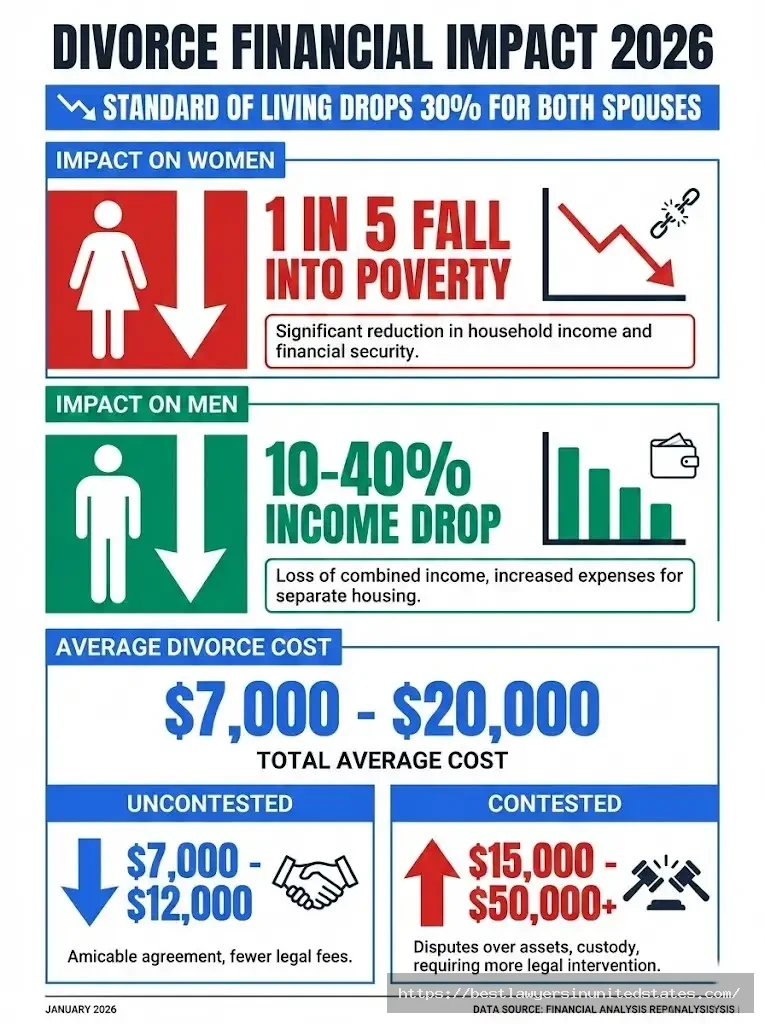

Divorce divides more than families. It splits bank accounts, retirement funds, homes, and financial futures. Most people see their standard of living drop by 30% or more after divorce, according to research from the Institute for Divorce Financial Analysts.

This guide explains how to protect your finances before, during, and after divorce. You’ll learn about asset division, spousal support, tax changes, and financial recovery strategies. Use our divorce cost calculator to estimate your total expenses based on your situation.

Understanding Divorce Finances: The Financial Reality of Separation

The average divorce costs between $7,000 and $20,000 in the United States. Filing fees alone range from $100 to $450 depending on your state. Attorney fees add $3,000 to $15,000 for uncontested cases and $15,000 to $50,000+ for contested divorces.

Women face unique financial challenges. One in five women falls into poverty after divorce. Men typically experience a 10-40% drop in their standard of living. Both spouses often struggle to maintain their previous lifestyle on divided assets and separate incomes.

