years depending on complexity and cooperation. Uncontested divorces where couples agree on property division settle fastest, often within 3-6 months.

Contested divorces with complex assets, business valuations, or hidden asset investigations take 12-24+ months. Discovery, valuations, and trial scheduling extend timelines significantly. Using mediation or collaborative divorce speeds the process compared to traditional litigation.

Should I File Taxes Jointly During Divorce?

Filing jointly usually provides better tax outcomes but requires cooperation and trust. Joint filing offers lower tax rates and higher standard deductions. However, joint filing makes both spouses liable for any tax debt or audit issues.

File jointly only if you trust your spouse’s reported income and deductions. Consider married filing separately if you suspect your spouse of tax fraud or underreporting income. Discuss filing status with a tax professional and divorce attorney before deciding.

Protecting Your Assets During Property Division

Property division represents one of the most important financial decisions you’ll make. Understanding your state’s property division system, knowing what constitutes marital versus separate property, and recognizing the value of different assets protects your financial future.

Whether you’re in a community property state expecting a 50/50 split or an equitable distribution state where judges weigh multiple factors, accurate asset valuation and strategic negotiation matter. Complex assets like businesses, retirement accounts, and digital currencies require professional expertise to value and divide properly.

Hidden assets destroy trust and lead to severe penalties. Full financial disclosure protects both spouses and ensures fair settlements. If you suspect your spouse is hiding assets, forensic accountants and legal discovery tools can uncover the truth.

Most importantly, remember that property division affects your financial security for years after divorce. Consider both immediate and long-term consequences. That house with significant equity might create tax bills when sold. Retirement accounts grow over time but face taxes when withdrawn. Balance current needs with future financial health.

Ready to understand your property division options?

Use our divorce cost calculator to estimate your total divorce expenses including property division costs. Calculate potential alimony payments and child support obligations to see your complete financial picture.

Find experienced divorce attorneys in your area who can evaluate your situation and protect your property rights. Most family law attorneys offer free initial consultations.

For more information about the divorce process, explore our guides on divorce steps, types of divorce, and divorce with children.