The marital home typically goes to the spouse who can afford it, needs it most for children, or agrees to buy out the other’s share. In most divorces, couples either sell the house and split proceeds or one spouse keeps it by refinancing and compensating the other for their equity. Courts consider custody arrangements, income levels, and state property division laws when deciding who gets the house.

Your home represents more than just your biggest asset. It holds memories, provides stability for children, and often carries significant emotional weight. According to the U.S. Census Bureau, 53.4% of divorcing couples in 2022 owned their homes, making property division one of the most complex aspects of divorce finances.

This guide explains how courts decide house ownership, what options you have, and the practical steps to transfer property after divorce. You’ll learn about refinancing requirements, buyout calculations, and state-specific rules that affect your situation.

Understanding Marital Property vs. Separate Property

Property classification determines whether your house gets divided in divorce. The distinction between marital and separate property varies by state but follows general principles across the country.

What Makes a House Marital Property?

A house becomes marital property when purchased during marriage using income earned during marriage. The name on the deed does not matter. If you bought the home after your wedding date, both spouses own it regardless of whose paycheck funded the down payment.

Courts presume any real estate acquired during marriage is marital property. Both spouses contributed to the household either through income, homemaking, or child care. These contributions give both parties an ownership interest that must be divided.

Key factors that make a house marital property:

- Purchased during marriage with marital income

- Mortgage payments made with joint funds

- Both names on deed or mortgage

- Refinanced during marriage using marital income

- Home improvements paid with joint savings

When a House Remains Separate Property

Your house stays separate property if you owned it before marriage and kept it completely separate from marital funds. No joint mortgage payments, no shared renovation costs, no commingling.

Inherited or gifted homes also remain separate property if you receive them in your name only. Your grandmother’s house becomes yours alone when she leaves it to you specifically, not to both spouses.

Separate property requirements:

- Owned before marriage with documented proof

- Received as personal gift or inheritance

- Never used marital funds for payments

- Title never changed to include spouse

- Kept finances completely separate

One Texas woman kept her pre-marriage condo as separate property by paying the entire mortgage from her individual account for 12 years. Her husband never contributed a dollar, and she kept meticulous records. The court confirmed it remained her separate property.

The Gray Area Situations

Most divorce cases involve houses that blur the line between separate and marital property. A home owned before marriage but improved with joint funds creates a partial marital interest. The spouse who didn’t originally own the property may claim part of the equity.

Common gray area scenarios:

- Pre-marriage home with mortgage paid by both spouses

- Inherited house renovated with marital savings

- Separate property home refinanced during marriage

- One name on deed but both names on mortgage

- Gift from parents used as down payment

California Family Code Section 2640 allows reimbursement for separate property contributions to community assets. If you used $50,000 in separate funds for a down payment, you might receive that amount back before dividing remaining equity.

The burden of proof falls on the spouse claiming separate property. You need bank statements, inheritance documents, and clear records showing no commingling occurred.

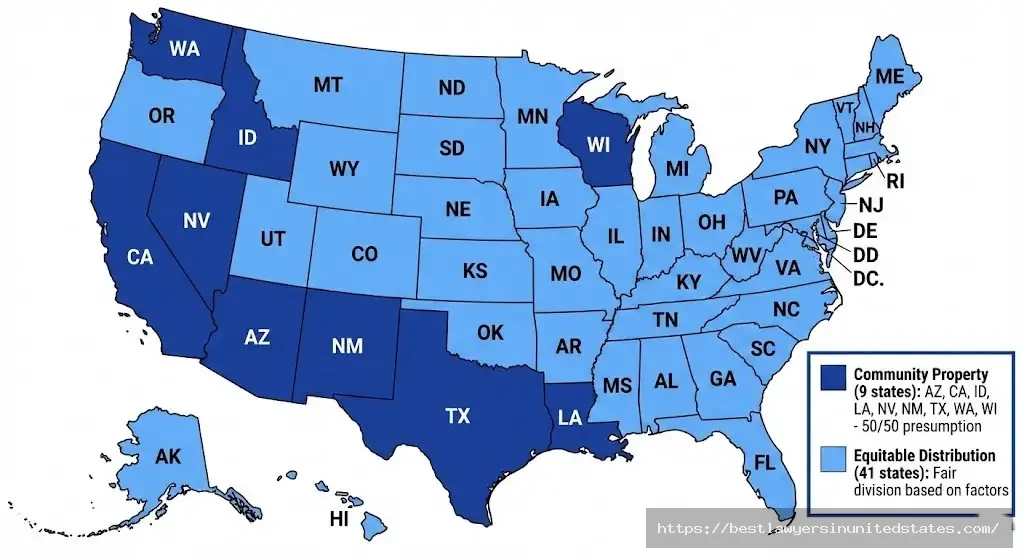

Community Property vs. Equitable Distribution: How Your State Divides Houses

State law determines how courts divide your house. The United States uses two property division systems that take fundamentally different approaches to splitting marital assets.

Community Property States (9 States)

Nine states presume all marital property belongs equally to both spouses: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. Alaska allows couples to opt into community property treatment.