Community Property vs Equitable Distribution States

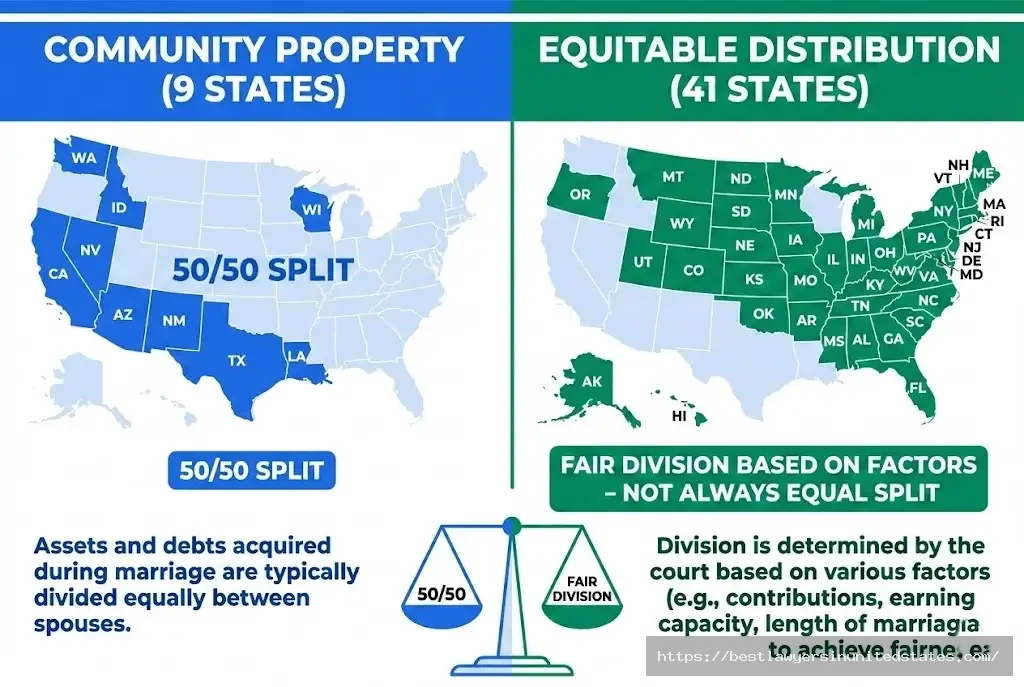

Your state’s property division system affects how assets are split. Nine states follow community property rules: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. These states split marital assets 50-50 regardless of who earned more.

The remaining 41 states use equitable distribution. Courts divide assets fairly based on factors like marriage length, income, and contributions. Fair doesn’t always mean equal. One spouse might receive 60% while the other gets 40%.

State Property Division Systems

| System Type | States | How It Works |

|---|---|---|

| Community Property | 9 states (AZ, CA, ID, LA, NV, NM, TX, WA, WI) | 50-50 split of marital assets |

| Equitable Distribution | 41 states + DC | Fair division based on multiple factors |

Understanding your state’s system helps you plan for what you’ll keep or lose. Check divorce laws by state for specific rules in your location.

Before You File: Financial Preparation Checklist

Smart preparation protects your assets and speeds up the divorce process. Start gathering documents and securing your finances at least 30-60 days before filing.

Gathering Critical Financial Documents

You need complete records of all shared finances. Collect recent statements for every account, loan, and asset. Missing documents delay settlement negotiations and cost you more in attorney fees.

Required Financial Documents

- Bank statements (checking and savings) from past 3 years

- Credit card statements showing all accounts

- Mortgage statements and home title documents

- Investment and brokerage account statements

- Retirement account statements (401k, IRA, pension)

- Tax returns from past 3-5 years

- Pay stubs or W-2 forms

- Business ownership documents

- Life, health, auto, and property insurance policies

- Estate planning documents (wills, trusts, powers of attorney)

Make copies of everything. Store digital copies in a secure cloud account your spouse can’t access. Keep physical copies with a trusted friend or family member. Learn more about required paperwork in our divorce process guide.

Understanding Your Assets and Liabilities

Separate marital property from separate property before negotiations begin. Marital property includes anything acquired during marriage. Separate property covers assets owned before marriage or inherited by one spouse.

Joint accounts need immediate attention. One angry spouse can drain accounts or max out credit cards. Document current balances and transaction history. Courts consider this evidence when dividing assets.

Debt division follows similar rules. Joint debts from marriage usually split between both spouses. Individual debts taken before marriage typically stay with the person who borrowed the money.

Protecting Your Credit Score

Open individual bank accounts before filing. Transfer your share of income and expenses to the new account. This prevents a spouse from cutting off your access to money.

Credit Protection Steps

- Check your credit report for joint accounts

- Freeze joint credit cards to prevent new charges

- Open individual credit cards in your name only

- Remove spouse as authorized user on your accounts

- Monitor credit reports monthly during divorce

- Pay all bills on time to maintain good credit

- Document any spouse spending that damages shared credit

Your credit score affects future housing, loans, and financial security. A vindictive spouse can destroy your credit through excessive spending. Courts may order reimbursement later, but damage to your score happens immediately.

Dividing Assets: Property, Retirement, and Investments

Asset division causes the most conflict in divorce. Houses, retirement accounts, businesses, and investments require careful evaluation and negotiation.

The Marital Home: Stay, Sell, or Split?

Three main options exist for the family home. One spouse can keep it by buying out the other’s share. Both can sell and split proceeds. Or they can co-own temporarily until market conditions improve.

Keeping the house requires refinancing in your name alone. Most lenders need proof you can afford the mortgage on your income. Many people qualify while married but fail when applying alone.

Home Division Options Comparison

| Option | Requirements | Costs | Timeline |

|---|---|---|---|

| One Spouse Keeps | Refinance approval, buyout funds | Closing costs, appraisal fee | 30-60 days |

| Sell Home | Market conditions, buyer found | Realtor fees (6%), repairs | 60-180 days |

| Temporary Co-ownership | Written agreement, shared expenses | Ongoing maintenance | Varies |

Calculate total costs before deciding. Factor in mortgage payments, property taxes, insurance, maintenance, and repairs. Many people can’t afford homes they kept in divorce. Research divorce filing fees and other costs that reduce available cash.