Community property rules start with a 50/50 split. Your house gets divided equally unless specific exceptions apply. One spouse contributed separate property funds or one spouse wasted marital assets gambling.

Community property state rules:

- All property acquired during marriage is owned 50/50

- Separate property stays separate only if never commingled

- Equal division presumed but not always required

- Courts can deviate for fairness in some states

- Inheritance and gifts remain separate if kept separate

Texas follows strict community property rules under Texas Family Code Title 1. If you bought a house during marriage in Texas, both spouses own exactly half regardless of whose name appears on documents. Understanding divorce costs in Texas helps you budget for the division process.

Equitable Distribution States (41 States + DC)

Most states use equitable distribution, which means fair division rather than equal division. Courts consider multiple factors to determine what split seems most just given your circumstances.

Factors courts evaluate in equitable distribution states:

- Length of the marriage

- Income and earning capacity of each spouse

- Age and health conditions

- Contributions to marital property (financial and non-financial)

- Child custody arrangements

- Standard of living during marriage

- Tax consequences of property division

- Other assets each spouse receives

Pennsylvania follows equitable distribution under 23 Pa.C.S. Section 3502. The typical divorce cost in Pennsylvania ranges from $10,000 to $25,000 for contested cases involving property division disputes.

New York courts consider 10 specific factors when dividing marital property. A 30-year marriage where one spouse sacrificed career advancement to raise children might result in a 60/40 or 70/30 split favoring the lower-earning spouse.

State-by-State Quick Reference

| State | Property System | Separate Property Rules | House Division Approach |

|---|---|---|---|

| California | Community Property | Pre-marriage + inheritance | Presumed 50/50 split |

| Texas | Community Property | Strict separation required | 50/50 starting point |

| Florida | Equitable Distribution | Pre-marriage protected | Fair division based on factors |

| New York | Equitable Distribution | Pre-marriage + gifts protected | 10-factor analysis |

| Pennsylvania | Equitable Distribution | Pre-marriage + inheritance | Contribution-based |

| Illinois | Equitable Distribution | Clear documentation needed | Multi-factor evaluation |

| Ohio | Equitable Distribution | Transmutation possible | Fairness over equality |

| Georgia | Equitable Distribution | Active vs passive appreciation | Contributions matter |

Each state’s approach affects whether you keep the house or must sell. Divorce laws by state vary significantly on property division timelines and procedures.

Who Gets the House When You Have Children?

Children’s needs often tip the scales in house ownership decisions. Courts prioritize stability and continuity for minor children when determining which parent keeps the marital home.

How Child Custody Affects House Decisions

The custodial parent usually has a stronger claim to keep the house. Judges want children to remain in familiar surroundings with minimal disruption to their education and social connections.

Research shows moving after divorce increases behavioral problems in children by 23%. Keeping kids in the same school district and neighborhood helps them adjust during an already difficult transition.

Custody considerations for house ownership:

- Primary physical custody often means keeping the home

- School district quality and continuity

- Distance from both parents’ work

- Children’s ages and attachment to home

- Ability to maintain mortgage and expenses

Divorce cases involving children require additional planning around child support obligations. Use our child support calculator to estimate monthly payments based on custody arrangements and state guidelines.

Temporary Orders During Divorce

Courts issue temporary orders that specify who stays in the house while divorce proceedings continue. These orders typically last 6 to 18 months until the final decree.

The spouse remaining in the home usually pays the mortgage, property taxes, insurance, and utilities. The other spouse may receive a small credit against their support obligation, called a mortgage deviation.

Temporary possession does not determine final ownership. Moving out during divorce does not forfeit your property rights, though it may affect custody considerations.

Long-Term Custody Arrangements and House Ownership

Some divorce decrees allow the custodial parent to remain in the home until the youngest child graduates high school. The house then gets sold and proceeds divided according to the original agreement.

Delayed sale agreements typically include:

- Specific sale date or triggering event (graduation, age 18)

- Maintenance and repair responsibilities

- Mortgage payment obligations

- Buyout option terms

- What happens if one parent wants to sell early

Bird’s nest custody arrangements keep children in the family home while parents rotate in and out. This rare approach works for couples committed to co-parenting cooperation and who can afford two additional residences.

Can You Afford to Keep the House? Financial Reality Check

Emotional attachment to your home can cloud financial judgment. Running the numbers reveals whether keeping the house makes sense for your post-divorce budget.

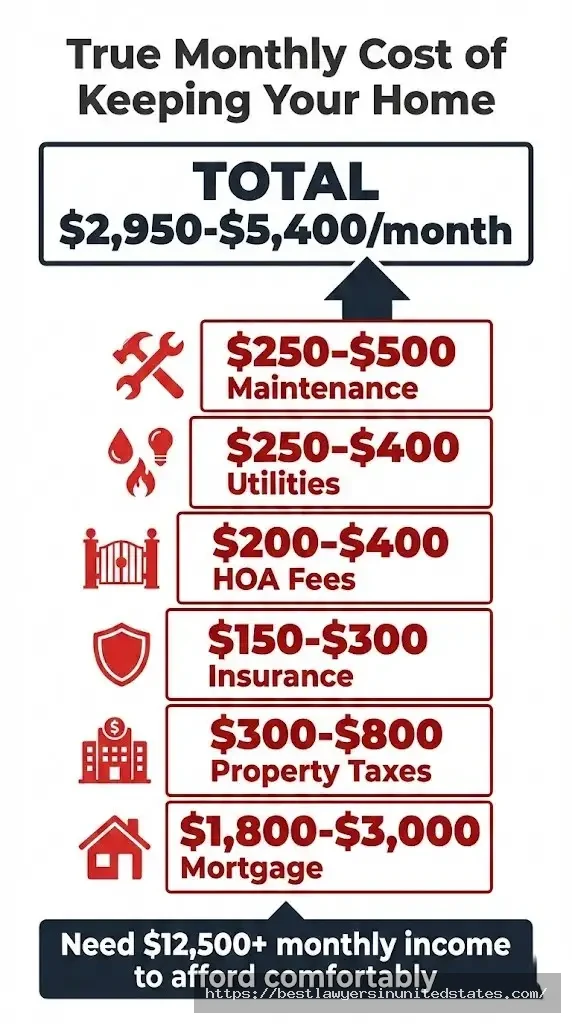

The True Cost of Keeping Your Marital Home

Your monthly housing expenses include far more than the mortgage payment. Property taxes, insurance, utilities, maintenance, and repairs add up quickly on a single income.

Complete monthly housing cost breakdown:

| Expense Category | Average Monthly Cost | Annual Cost |

|---|---|---|

| Mortgage Principal & Interest | $1,800 – $3,000 | $21,600 – $36,000 |

| Property Taxes | $300 – $800 | $3,600 – $9,600 |

| Homeowner’s Insurance | $150 – $300 | $1,800 – $3,600 |

| HOA Fees (if applicable) | $200 – $400 | $2,400 – $4,800 |

| Utilities (electric, gas, water) | $250 – $400 | $3,000 – $4,800 |

| Maintenance & Repairs | $250 – $500 | $3,000 – $6,000 |

| Total Monthly | $2,950 – $5,400 | $35,400 – $64,800 |

Financial experts recommend housing costs stay below 28% of gross monthly income. If you earn $6,000 per month, you should spend no more than $1,680 on housing. A $3,500 monthly housing cost requires $12,500 in monthly income to stay financially healthy.

Refinancing Requirements After Divorce

Refinancing removes your ex-spouse from the mortgage and proves you can handle the debt alone. Lenders evaluate your individual income, credit score, and debt-to-income ratio without considering your ex-spouse’s finances.

Minimum refinancing qualifications:

- Credit score of 620+ (conventional loans)

- Debt-to-income ratio below 43%

- Stable employment for 2+ years

- Sufficient income to cover mortgage payments

- Home appraisal supporting loan amount

- 3-6 months of reserves recommended

Divorce decrees typically require refinancing within 60 to 180 days after the final order. If you cannot qualify within that timeframe, the court may order the house sold instead.

Calculate your potential divorce expenses including legal fees and refinancing costs with our divorce cost calculator. Understanding total costs helps you decide whether keeping the house fits your budget.

Buyout Options and Calculations

Buying out your spouse means compensating them for their share of the home’s equity. Home equity equals current market value minus outstanding mortgage balance.

Simple buyout calculation:

Home Value: $400,000

Mortgage Balance: -$250,000

Home Equity: $150,000

Your Buyout (50%): $75,000You need $75,000 cash or equivalent assets to buy your spouse out. Most people refinance the mortgage for an amount large enough to pay off the existing loan plus the buyout amount.

Alternative buyout methods:

- Cash payment from savings or family loans

- Trading other assets (retirement accounts, investments)

- Payment plan over time (risky and uncommon)

- Offsetting with your share of other property

- Keeping more debt in exchange for house

The alimony calculator helps you understand potential spousal support obligations that might affect your ability to afford the house buyout.

The Hidden Costs of Keeping the House

Beyond monthly expenses, keeping the house carries opportunity costs and emotional burdens that affect your quality of life.

Tying up equity in the house means less money for retirement savings, emergency funds, and enjoying life post-divorce. A $150,000 equity position could generate $6,000 to $9,000 annually if invested in a diversified portfolio.

Real example comparison:

Option A: Keep $400,000 House

- Monthly payment: $3,500

- Annual housing: $42,000

- Investment income: $0

- Financial stress: High

Option B: Sell and Buy $200,000 Townhome

- Monthly payment: $1,800

- Annual housing: $21,600

- $150,000 invested generating 5%: $7,500/year

- Financial stress: Low

- Annual savings: $27,900

Many people who keep the house report feeling “house poor” within the first year. You own a beautiful home but lack funds for vacations, dining out, or hobbies that make life enjoyable.

Your Options for the Marital Home

Divorcing couples have four main options for handling the family home. Each approach carries distinct advantages and challenges depending on your financial situation and relationship.

Option 1: Sell the House and Split Proceeds

Selling creates a clean break with both spouses receiving liquid cash from their share of equity. This option works well when neither spouse can afford the house alone or when you want to eliminate all financial ties.