Dividing Retirement Accounts (QDRO Guide)

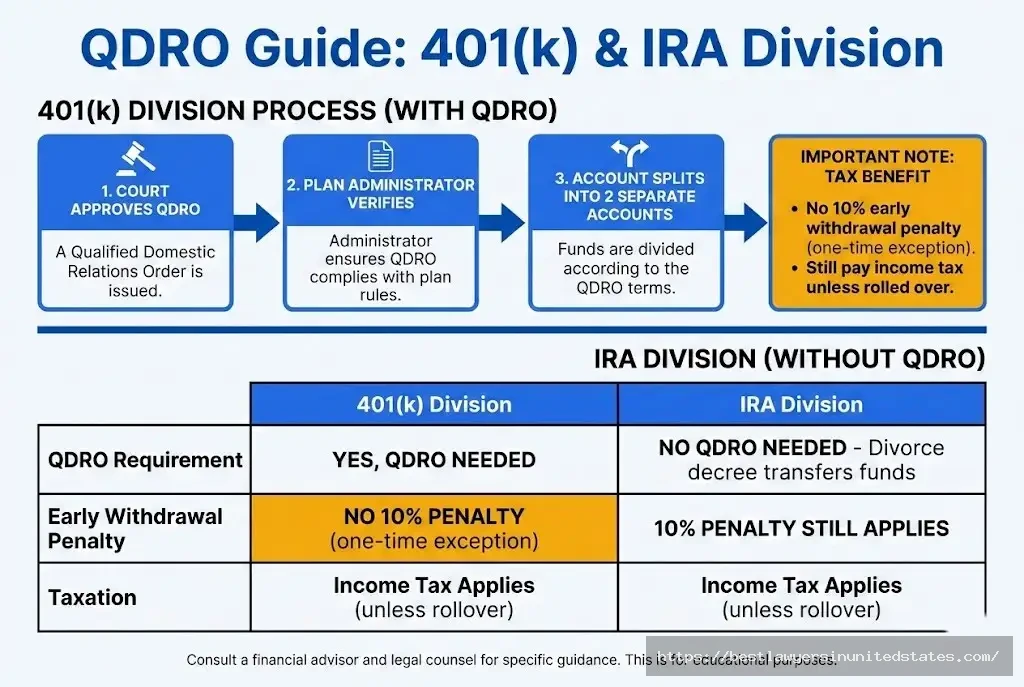

A Qualified Domestic Relations Order splits retirement accounts without tax penalties. QDROs apply to 401(k) plans, 403(b) plans, and most pensions. IRAs use different rules but achieve similar results.

The QDRO process starts after divorce decree but before retirement. Courts approve the order. Plan administrators verify it meets requirements. Then they split the account into two separate accounts.

401(k) vs IRA Division Differences

| Account Type | Division Method | Tax Treatment | Early Withdrawal |

|---|---|---|---|

| 401(k) | QDRO required | Tax-deferred if rolled over | No 10% penalty with QDRO |

| IRA | Divorce decree | Tax-deferred if rolled over | 10% penalty applies |

| Pension | QDRO required | Tax-deferred if rolled over | Depends on plan rules |

You can withdraw QDRO funds without the usual 10% early withdrawal penalty. This one-time exception helps people who need cash immediately. You still pay income tax on withdrawals unless you roll over to another qualified retirement account.

Investment Accounts, Stocks, and Business Assets

Brokerage accounts transfer through your divorce decree. Capital gains taxes apply when you sell investments later. Track the cost basis carefully to calculate future tax liability.

Stock options and restricted stock require special valuation. Vesting schedules affect when you can access the money. Unvested options might be marital property even though you can’t sell them yet.

Business ownership complicates divorce significantly. Professional appraisers value the business. Options include buying out the spouse’s share, selling the business, or continuing as co-owners.

Cryptocurrency and digital assets need disclosure like any other property. Courts treat them as assets subject to division. Track wallet addresses, exchange accounts, and transaction history.

Calculate Your Divorce Costs

Planning a divorce? Use our free calculator to estimate your total costs based on filing fees, typical attorney rates, and whether your divorce is contested or uncontested.

Divorce Cost Calculator

Get an estimated cost for your divorce based on your specific situation

Your Estimated Divorce Cost

Cost Breakdown

📧 Get a Personalized Consultation

Have questions about your specific situation? Contact our legal experts for guidance tailored to your needs.

Contact Us via EmailCalculator features:

- State-specific filing fees

- Attorney cost estimates by complexity

- Contested vs uncontested comparison

- Total cost breakdown

- Money-saving tips based on your situation

Need help finding an affordable divorce attorney? Contact family law attorneys for free consultation at [email protected]

Spousal Support and Child Support Payments

Courts order support payments to balance income inequality and provide for children. State formulas and guidelines determine amounts and duration.

Understanding Alimony/Spousal Maintenance

Alimony helps lower-earning spouses maintain a reasonable standard of living. Temporary support lasts during the divorce process. Rehabilitative support continues for a set period while the recipient gains job skills. Permanent support rarely happens except in long marriages with significant income gaps.

State laws vary widely on alimony calculations. Some use specific formulas based on income difference and marriage length. Others give judges broad discretion to consider multiple factors.

Alimony Calculation Factors

- Length of marriage (longer marriages = more likely)

- Income and earning capacity of each spouse

- Standard of living during marriage

- Age and health of both parties

- Contributions to marriage (including homemaking)

- Education and employment history

- Property division in the divorce settlement

Tax treatment changed in 2019. Divorces finalized before January 1, 2019 allow the payer to deduct alimony and require the recipient to claim it as income. Divorces after that date provide no tax deduction or income reporting for alimony payments.

Calculate Alimony Payments

Wondering about spousal support? Our calculator estimates alimony payments based on your state’s guidelines, income difference, marriage length, and other factors.

Calculator features:

- State-specific alimony formulas

- Duration estimates

- Income-based calculations

- Modification factors

Questions about your divorce or need legal help? Find Divorce Lawyers – Free Consultation or email [email protected]

Child Support Obligations

Child support covers expenses for children’s basic needs. State guidelines calculate amounts based on parents’ incomes and custody arrangements. Most states use either income shares or percentage of income models.

The income shares model estimates what married parents would spend on children. Courts divide this amount between parents based on their income percentages. The percentage of income model takes a flat percentage of the non-custodial parent’s income.

What Child Support Covers

- Basic necessities (food, clothing, housing)

- Medical and dental care

- Health insurance premiums

- Educational expenses

- Childcare costs for work or job training

- Extracurricular activities

- Transportation between homes

Additional expenses beyond basic support include private school tuition, special medical needs, and extraordinary activity costs. Parents negotiate these separately or courts add them to the support order.

Calculate Child Support

Have children? Our calculator estimates child support payments based on your state’s child support guidelines.

Calculator features:

- State-specific child support formulas

- Income shares model calculations

- Custody time adjustments

- Additional expense estimates

Questions about your divorce or need legal help? Find Divorce Lawyers – Free Consultation or email [email protected]

Tax Implications of Divorce

Divorce changes your tax situation immediately. Filing status, deductions, exemptions, and capital gains all shift when you separate.4

Filing Status Changes

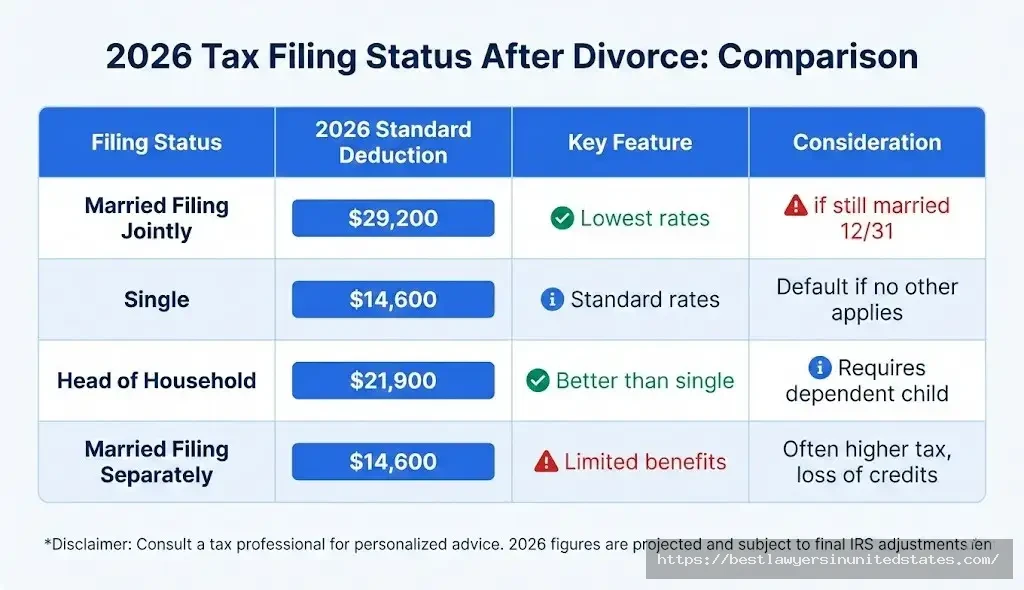

Your marital status on December 31 determines your tax filing options for that year. Married couples who finalize divorce before year-end must file as single or head of household. Those still married on December 31 can file jointly or separately.

Head of household status offers better tax rates than filing single. You qualify if you’re unmarried, paid more than half the household costs, and have a dependent child living with you for over half the year.

2026 Tax Filing Status Options

| Status | Requirements | Standard Deduction | Tax Benefits |

|---|---|---|---|

| Married Filing Jointly | Still married 12/31 | $29,200 | Lowest tax rates |

| Married Filing Separately | Still married 12/31 | $14,600 | Limited deductions |

| Single | Divorced by 12/31 | $14,600 | Standard rates |

| Head of Household | Divorced, dependent child | $21,900 | Better than single |

Child tax credits and dependent exemptions typically go to the custodial parent. Courts can assign these benefits to the non-custodial parent in the divorce decree. The custodial parent must sign Form 8332 to release the exemption.