Advantages of selling:

- Complete financial separation

- Both spouses get cash for fresh start

- No refinancing required

- Eliminate joint mortgage liability

- Fair market value determines split

Disadvantages of selling:

- Selling costs eat 6% to 10% of home value

- Current market conditions might be unfavorable

- Children lose stability and familiar surroundings

- Possible capital gains tax on appreciation

- Emotional difficulty leaving family home

The selling process requires both spouses to cooperate on listing price, realtor selection, and closing documents. Uncontested divorce cases typically handle house sales more smoothly than contentious splits.

Option 2: One Spouse Keeps the House (Buyout)

One spouse refinances the mortgage in their name alone and compensates the other for their equity share. This option provides stability but requires qualifying for a new loan on single income.

Buyout process steps:

- Order professional home appraisal ($400-$600)

- Calculate net equity (value minus mortgage)

- Determine buyout amount (typically 50% of equity)

- Apply for refinancing with new lender

- Close on new mortgage and pay buyout

- Transfer deed via quitclaim deed

- File deed with county recorder ($50-$150)

- Update homeowner’s insurance

Advantages of keeping the house:

- Stability for children in same school

- Maintain established neighborhood connections

- Build equity over time

- Avoid moving expenses and hassle

- Keep familiar home environment

Disadvantages of keeping the house:

- Refinancing required within tight deadline

- Significant cash needed for buyout payment

- All maintenance and repair burden falls on one person

- Risk of being house poor on single income

- Emotional reminders of marriage in every room

Review the complete divorce process steps to understand how property division fits into overall divorce timeline and requirements.

Option 3: Co-Own Temporarily (Delayed Sale)

Temporary co-ownership allows both spouses to remain on the deed and mortgage while deciding the home’s fate later. This arrangement typically lasts 1 to 5 years with a specific end date.

When delayed sale makes sense:

- Housing market down, waiting for recovery

- Children finishing high school in 2-3 years

- Neither spouse can afford buyout currently

- Tax timing considerations for capital gains

- One spouse needs time to improve credit

Required agreement terms:

- Specific sale date or triggering event

- Who lives in the home during delay

- Mortgage and expense payment split

- Maintenance and repair responsibilities

- Dispute resolution procedures

- Buyout option terms and deadlines

Risks of co-ownership:

- Continued financial entanglement with ex-spouse

- Both remain liable if either defaults on mortgage

- Disagreements over repairs and improvements

- Complicates new relationships

- Either spouse’s financial problems affect both

One spouse defaulting on agreed payments creates immediate problems. The other spouse faces credit damage if the mortgage goes unpaid, even if they made their share of payments on time.

Contested divorce cases rarely result in successful co-ownership arrangements due to high conflict levels between spouses.

Option 4: Convert to Rental Property

Converting the marital home to a rental property lets both spouses retain ownership and receive rental income. This option requires an investment mindset and strong communication.

Rental conversion considerations:

- Both spouses agree to landlord responsibilities

- Property management company recommended ($150-$300/month)

- Rental income split according to divorce decree

- Tax implications for rental property income

- Maintenance and capital improvement decisions

- Exit strategy with clear buyout terms

- Insurance changes from homeowner to landlord policy

Rental property co-ownership rarely succeeds long-term. Most couples include a 3 to 5-year timeline before requiring sale or buyout.

Special Situations: Complex House Ownership Scenarios

Several common situations complicate house division beyond straightforward marital property. Understanding how courts handle these scenarios helps you plan realistic expectations.

House in One Spouse’s Name Only

The name on the deed does not determine ownership in divorce. A house purchased during marriage belongs to both spouses as marital property regardless of whose name appears on title documents.

Courts override deed names when dividing marital property. State law presumes joint ownership of assets acquired during marriage using marital income. The spouse claiming sole ownership must prove the house is separate property with clear evidence.

One-name deed scenarios:

- Wife’s name on deed, husband’s income bought house = marital property

- Husband on deed alone, wife paid half of mortgage = marital property

- One spouse only for credit reasons = still marital property

- Purchased during marriage = marital unless proven separate

House Bought Before Marriage

Pre-marriage home ownership creates separate property, but marital contributions convert part of the equity to marital property. The longer the marriage and the more joint funds used, the larger the marital interest.

Formula for partial marital interest:

Marital Interest = (Marital Contributions ÷ Current Home Value) × Total Equity

Example:

- Home value at marriage: $200,000

- Mortgage at marriage: $150,000

- Current home value: $350,000

- Current mortgage: $100,000

- Current equity: $250,000

- Marital payments: $50,000 + $30,000 improvements = $80,000

Marital Interest = ($80,000 ÷ $350,000) × $250,000 = $57,143

Separate Property = $250,000 - $57,143 = $192,857The spouse who owned the home before marriage receives the separate property portion. The remaining equity gets divided according to state property division laws.

Inherited or Gifted House

Houses received through inheritance or personal gifts remain separate property if kept completely separate from marital funds. Using joint money for any purpose converts part of the home to marital property.