Capital Gains Tax on Asset Transfers

Asset transfers between spouses during divorce avoid immediate taxes. You receive the same cost basis your spouse had. Capital gains taxes apply only when you sell the asset later.

Primary residence sales get special treatment. Single sellers exclude $250,000 of gain from taxes. Married couples filing jointly exclude $500,000. You must own and live in the home for 2 of the past 5 years to qualify.

Investment property sales face full capital gains taxes. Long-term capital gains rates range from 0% to 20% based on income. State taxes may add another 0% to 13.3%.

Tax Planning Strategies

Timing matters for tax optimization. Finalizing divorce early in the tax year gives more time for financial adjustments. Late-year divorces force rushed decisions about filing status and deductions.

Coordinate with a tax professional before signing settlement agreements. Property divisions that look equal might have different after-tax values. A $100,000 IRA worth $75,000 after taxes doesn’t equal $100,000 in a checking account.

Quarterly estimated tax payments need adjustment after divorce. Income changes, deduction losses, and filing status shifts all affect your tax liability. Underpayment penalties apply if you don’t adjust payments throughout the year.

Insurance Considerations During and After Divorce

Health coverage, life insurance, and disability protection need immediate updates during divorce. Losing coverage or naming the wrong beneficiary creates serious financial risks.

Health Insurance Coverage

Employer-sponsored family plans typically drop ex-spouses after divorce. COBRA continuation coverage lets you keep the same insurance for up to 36 months. You pay the full premium plus a 2% administrative fee.

COBRA costs more than employee contributions because employers no longer subsidize the premium. Monthly costs often range from $600 to $2,000 for individual coverage. Family coverage costs even more if you’re covering children.

Health Insurance Options After Divorce

| Option | Cost | Coverage | Duration |

|---|---|---|---|

| COBRA | Full premium + 2% | Same as before | Up to 36 months |

| Employer Plan | Varies | New plan | Ongoing |

| Marketplace (ACA) | Based on income | Multiple options | Annual enrollment |

| Medicaid | Free/low-cost | State program | Based on eligibility |

Affordable Care Act marketplace plans offer alternatives to COBRA. Divorce qualifies as a special enrollment period. You can shop for coverage outside the normal annual enrollment window. Premiums vary based on income, age, and location.

Life Insurance for Support Obligations

Courts often require life insurance to secure alimony and child support payments. If the paying spouse dies, insurance proceeds replace lost income. The receiving spouse becomes the irrevocable beneficiary.

Irrevocable beneficiaries can’t be changed without their written consent. This protection ensures support obligations continue even after remarriage or family changes. Policy ownership determines who controls the coverage.

The spouse receiving support should own the policy when possible. This prevents the paying spouse from letting coverage lapse. Annual proof of premium payment provides verification the insurance remains active.

Updating Property and Auto Insurance

Homeowners and auto insurance policies need immediate updates. Remove your ex-spouse from policies covering property you’re keeping. Add them to policies for property they received.

Renter’s insurance becomes necessary if you move to an apartment. Coverage protects your belongings from theft, fire, and damage. Liability protection covers injuries to visitors in your new home.

Auto insurance companies offer discounts for multiple policies. Bundling home and auto coverage saves 15-25% on premiums. Shop around for better rates when your marital discount disappears.

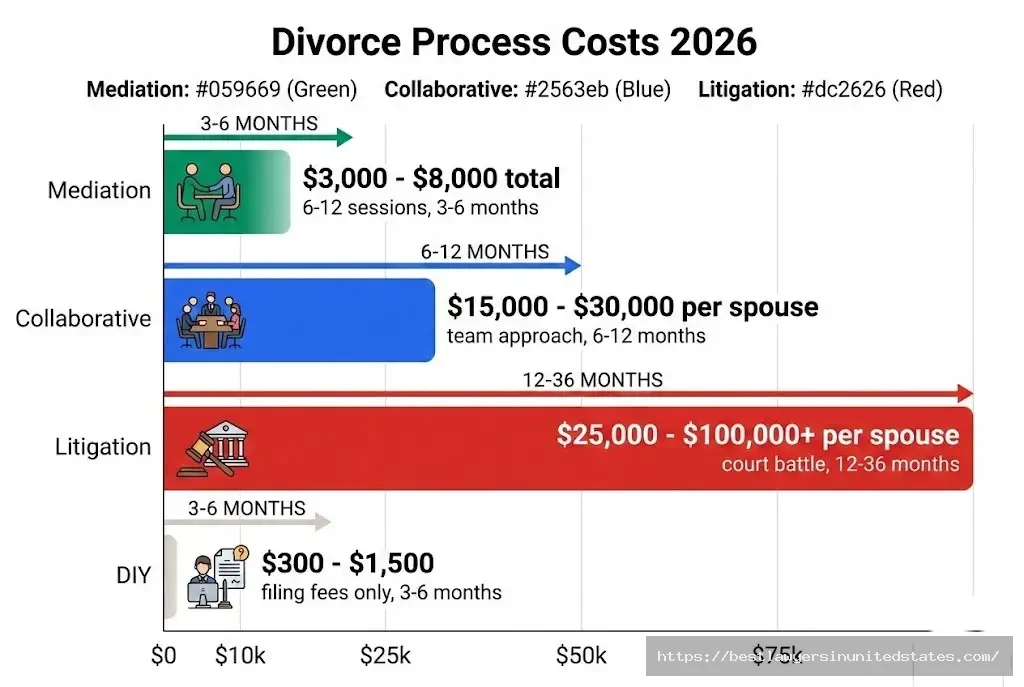

Divorce Process Options: Cost and Financial Impact

How you divorce affects total costs significantly. Mediation, collaboration, litigation, and DIY each carry different price tags and timelines.

Mediation: The Cost-Effective Approach

Divorce mediation costs $3,000 to $8,000 total for most cases. A neutral mediator helps both spouses reach agreement on all issues. You control the process instead of letting a judge decide.

Mediators charge $100 to $400 per hour. Most cases need 6 to 12 sessions. You still need an attorney to review the final agreement before signing.

Financial transparency helps mediation succeed. Both spouses disclose all assets, debts, income, and expenses. Hidden assets destroy trust and end the mediation process.

Collaborative Divorce: Professional Team Approach

Collaborative divorce uses a team of professionals to reach settlement. Each spouse has an attorney. The team adds financial advisors, child specialists, and mental health professionals as needed.

Total costs range from $15,000 to $30,000 per spouse. The team approach costs more than mediation but less than litigation. Everyone signs an agreement to negotiate in good faith.

The participation agreement creates financial stakes. If negotiation fails, both attorneys must withdraw. Spouses hire new lawyers for trial. This motivates everyone to reach settlement.

Litigation: When Court Becomes Necessary

Court battles cost $25,000 to $100,000+ per spouse for complex cases. Attorney fees run $300 to $500 per hour in most markets. High-conflict cases burn through retainers quickly.

Expert witnesses add thousands to litigation costs. Business valuators charge $5,000 to $25,000. Forensic accountants cost $10,000 to $50,000 for complex asset tracing. Child custody evaluators add $3,000 to $10,000.

Court timelines extend 12 to 36 months for contested divorces. Each hearing, motion, and discovery request adds fees. Emotional costs multiply alongside financial expenses.

DIY Divorce: Risks and Savings

Self-filing saves money but carries risks. Filing fees and court costs total $300 to $500 in most states. You skip attorney fees if you handle everything yourself.

DIY works best for short marriages with minimal assets and no children. Both spouses must agree on all terms. One mistake in paperwork can delay finalization for months.

State-specific DIY guides help you file correctly. Many courts offer self-help centers and form packets. Online services provide document preparation for $300 to $1,500.

Common Financial Mistakes to Avoid in Divorce

These mistakes cost thousands in unnecessary expenses or lost assets. Avoid them to protect your financial future.

Top Financial Errors in Divorce

- Waiting until after divorce to plan finances

- Agreeing to settlement without full analysis

- Keeping a house you can’t afford alone

- Overlooking tax consequences of asset transfers

- Delaying beneficiary updates on accounts

- Hiding or devaluing assets before settlement

- Ignoring future expense obligations

- Skipping professional financial advice

- Making emotional decisions instead of logical ones

- Failing to protect credit during the process

Each mistake has long-term consequences. A house you can’t afford leads to foreclosure. Hidden assets result in fraud charges. Emotional decisions create settlements you regret for decades.

Get professional help even for simple divorces. A Certified Divorce Financial Analyst costs $200 to $400 per hour but saves thousands in mistakes. They model settlement scenarios and project long-term financial impacts.