Separate property protection rules:

- Must be gifted or inherited to one spouse only

- Never use marital funds for mortgage payments

- No joint funds for renovations or improvements

- Keep separate bank accounts for all payments

- Document all transactions meticulously

- Refinancing can change separate to marital

Selling an inherited house and buying a new home with proceeds typically creates marital property. The new house was purchased during marriage, eliminating separate property protection.

House Underwater (Negative Equity)

Owing more than your home’s worth creates unique challenges in divorce. Both spouses remain liable for the full mortgage amount regardless of who keeps the house or what the divorce decree says.

Underwater house options:

- Continue joint payments until equity returns

- One spouse keeps house and full debt

- Short sale with lender approval

- Deed in lieu of foreclosure

- Strategic default (damages both credit scores)

| Scenario | Home Value | Mortgage Balance | Negative Equity |

|---|---|---|---|

| Typical Underwater | $250,000 | $290,000 | -$40,000 |

| Severe Underwater | $180,000 | $275,000 | -$95,000 |

Lenders cannot be forced to reduce mortgage balances in divorce. Both spouses signed the original loan agreement and remain equally responsible until the mortgage is paid off or refinanced.

Second Homes, Vacation Properties, Investment Properties

Additional properties follow the same marital versus separate property rules as primary residences. Multiple properties often get divided strategically with each spouse receiving different assets.

Strategic property division examples:

- Spouse A keeps primary residence ($400,000 equity)

- Spouse B keeps vacation home ($200,000 equity) + retirement account ($200,000)

- Both values balance to $400,000 each

Investment properties generating rental income require special consideration for tax implications and ongoing management responsibilities.

What Courts Consider When Deciding Who Gets the House

Judges evaluate multiple factors when determining house ownership if you cannot reach agreement. Understanding these considerations helps you build a stronger case or negotiate more effectively.

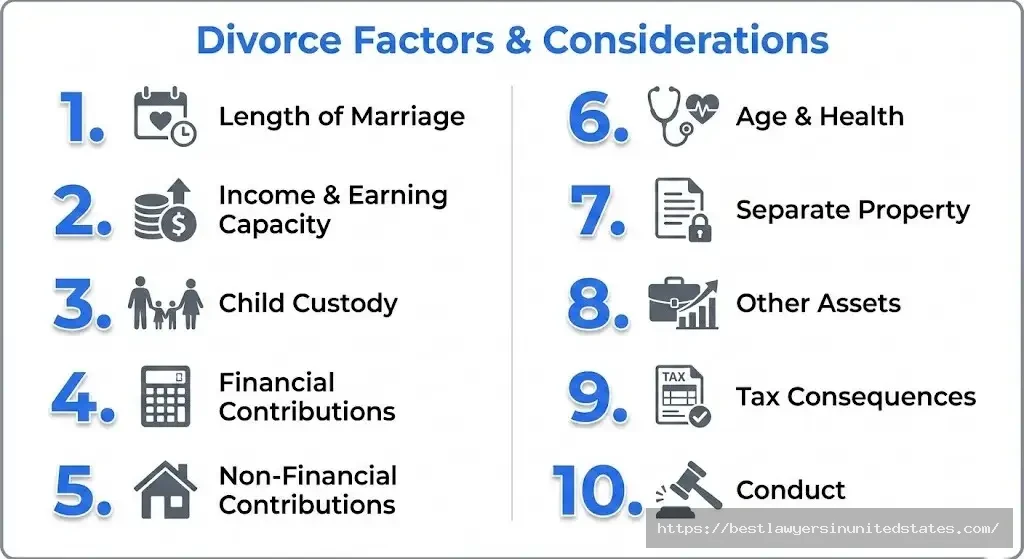

The 10 Key Factors Judges Evaluate

1. Length of Marriage

Longer marriages typically result in more equal property splits. A 25-year marriage receives different treatment than a 3-year marriage.

2. Income and Earning Capacity

Courts analyze who can afford to maintain the house long-term. Current income and future earning potential both matter.

3. Child Custody Arrangements

Primary custodial parents often receive preference for keeping the home to maintain children’s stability.

4. Financial Contributions

Who paid the down payment, made mortgage payments, and funded major improvements affects division decisions.

5. Non-Financial Contributions

Stay-at-home parenting, homemaking, and supporting the other spouse’s career count as valuable contributions.

6. Age and Health

Older spouses or those with health conditions may need the stability of remaining in the family home.

7. Separate Property Components

Pre-marriage ownership or inheritance portions affect how much of the house is divisible.

8. Other Assets Available

Courts consider whether other assets can offset the home’s value for fair overall distribution.

9. Tax Consequences

Capital gains taxes and mortgage interest deductions influence decisions about who benefits most from keeping the house.

10. Conduct and Fault

Some states consider marital misconduct or dissipation of assets when dividing property.

When the Judge Orders a Sale

Courts order house sales when neither spouse can afford buyouts, both want the house, or selling is the only way to divide equity fairly.

Common sale order scenarios:

- Neither spouse qualifies for refinancing

- Both spouses insist on keeping the house

- House represents most marital assets

- Negative equity requires shared loss

- Contentious relationship prevents co-ownership

Forced sales typically happen within 60 to 120 days after the court order. Both spouses must cooperate on listing price, realtor selection, and accepting offers.