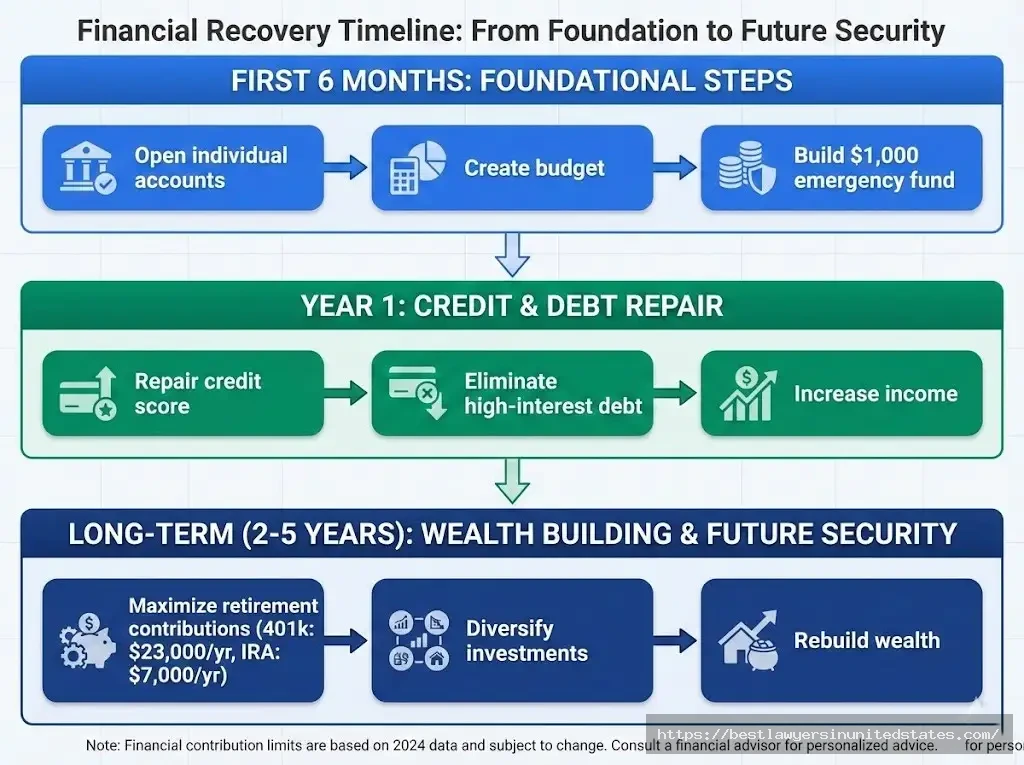

Post-Divorce Financial Recovery Strategies

Recovery takes time and planning. Most people need 2 to 5 years to stabilize finances and rebuild savings after divorce.

First 6 Months: Stabilization

Open new individual accounts immediately. Transfer your income to accounts controlled only by you. Update direct deposits and automatic payments to reflect your new accounts.

Create a realistic post-divorce budget. Track every expense for 60 days to understand your actual spending. Most people underestimate costs by 20-30% when guessing.

Essential Budget Categories

- Housing (rent/mortgage, insurance, utilities)

- Transportation (car payment, insurance, gas, maintenance)

- Food and groceries

- Healthcare and insurance

- Debt payments

- Child expenses

- Savings and emergency fund

- Personal expenses

Build an emergency fund covering 3 to 6 months of expenses. Start with $1,000 if that’s all you can manage. Gradually increase savings until you reach your full goal.

Year One: Rebuilding

Credit score repair takes consistent effort. Pay all bills on time without exception. Keep credit card balances below 30% of limits. Dispute any errors on credit reports immediately.

Debt elimination speeds financial recovery. List all debts by interest rate. Pay minimums on everything while putting extra money toward the highest-rate debt. This debt avalanche method saves thousands in interest.

Income growth offsets the financial hit from divorce. Ask for a raise at your current job. Look for higher-paying positions. Start a side business or freelance work to supplement your income.

Long-Term Wealth Building

Retirement savings need aggressive catch-up contributions. You lost years of growth during marriage. Many people split retirement accounts in divorce. Maximize annual contributions to close the gap.

2026 Retirement Contribution Limits

| Account Type | Under 50 | Age 50+ |

|---|---|---|

| 401(k) | $23,000 | $30,500 |

| IRA | $7,000 | $8,000 |

| SEP-IRA | $69,000 | $69,000 |

Investment diversification protects against market downturns. Don’t keep everything in one stock or asset class. A balanced portfolio includes stocks, bonds, real estate, and cash.

Estate plan updates prevent disasters. Remove your ex-spouse from your will, trust, and power of attorney. Name new beneficiaries on all accounts. Create healthcare directives naming someone you trust.

Building Your Divorce Financial Team

Professional guidance prevents costly mistakes. Assemble your team before filing for divorce when possible.

Divorce Attorney Selection

Family law specialists handle divorce better than general practice lawyers. Look for attorneys who spend at least 75% of their time on family law cases. Experience with cases like yours matters more than years practicing law.

Fee structures vary by attorney and case complexity. Hourly rates range from $200 to $500 per hour. Flat fees work for simple uncontested divorces. Retainers require $3,000 to $10,000 upfront.

Finding divorce lawyers starts with referrals from friends who divorced. State bar associations offer referral services. Many attorneys provide free initial consultations to discuss your case.

Certified Divorce Financial Analyst (CDFA)

CDFAs specialize in the financial aspects of divorce. They analyze settlement proposals and model long-term outcomes. Their analysis reveals the true value of different options.

Services include asset division analysis, tax projection, and retirement planning. CDFAs help you understand trade-offs between keeping the house versus taking retirement assets.

Fees run $150 to $400 per hour for CDFA services. Some work directly with clients. Others consult with your attorney to provide financial expertise.

Tax Professional (CPA/Enrolled Agent)

Tax planning during divorce prevents expensive mistakes. CPAs calculate after-tax values of different assets. They project your tax liability under various settlement scenarios.

Filing assistance helps during transition years. Joint versus separate filing, timing issues, and deduction allocation all need professional guidance. Mistakes cost thousands in penalties and lost deductions.

Future tax projection shows how your settlement affects long-term tax bills. This information helps you negotiate better terms and avoid surprises at tax time.

Frequently Asked Questions About Divorce Finances

How much does divorce cost on average?

Quick Answer: The average divorce costs $7,000 to $20,000 total, with uncontested divorces at the lower end and contested divorces ranging from $15,000 to $50,000+.

Costs vary significantly by state, complexity, and whether you use mediation, collaboration, or litigation. Use our divorce cost calculator for a personalized estimate.

Who pays more financially in divorce, men or women?

Quick Answer: Women experience greater financial hardship, with 1 in 5 falling into poverty after divorce compared to men’s typical 10-40% income drop.

Women face wage gaps, career interruptions from childcare, and loss of spousal health insurance. Men lose household efficiency and often pay child support and alimony.

How are assets divided in divorce?

Quick Answer: Nine states use community property (50-50 split), while 41 states use equitable distribution (fair but not necessarily equal division).

Community property states include Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. All others divide assets based on factors like marriage length, income, and contributions.

Do I have to split my retirement account?

Quick Answer: Yes, retirement accounts earned during marriage are typically marital property subject to division in divorce.

A Qualified Domestic Relations Order (QDRO) splits 401(k)s and pensions without tax penalties. IRAs transfer through divorce decree but may face early withdrawal penalties without careful planning.

How long do I have to pay alimony?

Quick Answer: Alimony duration varies by state, marriage length, and circumstances, ranging from temporary support to permanent payments in long marriages.

Short marriages (under 5 years) rarely receive alimony. Medium marriages (5-20 years) often see alimony lasting 25-50% of marriage length. Long marriages (20+ years) may result in permanent support.

Can I keep the house after divorce?

Quick Answer: Yes, if you can qualify for refinancing in your name alone and afford all expenses on your income.

You must buy out your spouse’s equity share and refinance to remove them from the mortgage. Many people qualified while married but can’t afford the house alone after divorce.

What happens to joint credit card debt?

Quick Answer: Joint debts from marriage typically split between both spouses based on state law and ability to pay.

Courts assign debt responsibility in the divorce decree. Both spouses remain legally liable to creditors regardless of court orders. Protect your credit by closing joint accounts before divorce.

How does divorce affect my credit score?

Quick Answer: Divorce itself doesn’t affect credit, but joint account management, missed payments, and debt division can damage your score significantly.

Open individual accounts before filing. Monitor joint accounts for unauthorized charges. Pay all bills on time throughout the divorce process to maintain good credit.

When should I update my will and beneficiaries?

Quick Answer: Update beneficiaries immediately when filing for divorce and revise your estate plan as soon as the divorce finalizes.

Remove your spouse from life insurance, retirement accounts, bank accounts, and investment accounts. Many states automatically revoke spousal beneficiary designations, but don’t rely on this protection.

Do I need a QDRO for 401(k) division?

Quick Answer: Yes, 401(k) plans, 403(b) plans, and pensions require a QDRO to divide assets without tax penalties and early withdrawal fees.

IRAs don’t need QDROs but transfer through divorce decree. The QDRO must be approved by the court and the plan administrator before the split occurs.

Is alimony still tax deductible?

Quick Answer: No, alimony is no longer tax deductible for divorces finalized after December 31, 2018.

The Tax Cuts and Jobs Act eliminated the alimony deduction for new divorces. Recipients also don’t report it as taxable income. Divorces finalized before 2019 still use the old tax treatment.

How is child support calculated?

Quick Answer: States use either income shares or percentage of income models based on parents’ combined income and custody time.

Most states follow income shares guidelines that estimate what married parents would spend on children. A few states take a percentage of the non-custodial parent’s income. Use our child support calculator for estimates.

What if my spouse is hiding assets?

Quick Answer: Hire a forensic accountant to trace hidden assets through bank records, tax returns, and lifestyle analysis.

Hidden assets constitute fraud and result in serious penalties. Courts can award the entirety of hidden assets to the discovering spouse. Document suspicious spending or transfers immediately.

Can I get health insurance after divorce?

Quick Answer: Yes, through COBRA (up to 36 months), employer plans, Affordable Care Act marketplace, or Medicaid based on income.

COBRA costs the full premium plus 2% administrative fees. Marketplace plans vary by income and may qualify for subsidies. Divorce creates a special enrollment period outside annual enrollment.

Should I file taxes jointly or separately during divorce?

Quick Answer: Filing jointly usually saves money but requires trust and cooperation with your spouse on tax liability and refunds.

Joint filing offers better tax rates and higher deductions. Separate filing protects you from spouse’s tax issues but costs more. Consult a CPA to model both options before deciding.

Conclusion

Divorce creates major financial challenges, but smart planning reduces damage and speeds recovery. Understanding property division, support obligations, tax changes, and insurance needs helps you protect your assets.

Use our divorce cost calculator to estimate expenses. Research state-specific divorce laws that affect your settlement. Consider working with a Certified Divorce Financial Analyst to model long-term outcomes.

Financial recovery takes time, but most people rebuild within 2 to 5 years. Build your professional team early, avoid common mistakes, and focus on long-term wealth building. Your financial future depends on the decisions you make during divorce.

Need professional guidance? Find experienced divorce lawyers offering free consultations, or contact [email protected] for help finding the right attorney for your situation.