Temporary vs. Permanent Orders

Temporary orders address immediate housing needs during divorce proceedings. Permanent orders in the final divorce decree establish long-term property ownership.

| Order Type | Duration | Purpose | Modification |

|---|---|---|---|

| Temporary | 3-18 months | Who stays during divorce | Possible with changed circumstances |

| Permanent | Final | Long-term ownership | Difficult to modify |

Temporary possession does not predict final outcomes. Moving out voluntarily during proceedings does not forfeit your ownership rights or equity interest.

Step-by-Step: How to Transfer House Ownership After Divorce

Property transfer requires specific legal documents and procedures. Missing steps or incorrect paperwork creates title problems and potential liability issues.

Documents You’ll Need

Required transfer documents:

- Final Divorce Decree with property division terms

- Quitclaim Deed or Special Warranty Deed

- Professional home appraisal (for refinancing)

- Mortgage refinance approval letter

- New title insurance policy

- County recording fees ($50-$150 varies by location)

- Updated homeowner’s insurance policy

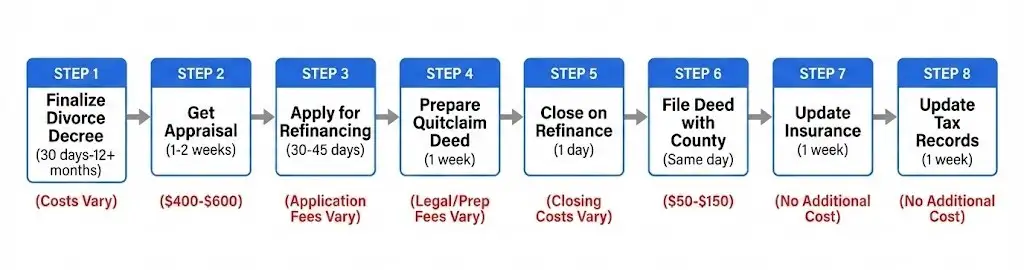

The Complete Transfer Process

Step 1: Finalize Divorce Decree

Your divorce decree must include specific property transfer terms, legal description of property, and timeline for completing transfer. Most states require 30 days to 12+ months from filing to final decree.

Step 2: Obtain Professional Appraisal

Lenders require appraisals for refinancing. Professional appraisers charge $400 to $600 and take 1 to 2 weeks to complete reports.

Step 3: Apply for Refinancing

Submit income documentation, employment verification, and credit authorization to new lender. Approval takes 30 to 45 days for conventional loans.

Refinancing requirements checklist:

- Pay stubs for last 2 months

- W-2 forms for last 2 years

- Tax returns for last 2 years

- Bank statements for last 2 months

- Current mortgage statement

- Homeowner’s insurance information

- Credit score 620+ for conventional loans

Step 4: Prepare Quitclaim Deed

Hire real estate attorney or use online legal service to draft quitclaim deed. Document must match divorce decree terms exactly with correct legal description.

Step 5: Close on Refinance

Original mortgage gets paid off, new mortgage created in one spouse’s name only, and ex-spouse released from all liability.

Step 6: File Deed with County Clerk

Record quitclaim deed at county recorder’s office the same day as refinance closing. Recording fees range from $50 to $150 depending on county. You receive stamped recorded deed copy as proof.

Step 7: Update Homeowner’s Insurance

Remove ex-spouse from insurance policy, update beneficiaries, and adjust coverage amounts if needed. Premium may change based on single vs. married status.

Step 8: Update Property Tax Records

Notify county assessor’s office of ownership change. Update mailing address if needed for tax bills.

What If Your Ex Won’t Sign the Deed?

Divorce decrees are court orders with enforcement power. Your ex-spouse cannot refuse to comply without facing contempt charges.

Enforcement options:

- File contempt motion with family court

- Request judge sign on non-compliant spouse’s behalf

- Seek monetary sanctions for deliberate delays

- In some states, divorce decree itself serves as deed

Most states allow judges to sign property transfer documents when one spouse refuses to cooperate. Your attorney files a motion, the court holds a hearing, and the judge can execute the transfer over objections.

Removing Your Name from the Mortgage

Quitclaim deeds transfer ownership but do not affect mortgage liability. Only refinancing or paying off the loan removes your name from mortgage obligations.

Critical mortgage liability facts:

- Quitclaim deed ≠ mortgage release

- Both names remain liable until refinance

- Lenders are not bound by divorce decrees

- Default by ex-spouse damages your credit

- You can pay mortgage and sue ex for reimbursement

Assumption loans allow transferring existing mortgage to one spouse without refinancing, but lenders rarely approve these requests. The new sole borrower must qualify under current underwriting standards anyway.

Tax Implications of Divorce and House Division

Property transfers and sales during divorce carry significant tax consequences. Understanding rules helps you time decisions strategically and minimize tax liability.

Capital Gains Exclusion Rules

Single filers exclude up to $250,000 in capital gains from home sales. Married couples filing jointly exclude up to $500,000. Timing your sale relative to divorce finalization affects which exclusion applies.

Capital gains exclusion requirements:

- Owned home for 2+ years of last 5 years

- Used home as primary residence 2+ years of last 5 years

- Have not used exclusion in last 2 years

- Meet both ownership and use tests independently

Strategic timing example:

Married couple bought home in 2016 for $300,000. Current value is $750,000, creating $450,000 gain. If they sell before divorce finalizes, the $500,000 married exclusion covers the entire gain tax-free. If they wait until after divorce, each $250,000 single exclusion only covers $500,000 combined, leaving $50,000 taxable.

Tax calculation on $50,000 taxable gain:

Taxable Capital Gain: $50,000

Long-term Capital Gains Tax Rate: 15%

Tax Owed: $7,500Transferring House Between Spouses

Property transfers between spouses during divorce are tax-free under IRC Section 1041. No gift taxes, no capital gains taxes, and no income taxes apply to these transfers.

The receiving spouse takes on the original cost basis, meaning they inherit the tax situation. If your spouse bought the house for $200,000 and transfers it to you when it’s worth $400,000, your cost basis remains $200,000. When you later sell for $450,000, your capital gain is $250,000.

Cost basis transfer example:

Original Purchase Price (2010): $200,000

Value at Divorce Transfer (2026): $400,000

Your New Cost Basis: $200,000 (not $400,000)

Future Sale (2030): $450,000

Capital Gain: $450,000 - $200,000 = $250,000

After Exclusion: $250,000 - $250,000 = $0 taxableMortgage Interest Deduction

The spouse making mortgage payments claims the mortgage interest tax deduction. Divorce decrees should specify who receives this benefit if both names remain on the mortgage temporarily.

Only the legal owner living in the home can claim the deduction. If your ex-spouse keeps the house but you’re paying the mortgage per court order, you cannot claim the deduction despite making payments.

Common Mistakes to Avoid

Learning from others’ mistakes saves money and stress during house division. These errors appear frequently in divorce cases involving real estate.

Mistake 1: Moving Out and Assuming You Lost Rights

Moving out during divorce proceedings does not forfeit your property ownership or equity rights. You maintain your legal interest in marital property regardless of physical location.

Document your reasons for leaving in writing. Domestic violence, safety concerns, or mutual agreement for space all justify moving out without hurting your case. Courts understand that living together during contentious divorce creates difficult circumstances.

Mistake 2: Keeping House You Can’t Afford

Emotional attachment clouds financial judgment. The house you loved on two incomes becomes a financial burden on one salary.

Warning signs you cannot afford the house:

- Monthly housing costs exceed 35% of gross income

- No emergency fund for repairs and maintenance

- Cutting retirement contributions to make payments

- Using credit cards for basic living expenses

- Constant stress about money

- No funds for enjoying life

One divorced woman kept her $450,000 home but earned $65,000 annually. After two years of struggling, she sold at a loss to escape the financial pressure. Downsizing immediately would have saved $40,000 and eliminated years of stress.

Mistake 3: Not Getting Proper Appraisal

Zillow and Redfin estimates vary by 5% to 15% from actual market value. Online valuations miss property condition, local market nuances, and recent comparable sales that affect price.

Professional appraisers charge $400 to $600 but provide the accurate valuations lenders require for refinancing. You need this appraisal anyway, so get it early in the divorce process.

Mistake 4: Forgetting About Capital Gains Tax

Large home appreciation creates surprise tax bills if you don’t plan strategically. A $600,000 gain exceeds both single and married exclusions, creating taxes on $100,000 to $350,000 depending on filing status and timing.

Consult a CPA before finalizing property division. Tax planning saves thousands and helps you make informed decisions about selling versus keeping the house.

Mistake 5: Relying on Quitclaim Deed to Remove Mortgage

Quitclaim deeds transfer ownership but have zero effect on mortgage liability. The lender’s agreement with both borrowers remains in force until the mortgage is paid off or refinanced.

Both spouses remain 100% liable for the full mortgage amount. If your ex-spouse stops paying after you quitclaimed, the lender comes after both of you. Your credit score suffers, and you may face foreclosure despite signing over the house.

Mistake 6: Not Documenting Separate Property Claims

The burden of proof falls on the spouse claiming separate property. Without clear documentation, courts presume all property acquired during marriage is marital.

Essential documentation:

- Bank statements showing separate account deposits

- Inheritance or gift letters from donors

- Pre-marriage purchase agreements and title documents

- Records of all payments from separate accounts

- No commingling evidence

One California man lost his $200,000 inheritance claim because he deposited it in a joint account and used funds for marital expenses. The court ruled he commingled the inheritance, converting it to marital property.

Mistake 7: Agreeing to Co-Ownership Without Clear Terms

Vague co-ownership agreements create ongoing disputes and potential litigation. Every possible scenario needs written terms agreed upon in advance.

Required co-ownership agreement terms:

- Specific sale date (month/day/year) or triggering event

- Who lives in property during co-ownership

- Exact payment split for mortgage, taxes, insurance, utilities

- Maintenance and repair expense procedures and limits

- Major capital improvement approval process

- What happens if one spouse wants to sell early

- Buyout option terms and pricing formula

- Dispute resolution procedures

Without these detailed terms, you return to court repeatedly to resolve disagreements.

Mistake 8: Ignoring Home Equity Lines of Credit

HELOCs create debt secured by your home that must be addressed in property division. Many couples forget about these credit lines until after divorce finalizes.

A $50,000 HELOC with $35,000 drawn reduces net equity from $200,000 to $165,000. Make sure your settlement agreement addresses all debt secured by the property.

Frequently Asked Questions

Does it matter whose name is on the house deed in a divorce?

No. In most states, houses purchased during marriage are marital property regardless of whose name appears on the deed. Both spouses have an ownership interest that must be divided according to state property division laws.

The only exception is if the house was bought before marriage or with separate property funds that were kept completely separate from marital finances.

Can I be forced to sell my house in a divorce?

Yes. If you and your spouse cannot agree on house division and neither can afford a buyout, the judge can order sale of the marital home with proceeds divided according to state law.

Courts order forced sales when selling is the only practical way to divide equity fairly between spouses. You typically have 60 to 120 days to complete the sale after the court order.

What if my spouse owned the house before we married?

The house may be separate property, but if marital funds paid the mortgage, property taxes, or home improvements, you may have a claim to part of the equity or appreciation that occurred during marriage.

Courts calculate the marital interest based on contributions made during marriage. The formula considers both direct payments and appreciation in value.

Do I give up my rights to the house if I move out during divorce?

No. Moving out during divorce proceedings does not forfeit your ownership rights to marital property. Your equity interest remains protected regardless of where you live.

Document your reasons for leaving (safety, mutual agreement, space) to avoid any perception that you abandoned the property voluntarily.

How long do I have to refinance after divorce?

Divorce decrees typically specify 60 to 180 days to refinance the mortgage. If you cannot qualify within that timeframe, you must return to court for alternative arrangements.

The spouse keeping the house should apply for refinancing immediately upon filing for divorce to identify any obstacles early in the process.

Can I keep the house if I can’t refinance the mortgage?

Options include delayed refinancing with a specific deadline, offsetting your ex-spouse with other assets equal to their equity, selling the house, or keeping both names on the mortgage temporarily (risky).

Courts cannot force lenders to approve loans, so if refinancing proves impossible, the judge will likely order a sale instead.

What happens if my ex stops paying the mortgage after I moved out?

If both names remain on the mortgage, both are fully liable regardless of divorce decree terms. Missed payments damage both credit scores and can lead to foreclosure affecting both spouses.

You can make the payments yourself to protect your credit, then file a contempt motion seeking reimbursement from your ex-spouse. This is why refinancing to remove the non-occupying spouse is so important.

How is home equity calculated in divorce?

Home equity equals current market value minus outstanding mortgage balance minus estimated selling costs (if applicable).

Current Market Value: $400,000

Outstanding Mortgage: -$250,000

Home Equity: $150,000Get a professional appraisal rather than relying on online estimates. Zillow and Redfin valuations can be off by 5% to 15%, creating disputes over the actual equity amount.

Can we both stay in the house during divorce?

Yes, but it’s complicated and often contentious. Some couples do this to minimize costs or maintain stability for children. Others find it creates too much conflict.

Courts can issue temporary orders specifying who stays in the home during divorce proceedings. These orders typically last 6 to 18 months until the final decree.

What if we’re underwater on the mortgage (owe more than it’s worth)?

You’ll need to decide who takes the debt or whether to pursue options like short sale, loan modification, or continuing joint payments until equity returns.

Both spouses remain liable for the full mortgage amount until it’s paid off or refinanced. The lender has no obligation to reduce the balance due to divorce.

Get Professional Help With Your Divorce

Dividing your marital home involves complex legal, financial, and emotional considerations. The decisions you make affect your finances and housing stability for years after divorce finalizes.

Understanding your state’s property division laws helps you negotiate effectively or present a strong case to the judge. Whether your state follows community property rules or equitable distribution principles changes your approach and likely outcome.

Most divorcing couples choose between selling the house and splitting proceeds, one spouse buying out the other, or temporarily co-owning while deciding. Each option carries distinct pros and cons depending on your children’s needs, financial capacity, and relationship with your ex-spouse.

Refinancing typically costs $3,000 to $5,000 but removes your ex-spouse from mortgage liability and proves you can afford the house alone. Without refinancing, both spouses remain fully liable for the mortgage regardless of divorce decree terms.

Tax planning prevents expensive mistakes. Capital gains exclusions, basis transfers, and mortgage interest deductions all affect the net financial impact of your decisions. Consulting a CPA before finalizing property division saves thousands in unnecessary taxes.

Our divorce cost calculator helps you estimate total expenses including legal fees, filing costs, and property division expenses. Understanding complete costs helps you budget realistically for the process ahead.

Questions about dividing your house or need legal guidance? Email [email protected] or find divorce lawyers in your state offering free consultations. Professional advice tailored to your specific situation and state laws protects your interests throughout the divorce process.